Question: Please include formulas and work, preferably without using excel! Thank you very much! Problem 2. a) (5 pts) We have a financial market consisting of

Please include formulas and work, preferably without using excel! Thank you very much!

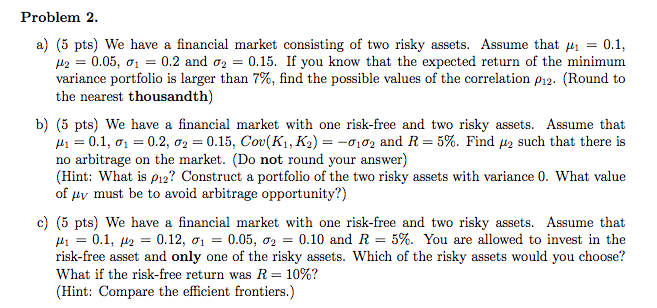

Problem 2. a) (5 pts) We have a financial market consisting of two risky assets. Assume that0.1, 2 = 0.05, | = 0.2 and 2 = 0.15. If you know that the expected return of the minimum variance portfolio is larger than 7%, find the possible values of the correlation P12. (Round to the nearest thousandth) b) (5 pts) We have a financial market with one risk-free and two risky assets. Assume that ,-0.1, 1-0.2, 2-0.15, Cov(KI, Ka)--ro, and R-5%. Find Ha such that there is no arbitrage on the market. (Do not round your answer) (Hint: What is p2? Construct a portfolio of the two risky assets with variance 0. What value of must be to avoid arbitrage opportunity?) c) (5 pts) We have a financial market with one risk-free and two risky assets. Assume that 1-0.1, 2-0.12, -0.05, 2-0.10 and R-5%. You are allowed to invest in the risk-free asset and only one of the risky assets. Which of the risky assets would you choose? What if the risk-free return was R-10%? Hint: Compare the efficient frontiers.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts