Question: Please help with part C Use the Black-Scholes option pricing model to price the following European call option. 58.00 60.00 3.00% 3.00% 3 6 13.00%

Please help with part C

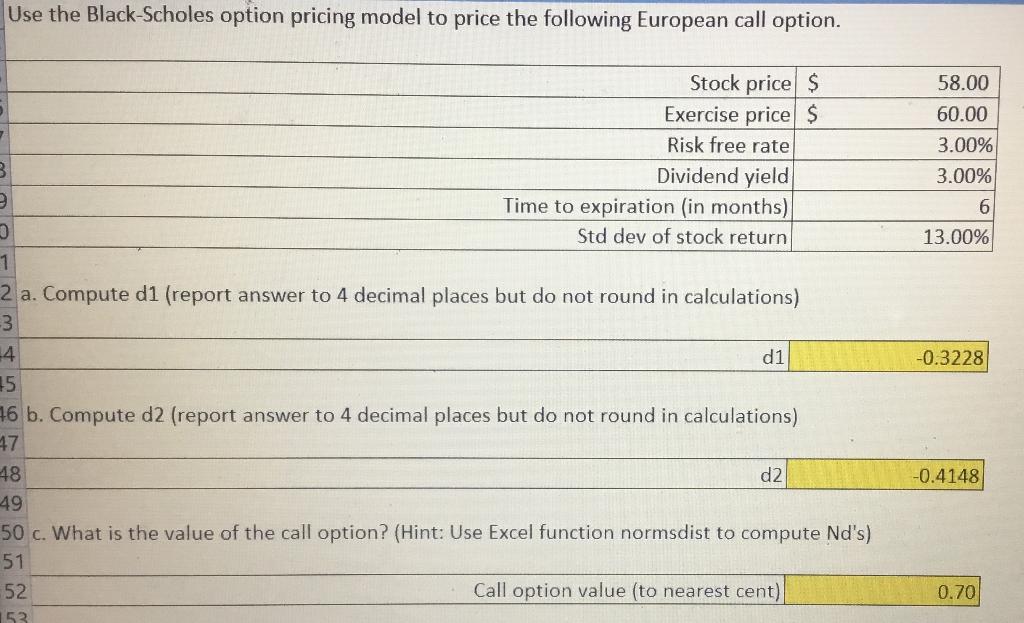

Use the Black-Scholes option pricing model to price the following European call option. 58.00 60.00 3.00% 3.00% 3 6 13.00% Stock price $ Exercise price $ Risk free rate Dividend yield Time to expiration (in months) Std dev of stock return 1 2 a. Compute d1 (report answer to 4 decimal places but do not round in calculations) 3 -4 d1 15 16 b. Compute d2 (report answer to 4 decimal places but do not round in calculations) 47 48 d2 49 50 c. What is the value of the call option? (Hint: Use Excel function normsdist to compute Nd's) 51 52 Call option value (to nearest cent) 53 -0.3228 -0.4148 0.70

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock