Question: Please help with a. and b. Refer to the Mini-S&P contract in Figure 22.1. Assume the closing price for this day. a. If the margin

Please help with a. and b.

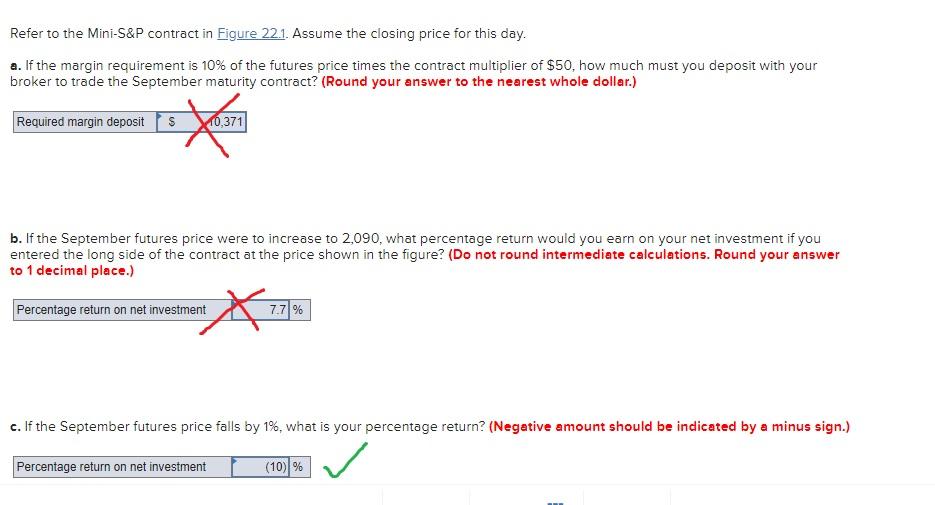

Refer to the Mini-S&P contract in Figure 22.1. Assume the closing price for this day. a. If the margin requirement is 10% of the futures price times the contract multiplier of $50, how much must you deposit with your broker to trade the September maturity contract? (Round your answer to the nearest whole dollar.) Required margin deposit S X 371 b. If the September futures price were to increase to 2,090, what percentage return would you earn on your net investment if you entered the long side of the contract at the price shown in the figure? (Do not round intermediate calculations. Round your answer to 1 decimal place.) Percentage return on net investment 7.7 % c. If the September futures price falls by 1%, what is your percentage return? (Negative amount should be indicated by a minus sign.) Percentage return on net investment (10) % Refer to the Mini-S&P contract in Figure 22.1. Assume the closing price for this day. a. If the margin requirement is 10% of the futures price times the contract multiplier of $50, how much must you deposit with your broker to trade the September maturity contract? (Round your answer to the nearest whole dollar.) Required margin deposit S X 371 b. If the September futures price were to increase to 2,090, what percentage return would you earn on your net investment if you entered the long side of the contract at the price shown in the figure? (Do not round intermediate calculations. Round your answer to 1 decimal place.) Percentage return on net investment 7.7 % c. If the September futures price falls by 1%, what is your percentage return? (Negative amount should be indicated by a minus sign.) Percentage return on net investment (10) %

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts