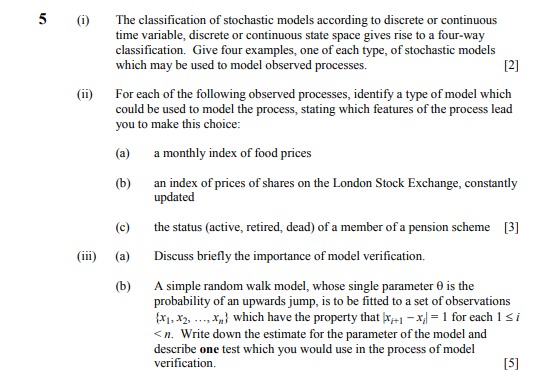

Question: Please help with the following; All questions are complete please. 6 The members of a disability insurance scheme are classified as active (A), temporarily disabled

Please help with the following;

All questions are complete please.

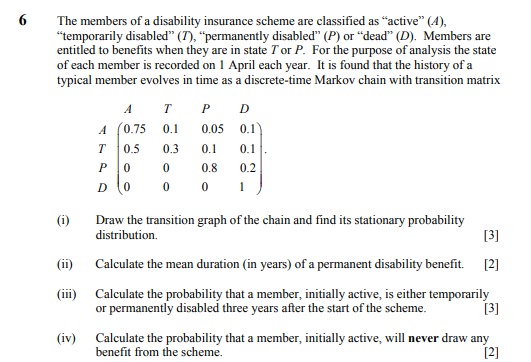

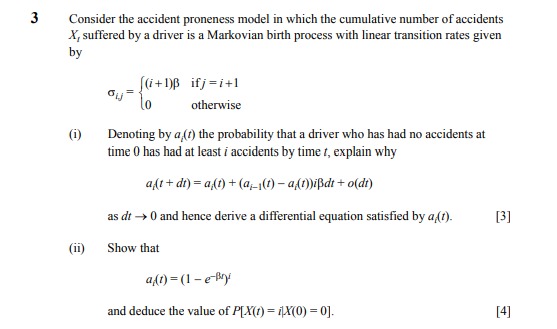

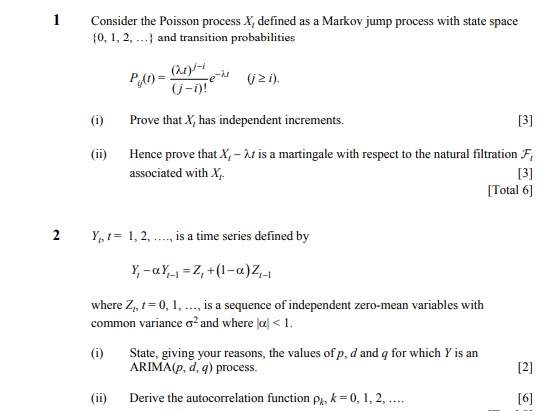

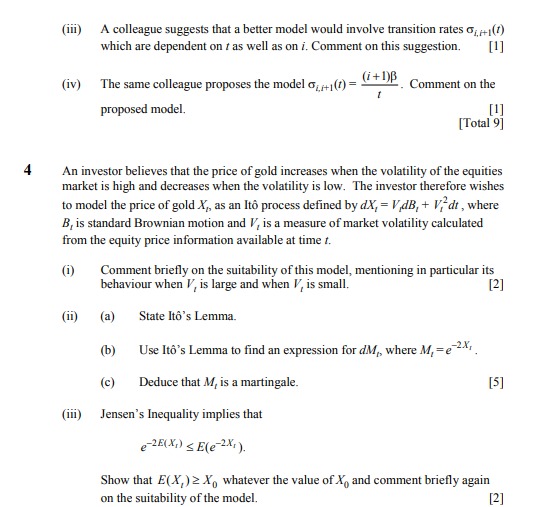

6 The members of a disability insurance scheme are classified as "active" (A), "temporarily disabled" (7), "permanently disabled" (P) or "dead" (D). Members are entitled to benefits when they are in state For P. For the purpose of analysis the state of each member is recorded on 1 April each year. It is found that the history of a typical member evolves in time as a discrete-time Markov chain with transition matrix T P D 0.75 0.1 0.05 0.1) 0.5 0.3 0.1 0.1 0 0 0.8 0.2 D 0 1 (i) Draw the transition graph of the chain and find its stationary probability distribution. [3] (ii) Calculate the mean duration (in years) of a permanent disability benefit. [2] (iii) Calculate the probability that a member, initially active, is either temporarily or permanently disabled three years after the start of the scheme. [3] (iv) Calculate the probability that a member, initially active, will never draw any benefit from the scheme. [2]3 Consider the accident proneness model in which the cumulative number of accidents X, suffered by a driver is a Markovian birth process with linear transition rates given by (i+1)p ifj=i+1 lo otherwise (i) Denoting by a (() the probability that a driver who has had no accidents at time 0 has had at least / accidents by time t, explain why aft + di) = a(0) + (a(1) - am)ipdr + o(di) as do - 0 and hence derive a differential equation satisfied by a,(). [3] (ii) Show that and deduce the value of P[X(() = 1X(0) = 0]. [4]Consider the Poisson process X, defined as a Markov jump process with state space (0, 1, 2, ...} and transition probabilities ew (izi). (j-1)! (i) Prove that X, has independent increments. [3] (ii) Hence prove that X, - 2./ is a martingale with respect to the natural filtration F associated with X,. [3] [Total 6] Y 1= 1, 2, ...., is a time series defined by Y -aY,_1 = Z, + (1-a)Z,- where Z,, 1 = 0, 1, ..., is a sequence of independent zero-mean variables with common variance oand where lo|

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts