Question: please help with this question . please do it fast my homework is due in 1 hour Based on the following tales, what would be

please help with this question . please do it fast my homework is due in 1 hour

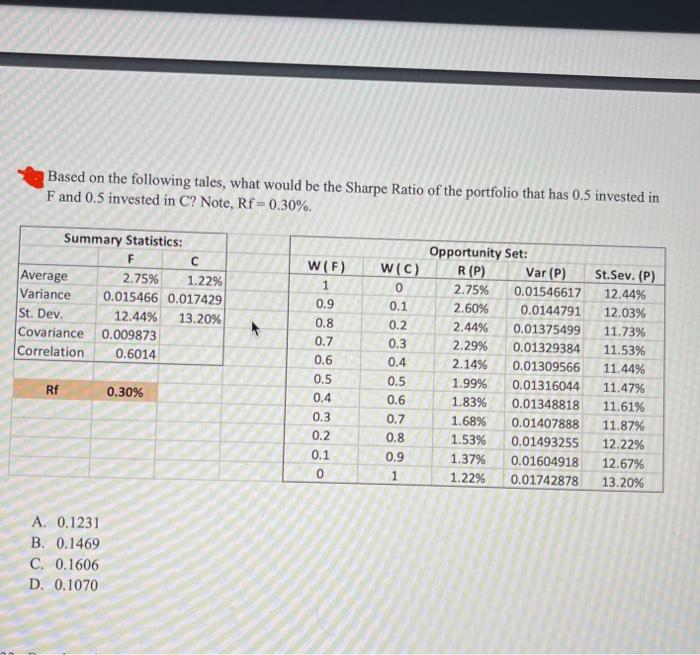

Based on the following tales, what would be the Sharpe Ratio of the portfolio that has 0.5 invested in F and 0.5 invested in C ? Note, Rf=0.30%. A. 0.1231 B. 0.1469 C. 0.1606 D. 0.1070

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock