Question: Please I need solution for this issue with all the details .please you can write the answer typing and not write by hand,so that I

Please I need solution for this issue with all the details .please you can write the answer typing and not write by hand,so that I can read and understand your answer clearly.I need step by step solution to the following this question asap.

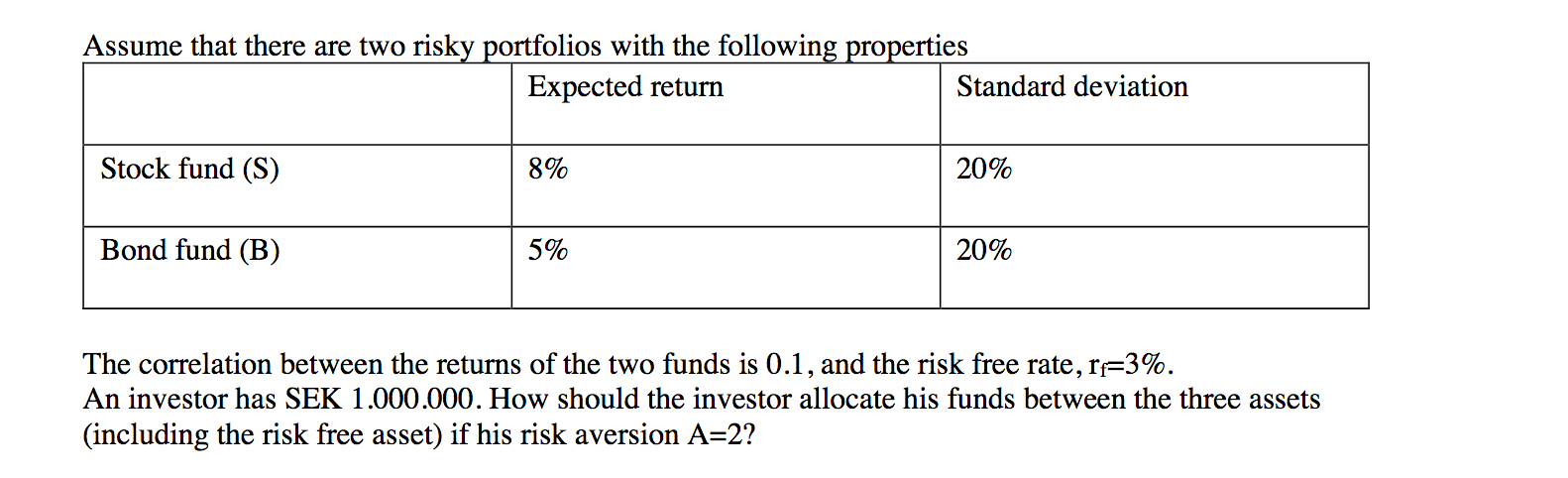

Assume that there are two risky portfolios with the following properties Expected return Standard deviation Stock fund (S) 8% 20% Bond fund (B) 5% 20% The correlation between the returns of the two funds is 0.1, and the risk free rate, rf=3%. An investor has SEK 1.000.000. How should the investor allocate his funds between the three assets (including the risk free asset) if his risk aversion A=2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock