Question: please help with both parts. someone else may know it. 14.12 Retirement Effects on Partnership Balance Sheet and Income Urban Tech is a na providing

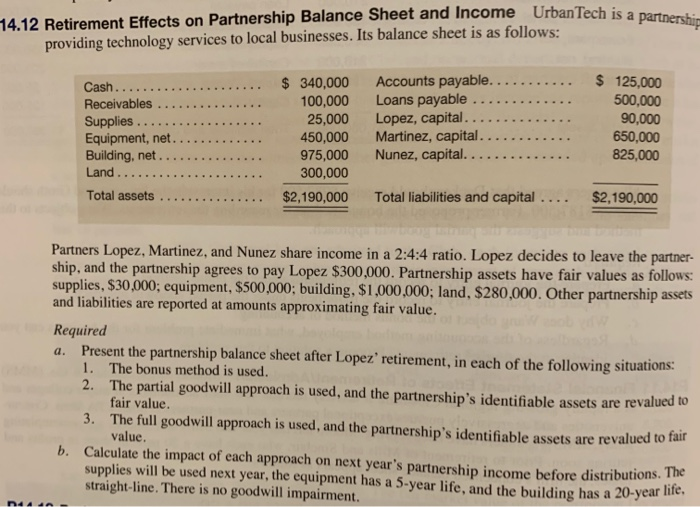

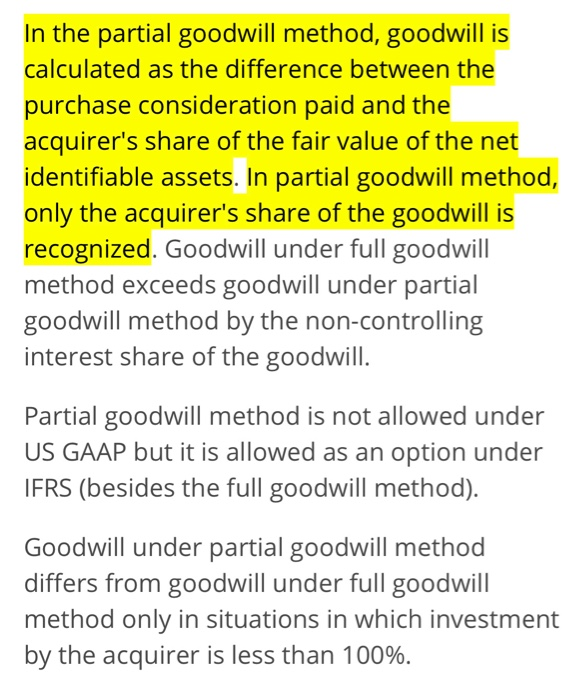

14.12 Retirement Effects on Partnership Balance Sheet and Income Urban Tech is a na providing technology services to local businesses. Its balance sheet is as follows: Cash... Receivables ............... Supplies ............ Equipment, net......... Building, net.......... Land. $ 340,000 100,000 25,000 450,000 975,000 300,000 $2,190,000 Accounts payable........... Loans payable ..... Lopez, capital. Martinez, capital..... Nunez, capital. ....... $ 125,000 500,000 90,000 650,000 825,000 Total assets .......... Total liabilities and capital .... $2,190,000 Partners Lopez, Martinez, and Nunez share income in a 2:4:4 ratio. Lopez decides to leave the partner- ship, and the partnership agrees to pay Lopez $300,000. Partnership assets have fair values as follows: supplies, $30,000; equipment, $500,000; building, $1,000,000; land, $280,000. Other partnership assets and liabilities are reported at amounts approximating fair value. Required a. Present the partnership balance sheet after Lopez' retirement, in each of the following situations 1. The bonus method is used. 2. The partial goodwill approach is used, and the partnership's identifiable assets are revalued to fair value. 3. The full goodwill approach is used, and the partnership's identifiable assets are revalued to fa value. b. Calculate the impact of each approach on next year's partnership income before distribution supplies will be used next year, the equipment has a 5-year life, and the building has a 20-year straight-line. There is no goodwill impairment. ling has a 20-year life, 144 In the partial goodwill method, goodwill is calculated as the difference between the purchase consideration paid and the acquirer's share of the fair value of the net identifiable assets. In partial goodwill method, only the acquirer's share of the goodwill is recognized. Goodwill under full goodwill method exceeds goodwill under partial goodwill method by the non-controlling interest share of the goodwill. Partial goodwill method is not allowed under US GAAP but it is allowed as an option under IFRS (besides the full goodwill method). Goodwill under partial goodwill method differs from goodwill under full goodwill method only in situations in which investment by the acquirer is less than 100%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts