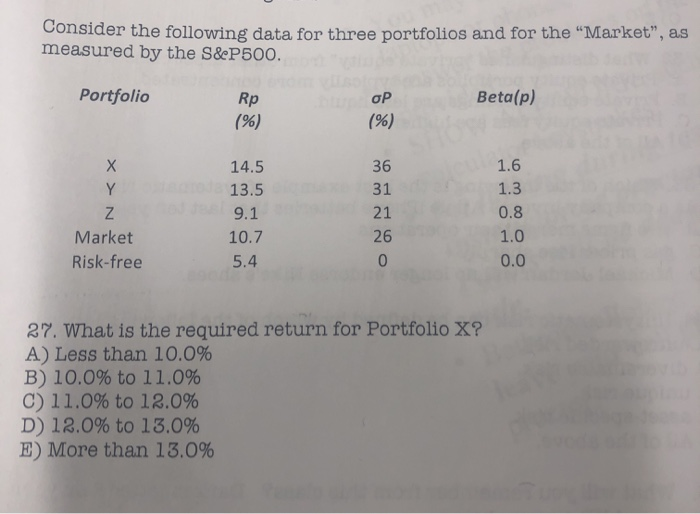

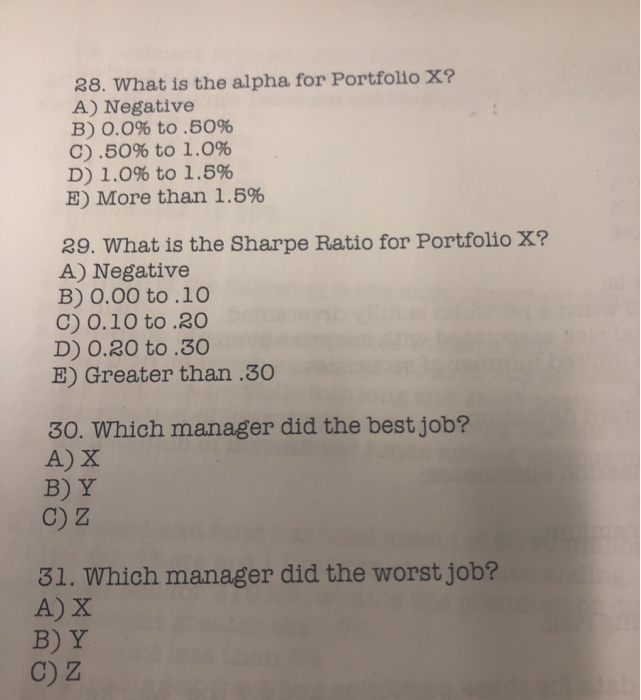

Question: please help with all 5. its a 5 part question. thank you. Consider the following data for three portfolios and for the Market, as measured

Consider the following data for three portfolios and for the "Market", as measured by the S&P500. Portfolio Beta(p) Rp (%) (%) 1.6 Y 1.3 14.5 13.5 9.1 10.7 5.4 0.8 1.0 Market Risk-free 0.0 27. What is the required return for Portfolio X?! A) Less than 10.0% B) 10.0% to 11.0% C) 11.0% to 12.0% D) 12.0% to 13.0% E) More than 13.0% 28. What is the alpha for Portfolio X? A) Negative B) 0.0% to .50% C) .50% to 1.0% D) 1.0% to 1.5% E) More than 1.5% 29. What is the Sharpe Ratio for Portfolio X? A) Negative B) 0.00 to .10 C) 0.10 to 20 D) 0.20 to .30 E) Greater than .30 30. Which manager did the best job? A) X B) Y CZ 31. Which manager did the worst job? A) X BY CZ

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts