Question: Please help with whatever you can do :) A U.S. firm holds an asset in France and faces the following scenario: Probability Spot rate P*

Please help with whatever you can do :)

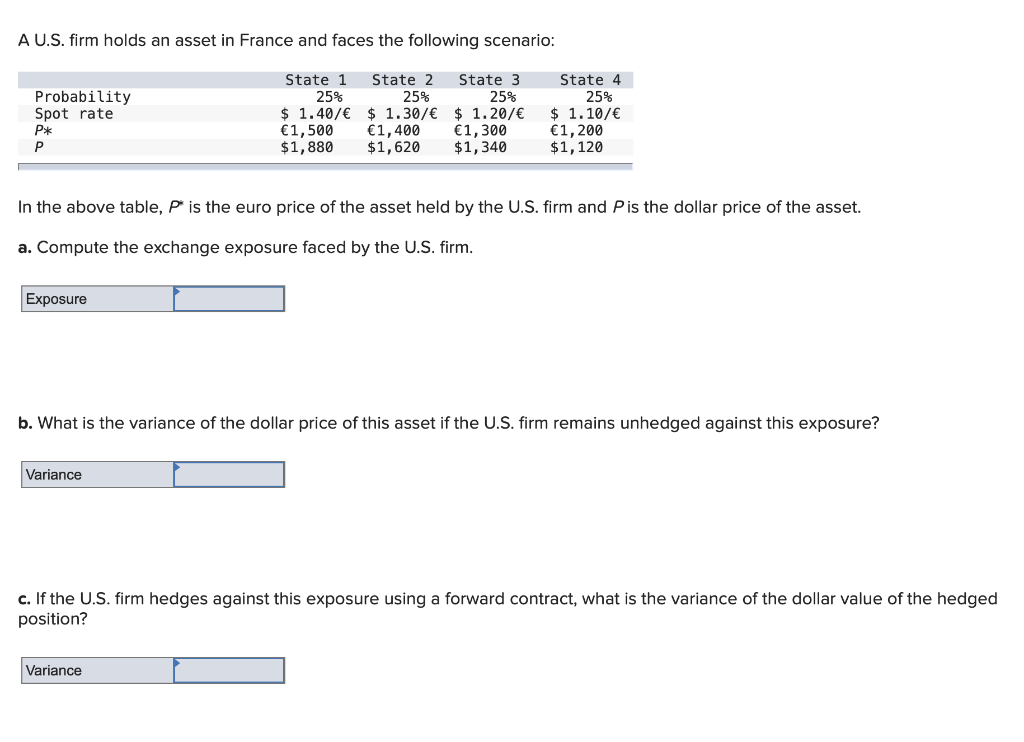

A U.S. firm holds an asset in France and faces the following scenario: Probability Spot rate P* P State 1 State 2 State 3 25% 25% 25% $ 1.40/ $ 1.30/ $ 1.20/ 1,500 1,400 1,300 $ 1,880 $1,620 $1,340 State 4 25% $ 1.10/ 1,200 $1,120 In the above table, P is the euro price of the asset held by the U.S. firm and P is the dollar price of the asset. a. Compute the exchange exposure faced by the U.S. firm. Exposure b. What is the variance of the dollar price of this asset if the U.S. firm remains unhedged against this exposure? Variance c. If the U.S. firm hedges against this exposure using a forward contract, what is the variance of the dollar value of the hedged position? Variance A U.S. firm holds an asset in France and faces the following scenario: Probability Spot rate P* P State 1 State 2 State 3 25% 25% 25% $ 1.40/ $ 1.30/ $ 1.20/ 1,500 1,400 1,300 $ 1,880 $1,620 $1,340 State 4 25% $ 1.10/ 1,200 $1,120 In the above table, P is the euro price of the asset held by the U.S. firm and P is the dollar price of the asset. a. Compute the exchange exposure faced by the U.S. firm. Exposure b. What is the variance of the dollar price of this asset if the U.S. firm remains unhedged against this exposure? Variance c. If the U.S. firm hedges against this exposure using a forward contract, what is the variance of the dollar value of the hedged position? Variance

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts