Question: Please hepl me to solve these problems. I will have same problems in the exam soon, but I don't really know how to solve it.

Please hepl me to solve these problems. I will have same problems in the exam soon, but I don't really know how to solve it.

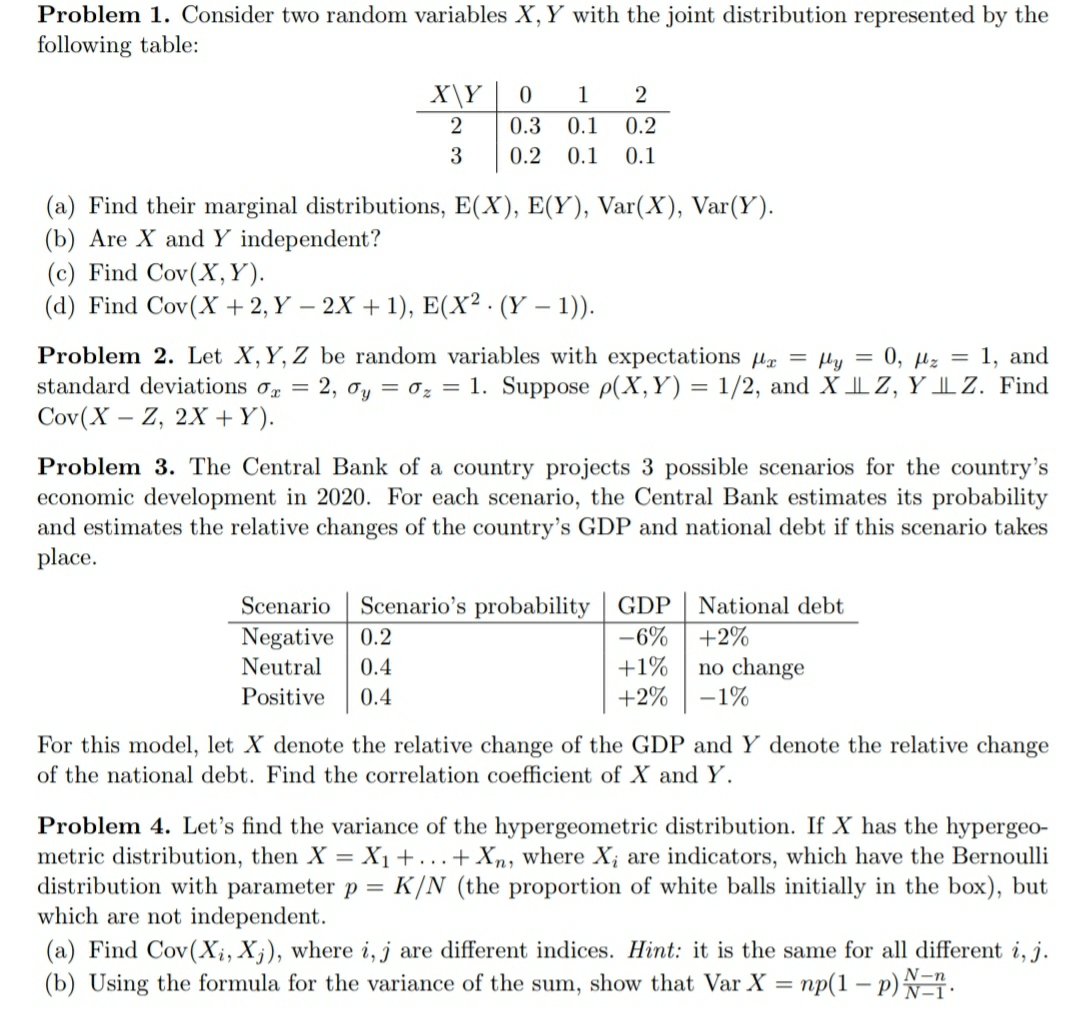

Problem 1. Consider two random variables X, Y with the joint distribution represented by the following table: 2 0.3 0.1 0.2 3 0.2 0.1 0.1 (a) Find their marginal distributions, E(X), E(Y), Var(X), Var(Y). (b) Are X and 1" independent? (c) Find Cov(X,Y). (d) Find Cov(X + 2, Y 2X + 1), E(X2 - (Y ~ 1)). Problem 2. Let X , Y,Z be random variables with expectations 3.5,,- = up = 0, p; = 1, and standard deviations on, = 2, try = or, = 1. Suppose p(X,Y) = 1/2, and XJLZ, YJLZ. Find Cov(X Z, 2X + Y). Problem 3. The Central Bank of a country projects 3 possible scenarios for the country's economic development in 2020. For each scenario, the Central Bank estimates its probability and estimates the relative changes of the country's GDP and national debt if this scenario takes place. Scenario Scenario's probability GDP National debt Negative +2% Neutral no change Positive 1% For this model, let X denote the relative change of the GDP and Y denote the relative change of the national debt. Find the correlation coefcient of X and 1". Problem 4. Let's nd the variance of the hypergeometric distribution. If X has the hypergeo- metric distribution, then X = X1 + . .. + Xn, where X, are indicators, which have the Bernoulli distribution with parameter p = K/N (the proportion of white balls initially in the box), but which are not independent. (9.) Find Cov(Xg, X 3-), where i, j are different indices. Hint: it is the same for all different 2', j. (b) Using the formula for the variance of the sum, show that VarX = np(1 QE

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts