Question: please help with this problem Suppose that many stocks are traded in the market and that it is possible to borrow at the risk-free raters.

please help with this problem

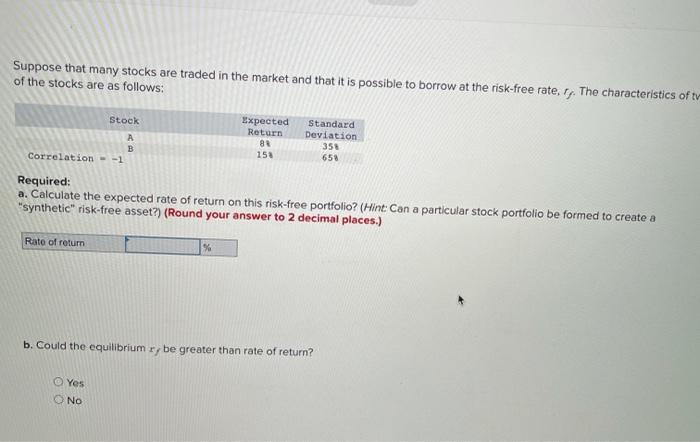

Suppose that many stocks are traded in the market and that it is possible to borrow at the risk-free raters. The characteristics of tv of the stocks are as follows: Stock B Correlation -- Expected Return 88 15 Standard Deviation 350 658 Required: a. Calculate the expected rate of return on this risk-free portfolio? (Hint: Can a particular stock portfolio be formed to create a "synthetic risk-free asset?) (Round your answer to 2 decimal places.) Rate of return % b. Could the equilibrium r; be greater than rate of return? Yes NO

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock