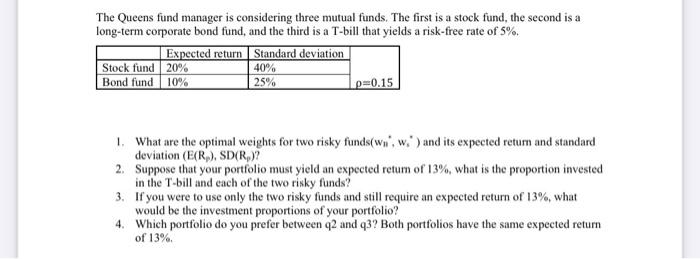

Question: please help The Queens fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term corporate bond fund,

The Queens fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term corporate bond fund, and the third is a T-bill that yields a risk-free rate of 5%. Expected return Standard deviation Stock fund 20% 40% Bond fund 10% 25% p=0.15 3. If you were to use only the two risky funds and still require an expected return of 13%, what would be the investment proportions of your portfolio? 4. Which portfolio do you prefer between q2 and q3? Both portfolios have the same expected return of 13%. The Queens fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term corporate bond fund, and the third is a T-bill that yields a risk-free rate of 5%. Expected return Standard deviation Stock fund 20% Bond fund 10% p=0.15 40% 25% 1. What are the optimal weights for two risky funds/wn'.w.) and its expected return and standard deviation (E(R), SD(R)? 2. Suppose that your portfolio must yield an expected return of 13%, what is the proportion invested in the T-bill and each of the two risky funds? 3. If you were to use only the two risky funds and still require an expected return of 13%, what would be the investment proportions of your portfolio? 4. Which portfolio do you prefer between q2 and 43? Both portfolios have the same expected return of 13%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts