Question: Please help with the following Return on Investment (ROI) The manager of an investment center should be evaluated based on revenues, costs, and investments. An

Please help with the following

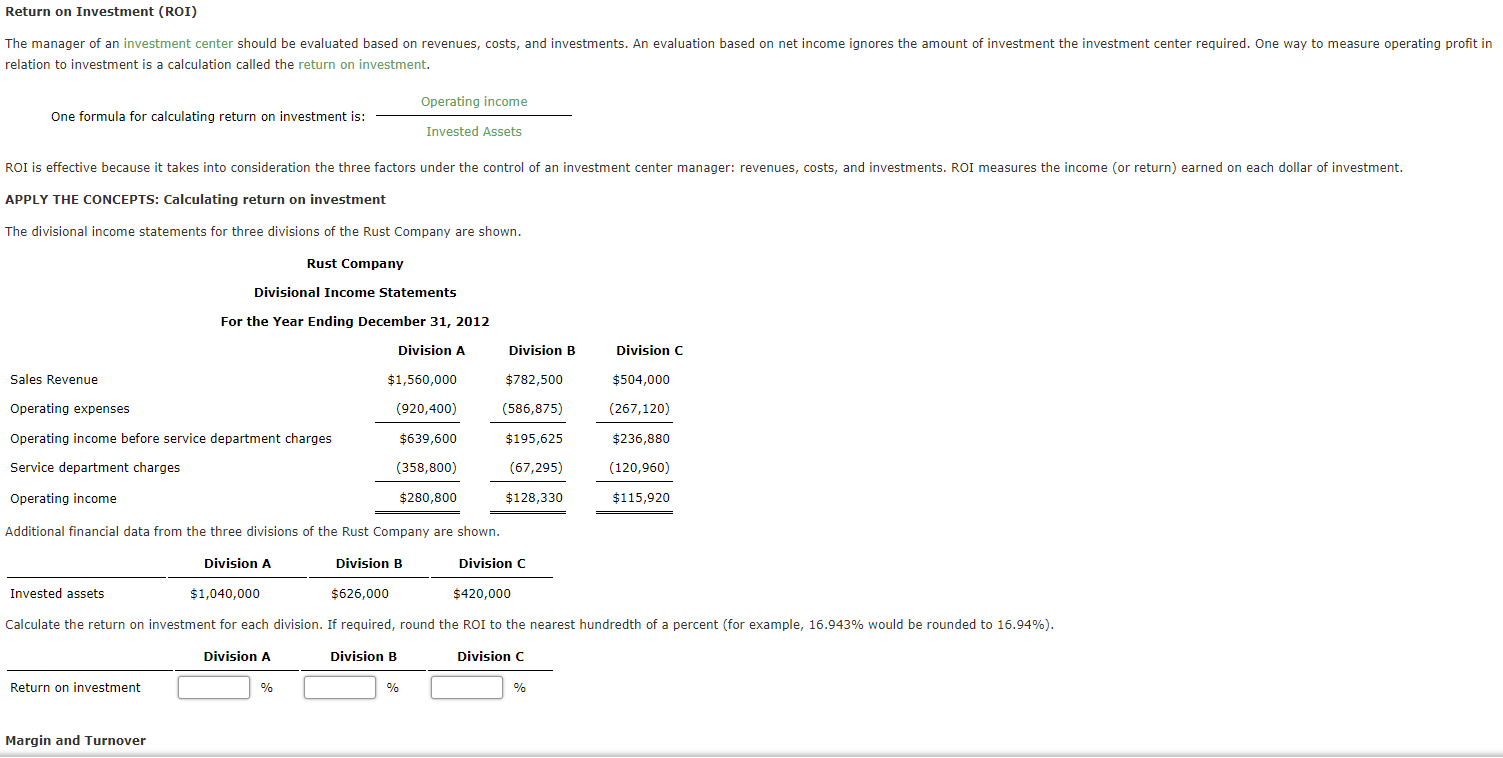

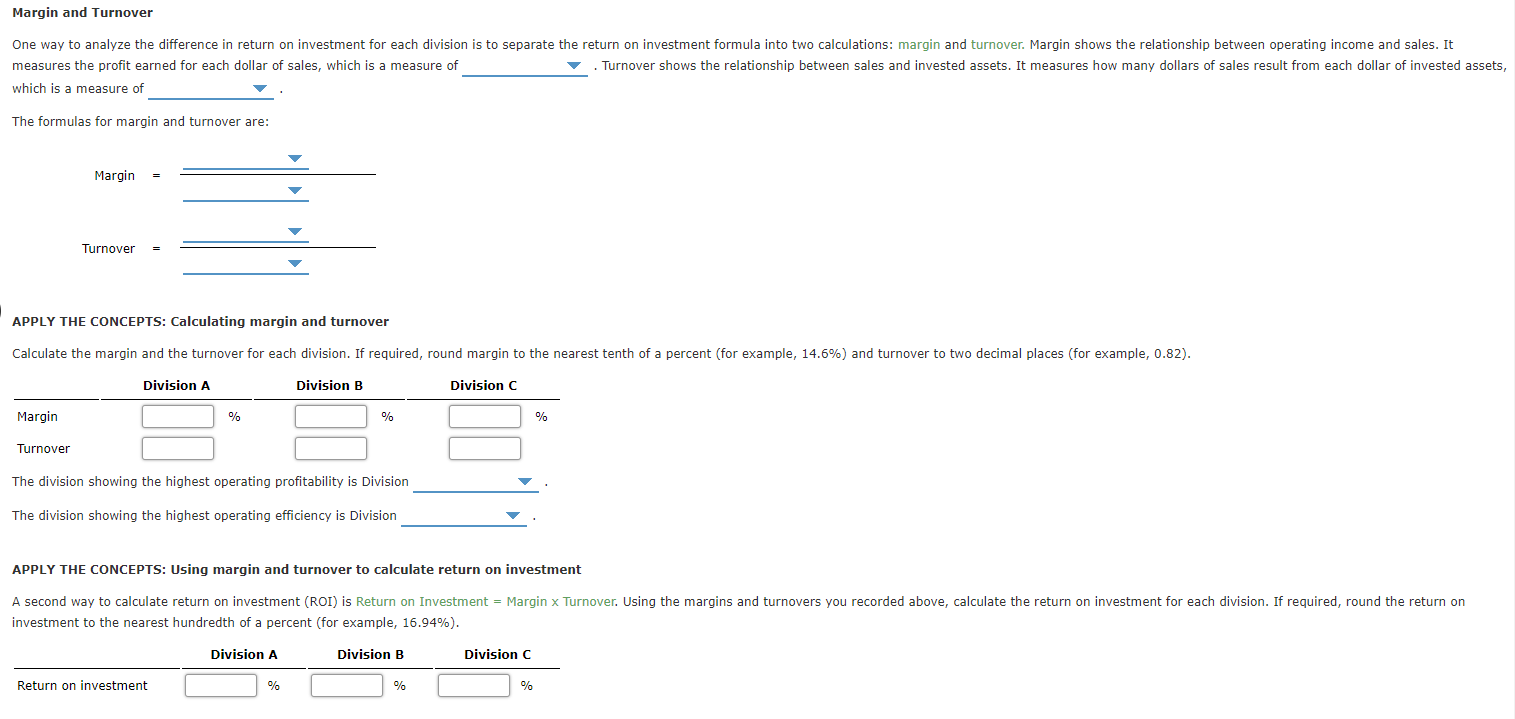

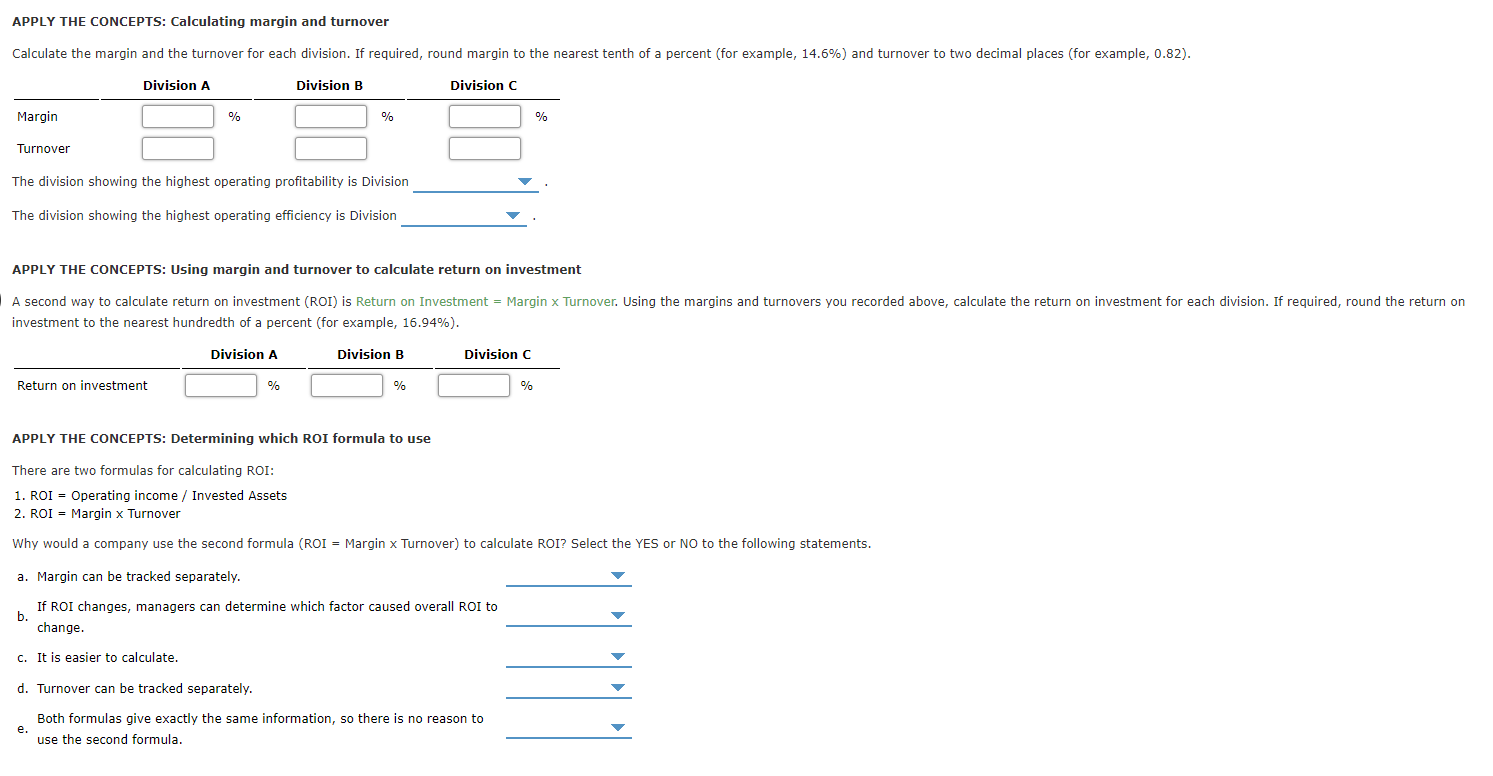

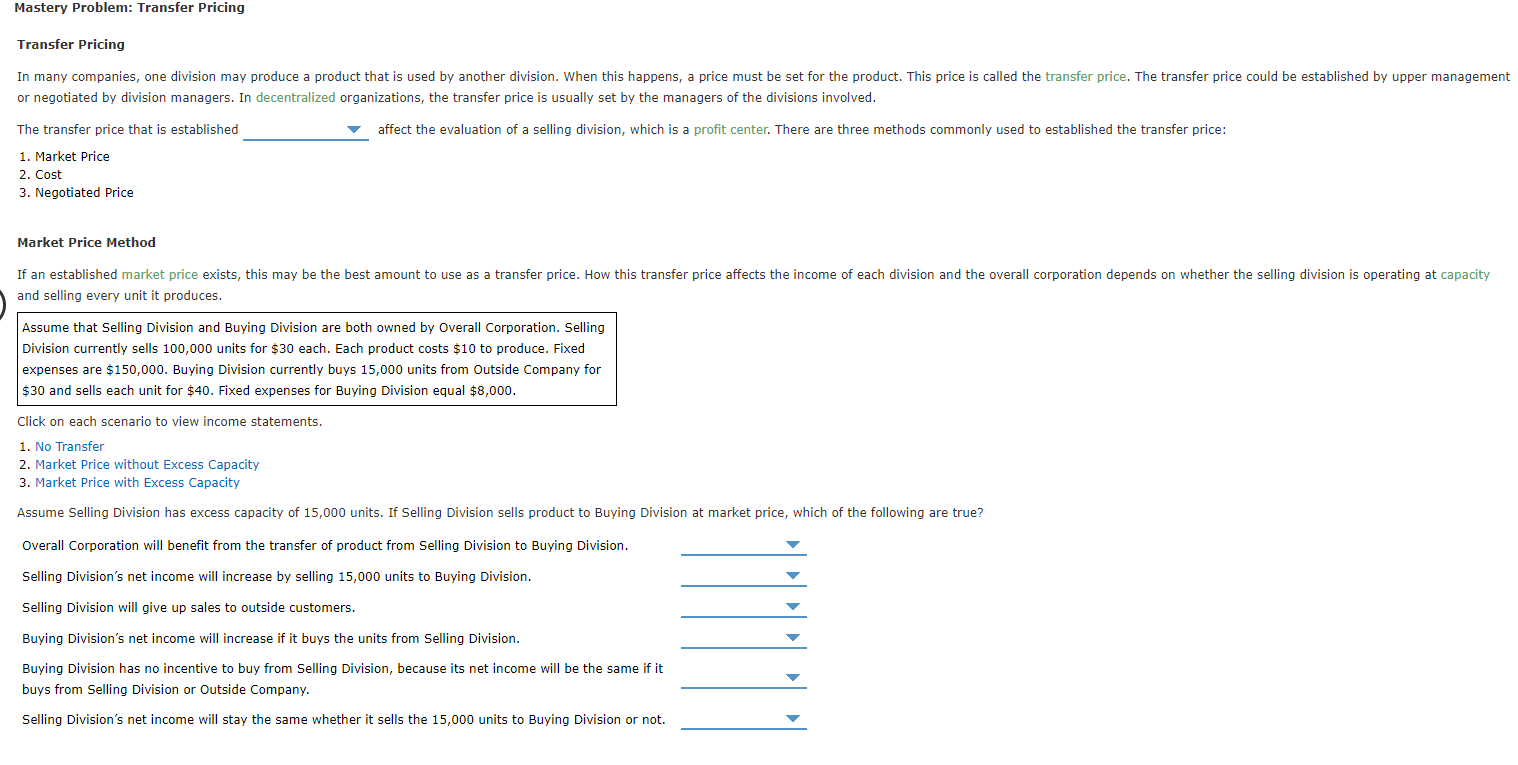

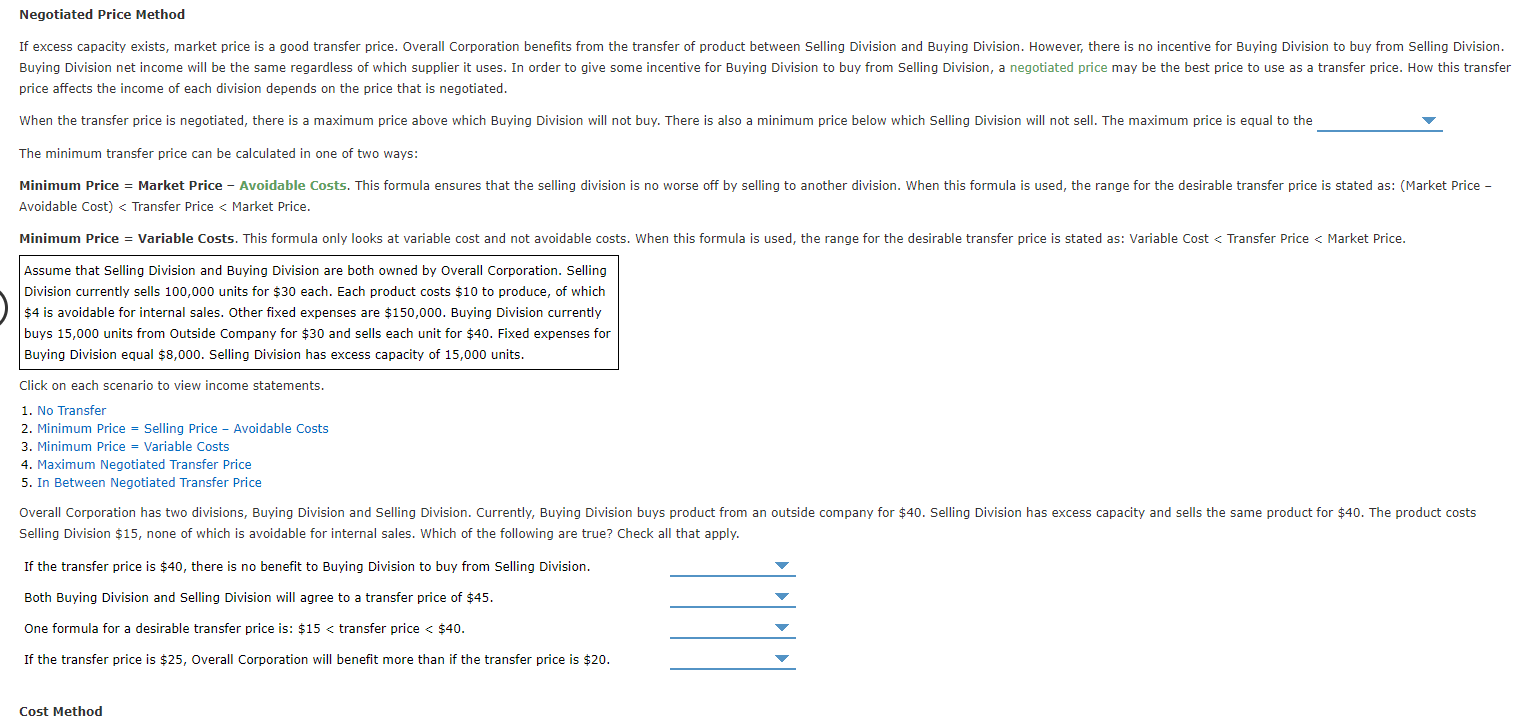

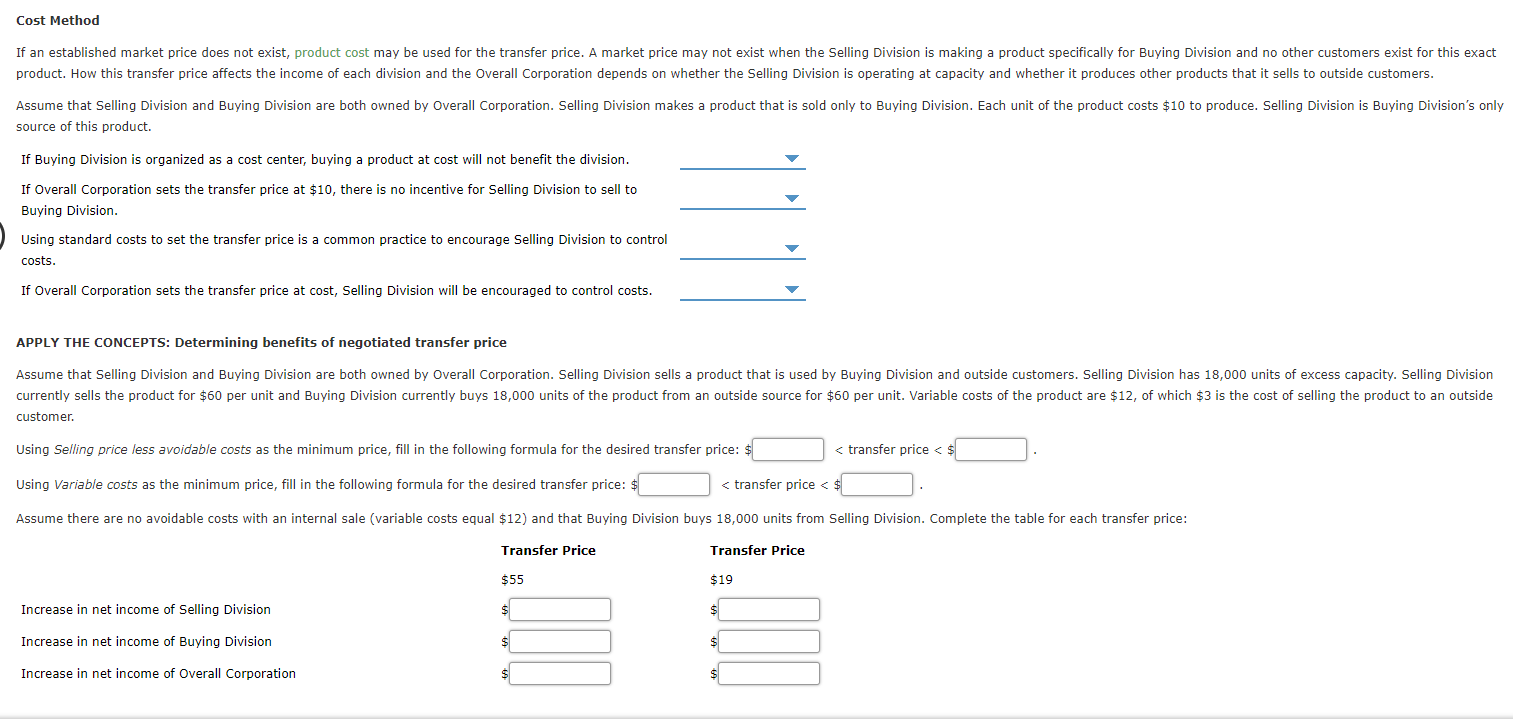

Return on Investment (ROI) The manager of an investment center should be evaluated based on revenues, costs, and investments. An evaluation based on net income ignores the amount of investment the investment center required. One way to measure operating profit in relation to investment is a calculation called the return on investment. Operating income One formula for calculating return on investment is: Invested Assets ROI is effective because it takes into consideration the three factors under the control of an investment center manager: revenues, costs, and investments. ROI measures the income (or return) earned on each dollar of investment. APPLY THE CONCEPTS: Calculating return on investment The divisional income statements for three divisions of the Rust Company are shown. Rust Company Divisional Income Statements For the Year Ending December 31, 2012 Division A Division B Division C Sales Revenue $1,560,000 $782,500 $504,000 Operating expenses (920,400) (586,875) (267,120) Operating income before service department charges $639,600 $195,625 $236,880 Service department charges (358,800) (67,295) (120,960) Operating income $280,800 $128,330 $115,920 Additional financial data from the three divisions of the Rust Company are shown. Division A Division B Division C Invested assets $1,040,000 $626,000 $420,000 Calculate the return on investment for each division. If required, round the ROI to the nearest hundredth of a percent (for example, 16.943% would be rounded to 16.94%). Division A Division B Division C Return on investment % % % Margin and Turnover Margin and Turnover One way to analyze the difference in return on investment for each division is to separate the return on investment formula into two calculations: margin and turnover. Margin shows the relationship between operating income and sales. It measures the profit earned for each dollar of sales, which is a measure of Turnover shows the relationship between sales and invested assets. It measures how many dollars of sales result from each dollar of invested assets, which is a measure of The formulas for margin and turnover are: Margin Turnover APPLY THE CONCEPTS: Calculating margin and turnover Calculate the margin and the turnover for each division. If required, round margin to the nearest tenth of a percent (for example, 14.6%) and turnover to two decimal places (for example, 0.82). Division A Division B Division C Margin % % % Turnover The division showing the highest operating profitability is Division The division showing the highest operating efficiency is Division APPLY THE CONCEPTS: Using margin and turnover to calculate return on investment A second way to calculate return on investment (ROI) is Return on Investment = Margin x Turnover. Using the margins and turnovers you recorded above, calculate the return on investment for each division. If required, round the return on investment to the nearest hundredth of a percent (for example, 16.94%). Division A Division B Division C Return on investment % % APPLY THE CONCEPTS: Calculating margin and turnover Calculate the margin and the turnover for each division. If required, round margin to the nearest tenth of a percent (for example, 14.6%) and turnover to two decimal places (for example, 0.82). Division A Division B Division C Margin % % % Turnover The division showing the highest operating profitability is Division The division showing the highest operating efficiency is Division APPLY THE CONCEPTS: Using margin and turnover to calculate return on investment A second way to calculate return on investment (ROI) is Return on Investment = Margin x Turnover. Using the margins and turnovers you recorded above, calculate the return on investment for each division. If required, round the return on investment to the nearest hundredth of a percent (for example, 16.94%). Division A Division B Division C Return on investment % APPLY THE CONCEPTS: Determining which ROI formula to use There are two formulas for calculating ROI: 1. ROI = Operating income / Invested Assets 2. ROI = Margin x Turnover Why would a company use the second formula (ROI = Margin x Turnover) to calculate ROI? Select the YES or NO to the following statements. a. Margin can be tracked separately. b. If ROI changes, managers can determine which factor caused overall ROI to change. C. It is easier to calculate. d. Turnover can be tracked separately. e. Both formulas give exactly the same information, so there is no reason to use the second formula. Mastery Problem: Transfer Pricing Transfer Pricing In many companies, one division may produce a product that is used by another division. When this happens, a price must be set for the product. This price is called the transfer price. The transfer price could be established by upper management or negotiated by division managers. In decentralized organizations, the transfer price is usually set by the managers of the divisions involved. The transfer price that is established affect the evaluation of a selling division, which is a profit center. There are three methods commonly used to established the transfer price: 1. Market Price 2. Cost 3. Negotiated Price Market Price Method If an established market price exists, this may be the best amount to use as a transfer price. How this transfer price affects the income of each division and the overall corporation depends on whether the selling division is operating at capacity and selling every unit it produces. Assume that Selling Division and Buying Division are both owned by Overall Corporation. Selling Division currently sells 100,000 units for $30 each. Each product costs $10 to produce. Fixed expenses are $150,000. Buying Division currently buys 15,000 units from outside Company for $30 and sells each unit for $40. Fixed expenses for Buying Division equal $8,000. Click on each scenario to view income statements. 1. No Transfer 2. Market Price without Excess Capacity 3. Market Price with Excess Capacity Assume Selling Division has excess capacity of 15,000 units. If Selling Division sells product to Buying Division at market price, which of the following are true? Overall Corporation will benefit from the transfer of product from Selling Division to Buying Division. Selling Division's net income will increase by selling 15,000 units to Buying Division. Selling Division will give up sales to outside customers. Buying Division's net income will increase if it buys the units from Selling Division. Buying Division has no incentive to buy from Selling Division, because its net income will be the same if it buys from Selling Division or Outside Company. Selling Division's net income will stay the same whether it sells the 15,000 units to Buying Division or not. Negotiated Price Method If excess capacity exists, market price is a good transfer price. Overall Corporation benefits from the transfer of product between Selling Division and Buying Division. However, there is no incentive for Buying Division to buy from Selling Division. Buying Division net income will be the same regardless of which supplier it uses. In order to give some incentive for Buying Division to buy from Selling Division, a negotiated price may be the best price to use as a transfer price. How this transfer price affects the income of each division depends on the price that is negotiated. When the transfer price is negotiated, there is a maximum price above which Buying Division will not buy. There is also a minimum price below which Selling Division will not sell. The maximum price is equal to the The minimum transfer price can be calculated in one of two ways: Minimum Price = Market Price - Avoidable costs. This formula ensures that the selling division is no worse off by selling to another division. When this formula is used, the range for the desirable transfer price is stated as: (Market Price - Avoidable Cost)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts