Question: please help Total, nondiversifiable, and diversifiable risk David Talbot randomly selected securities from all those listed on the New York Stock Exchange for his portfolio.

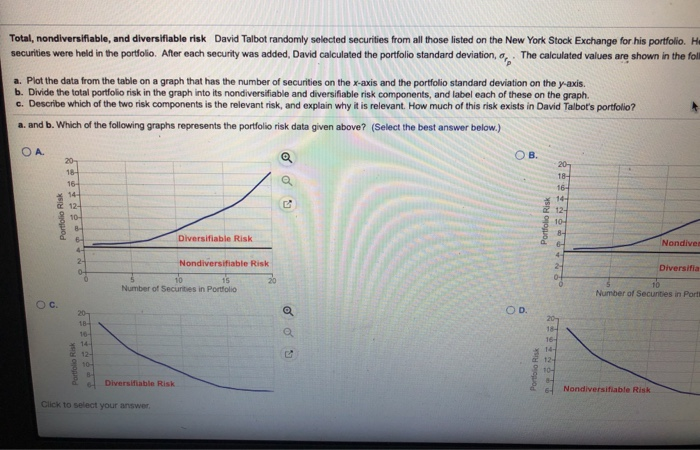

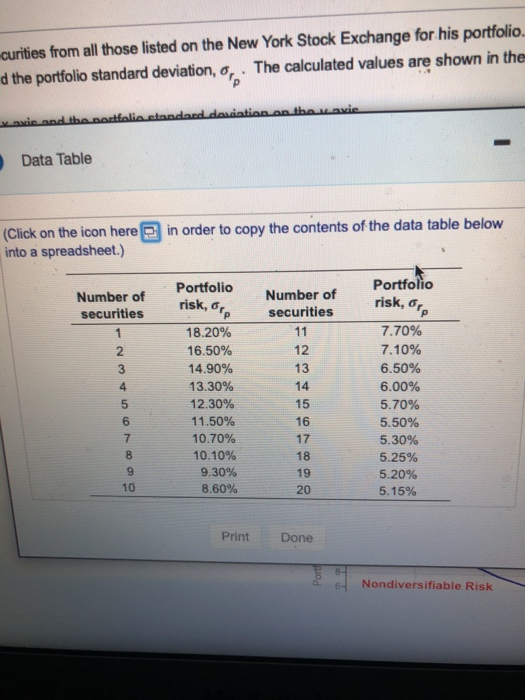

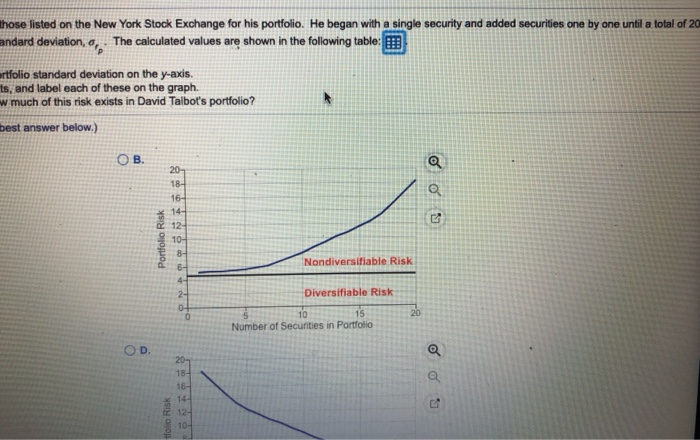

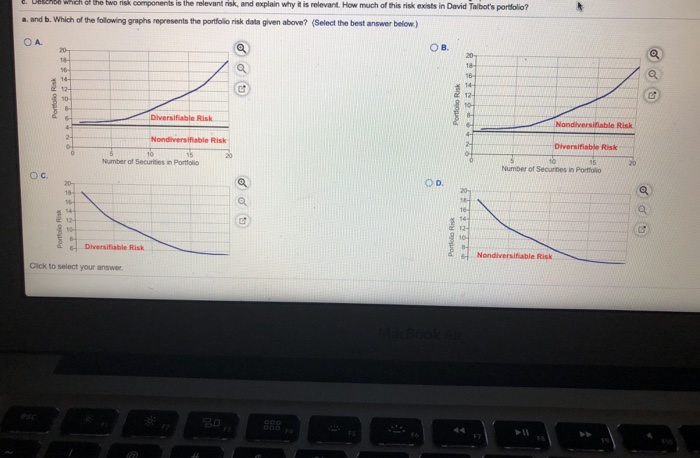

Total, nondiversifiable, and diversifiable risk David Talbot randomly selected securities from all those listed on the New York Stock Exchange for his portfolio. He securities were held in the portfolio. After each security was added, David calculated the portfolio standard deviation, o, The calculated values are shown in the follo a. Plot the data from the table on a graph that has the number of securities on the x-axis and the portfolio standard deviation on the y-axis. b. Divide the total portfolio risk in the graph into its nondiversifiable and diversifiable risk components, and label each of these on the graph. c. Describe which of the two risk components is the relevant risk, and explain why it is relevant. How much of this risk exists in David Talbot's portfolio? a. and b. Which of the following graphs represents the portfolio risk data given above? (Select the best answer below.) OA . 20 18 16 Portfolio Risk 20 18 16- 14- 2 12- 10- 8- 12 10 B Portfolio Risk Diversifiable Risk Nondiver 4 2- Diversifia Nondiversifiable Risk 15 Number of Securities in Portfolio 10 Number of Securities in Port OD 20 18- 10- 14 12- e 20- 18- 16- Porto RR Porto Risk 12 10- 11 Diversifiable Risk Nondiversifiable Risk Click to select your answer d the portfolio standard deviation, p -curities from all those listed on the New York Stock Exchange for his portfolio The calculated values are shown in the Xavie and the portfolio Standard deviation on the wavie Data Table in order to copy the contents of the data table below (Click on the icon here into a spreadsheet.) Portfolio Number of securities Portfolio risk, risk, ore 1 2 3 4 5 6 7 8 9 10 18.20% 16.50% 14.90% 13.30% 12.30% 11.50% 10.70% 10.10% 9.30% 8.60% Number of securities 11 12 13 14 15 16 17 7.70% 7.10% 6.50% 6.00% 5.70% 5.50% 5.30% 5.25% 5.20% 5.15% 18 19 20 Print Done 6- Nondiversifiable Risk those listed on the New York Stock Exchange for his portfolio. He began with a single security and added securities one by one until a total of 20 andard deviation, 1,0 The calculated values are shown in the following table: ortfolio standard deviation on the y-axis. ts, and label each of these on the graph. w much of this risk exists in David Talbot's portfolio? best answer below.) OB. Q Q Portfolio Risk 20 18 16- 14- 2 12 10- 8- 6- 4- 2- 0 0 Nondiversifiable Risk Diversifiable Risk 10 15 Number of Securities in Portfolio 20 D. 20 18- 16- 14- 12- 10- tfolio Risk Debenso which of the two risk components is the relevant risk, and explain why it is relevant. How much of this risk exists in David Thibot's portfolio? a and b. Which of the following graphs represents the portfolio risk data given above? (Select the best answer below) OA OB 20 16 16 14 12- 10 Portfolio Risk Portfolio Risk 20 18 16 14 12- 104 3- Diversifiable Risk 4 Nondiversifiable Risk 2 2- Nondiversifiable Risk 10 15 20 Number of Securities in Portfolio Diversifiable Risk 20 15 Number of Secures in Portfolio . 20 18 OD e 14 12- 16- 14 12- Portfolio Portfolio Risk Diversifiable Risk Nondiversifiable Risk Click to select your answer c. Describe which of the two risk components is the relevant risk, and explain why it is relevant. How much of this risk exists in David Talbot's portfolio? (Select the best answer below.) O A Only nondiversifiable risk is relevant because, as shown by the graph, diversifiable risk can be virtually eliminated through holding a portfolio of at least 20 securities that are not posim diversifiable risk could no longer be reduced by additions to the portfolio, has 5.15% relevant risk. OB. Only diversifiable risk is relevant because, as shown by the graph, nondiversifiable risk can be virtually eliminated through holding a portfolio of at least 20 securities that are not posit nondiversifiable risk could no longer be reduced by additions to the portfolio, has 18.20% relevant risk. OC. Only nondiversifiable risk is relevant because, as shown by the graph, diversifiable risk can be virtually eliminated through holding a portfolio of at least 20 securities that are not positi diversifiable risk could no longer be reduced by additions to the portfolio, has 18.20% relevant risk. OD Only diversifiable risk is relevant because, as shown by the graph, no diversifiable risk can be virtually eliminated through holding a portfolio of at least 20 securities that are not positiv nondiversifiable risk could no longer be reduced by additions to the portfolio, has 5.15% relevant risk. Click to select your

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts