Question: Please let me know, what extra information is needed to answer the question. since that's the only info i was provided for the question. thanks.

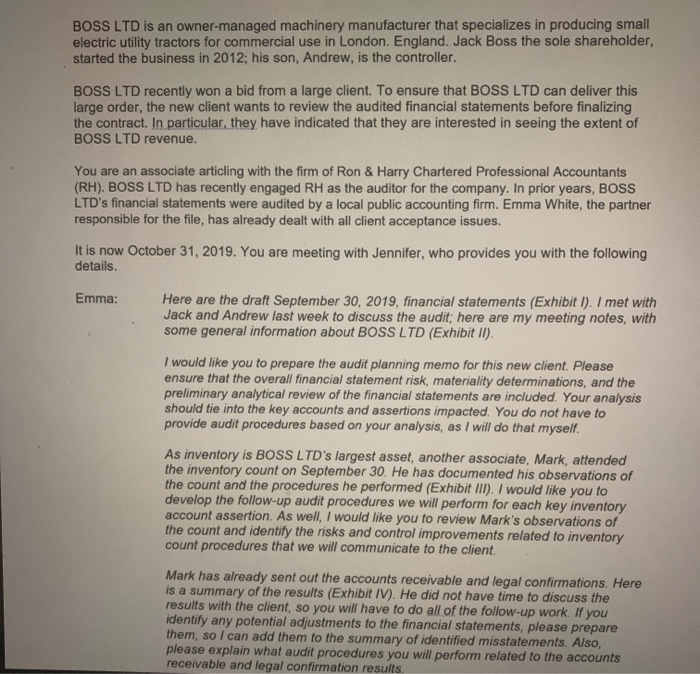

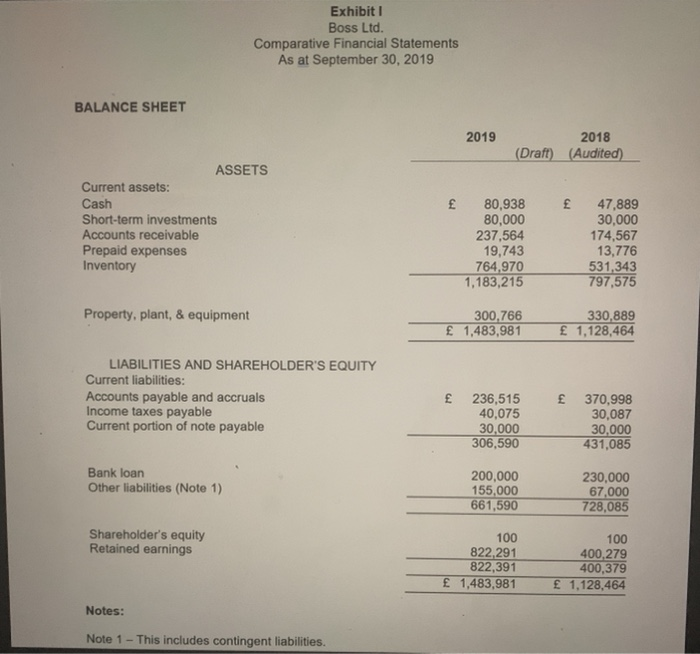

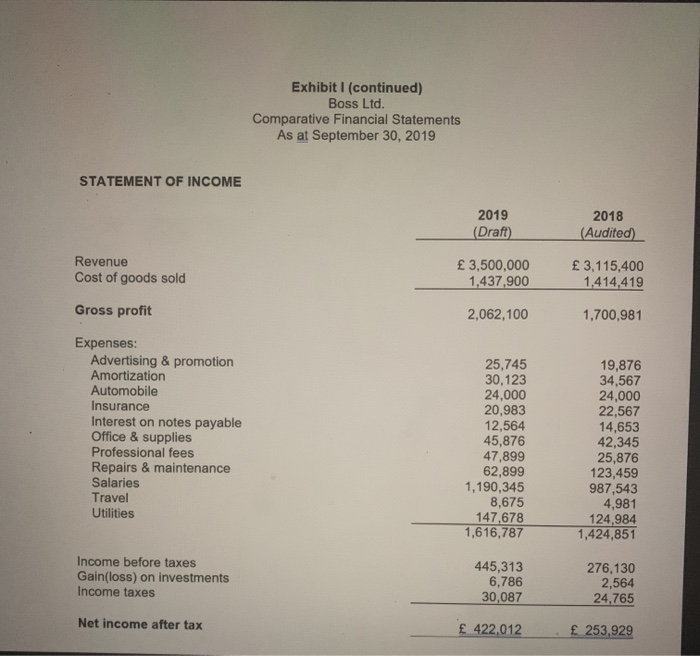

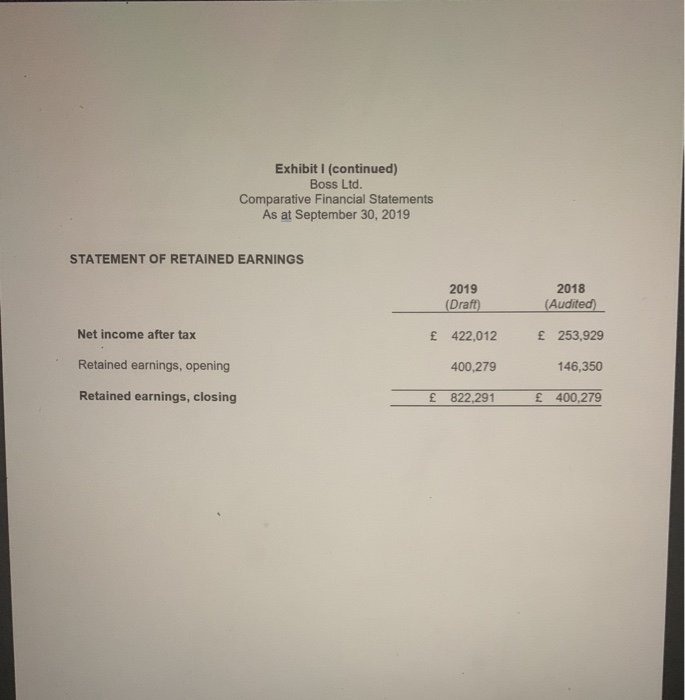

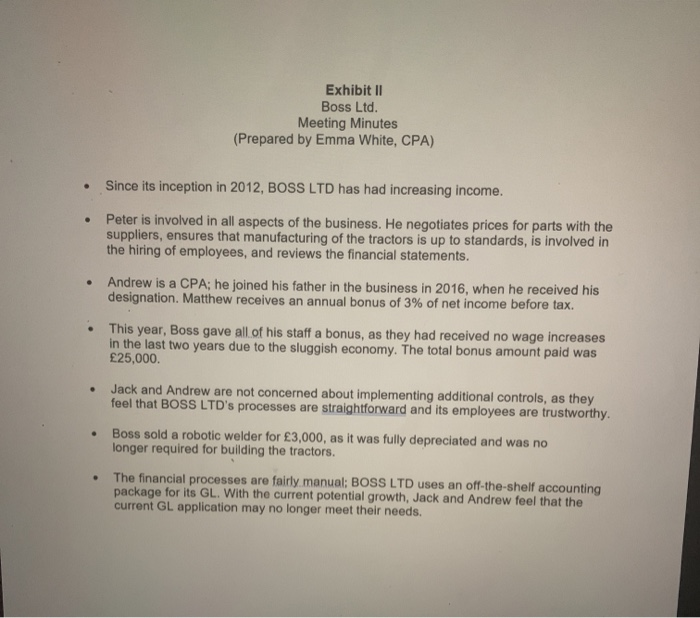

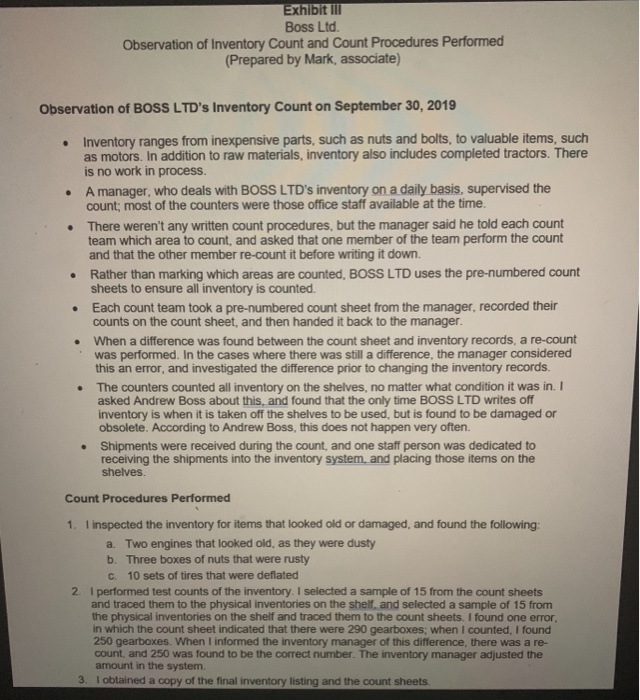

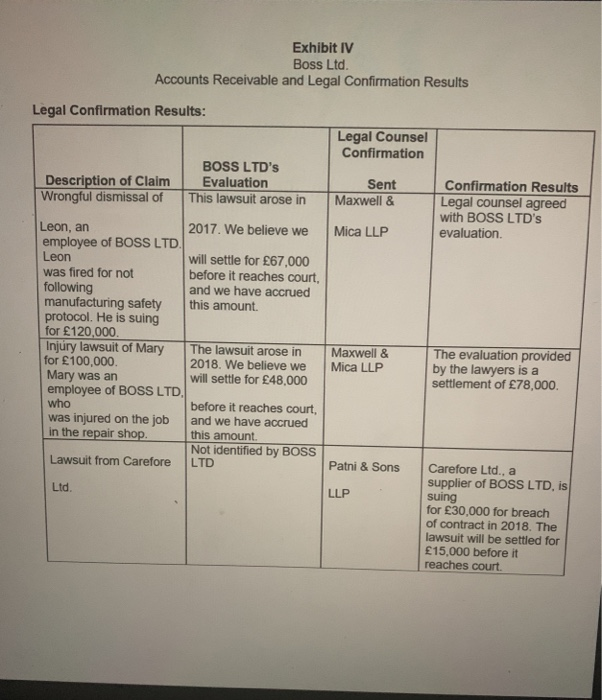

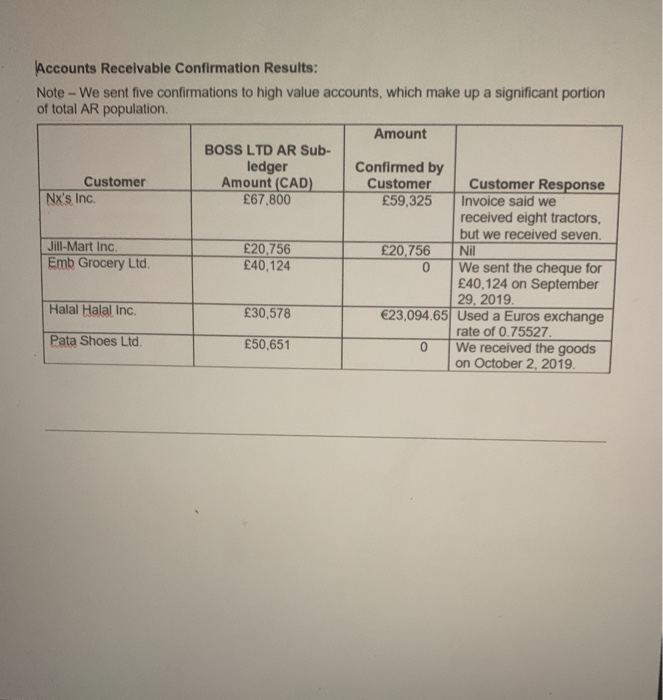

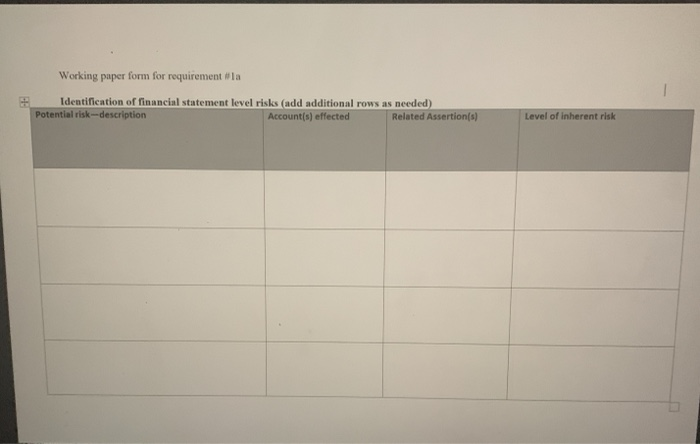

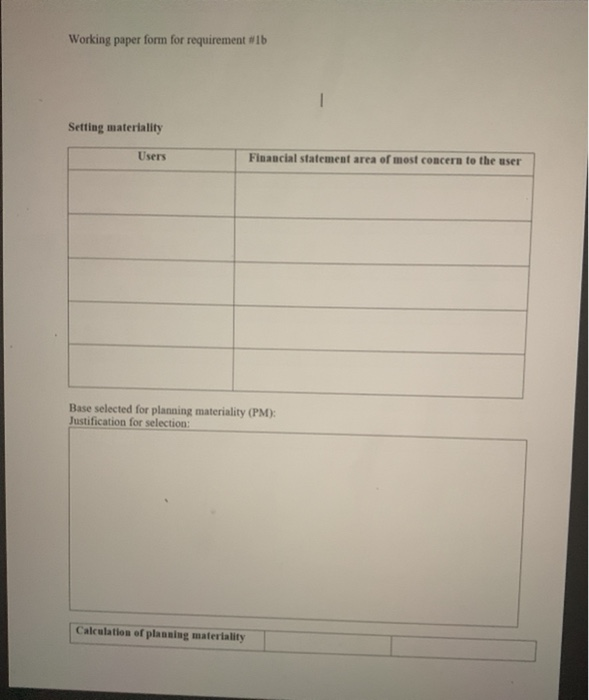

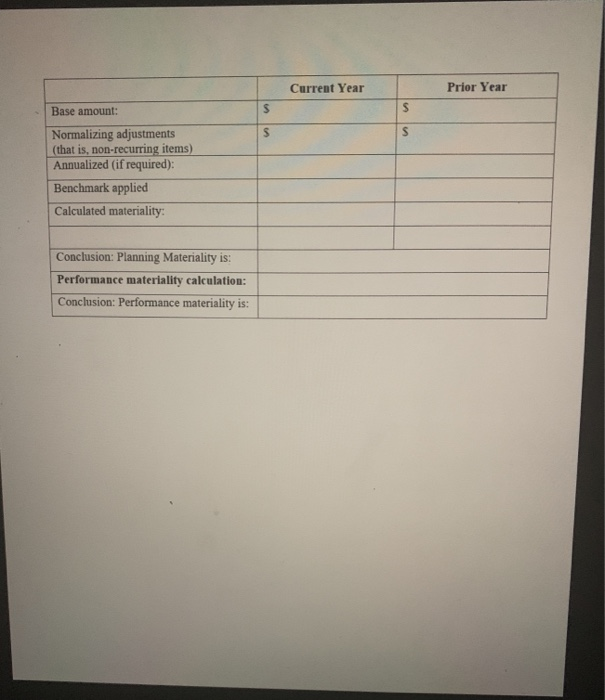

BOSS LTD is an owner-managed machinery manufacturer that specializes in producing small electric utility tractors for commercial use in London, England. Jack Boss the sole shareholder, started the business in 2012, his son, Andrew, is the controller. BOSS LTD recently won a bid from a large client. To ensure that BOSS LTD can deliver this large order, the new client wants to review the audited financial statements before finalizing the contract. In particular, they have indicated that they are interested in seeing the extent of BOSS LTD revenue. You are an associate articling with the firm of Ron & Harry Chartered Professional Accountants (RH). BOSS LTD has recently engaged RH as the auditor for the company. In prior years, BOSS LTD's financial statements were audited by a local public accounting firm. Emma White, the partner responsible for the file, has already dealt with all client acceptance issues. It is now October 31, 2019. You are meeting with Jennifer, who provides you with the following details. Emma: Here are the draft September 30, 2019, financial statements (Exhibit :). I met with Jack and Andrew last week to discuss the audit; here are my meeting notes, with some general information about BOSS LTD (Exhibit II). I would like you to prepare the audit planning memo for this new client. Please ensure that the overall financial statement risk, materiality determinations, and the preliminary analytical review of the financial statements are included. Your analysis should tie into the key accounts and assertions impacted. You do not have to provide audit procedures based on your analysis, as I will do that myself. As inventory is BOSS LTD's largest asset, another associate, Mark, attended the inventory count on September 30. He has documented his observations of the count and the procedures he performed (Exhibit III). I would like you to develop the follow-up audit procedures we will perform for each key inventory account assertion. As well, I would like you to review Mark's observations of the count and identify the risks and control improvements related to inventory count procedures that we will communicate to the client. Mark has already sent out the accounts receivable and legal confirmations. Here is a summary of the results (Exhibit IV). He did not have time to discuss the results with the client, so you will have to do all of the follow-up work. If you identify any potential adjustments to the financial statements, please prepare them, so I can add them to the summary of identified misstatements. Also, please explain what audit procedures you will perform related to the accounts receivable and legal confirmation results. Exhibiti Boss Ltd. Comparative Financial Statements As at September 30, 2019 BALANCE SHEET 2019 2018 (Draft) (Audited) ASSETS Current assets: Cash Short-term investments Accounts receivable Prepaid expenses Inventory 80,938 80,000 237,564 19,743 764,970 1,183,215 47,889 30,000 174,567 13,776 531,343 797,575 Property, plant, & equipment 300,766 1,483,981 330,889 1,128,464 LIABILITIES AND SHAREHOLDER'S EQUITY Current liabilities: Accounts payable and accruals Income taxes payable Current portion of note payable 236,515 40,075 30,000 306,590 370,998 30,087 30,000 431,085 Bank loan Other liabilities (Note 1) 200,000 155,000 661,590 230,000 67,000 728,085 Shareholder's equity Retained earnings 100 822,291 822,391 1,483,981 100 400,279 400,379 1,128,464 Notes: Note 1 - This includes contingent liabilities. Exhibit I (continued) Boss Ltd. Comparative Financial Statements As at September 30, 2019 STATEMENT OF INCOME 2019 (Draft) 2018 (Audited) Revenue Cost of goods sold 3,500,000 1,437,900 3,115,400 1.414,419 Gross profit 2,062,100 1,700,981 Expenses: Advertising & promotion Amortization Automobile Insurance Interest on notes payable Office & supplies Professional fees Repairs & maintenance Salaries Travel Utilities 25,745 30,123 24,000 20,983 12,564 45,876 47,899 62,899 1,190,345 8,675 147,678 1,616,787 19,876 34,567 24,000 22,567 14,653 42,345 25,876 123,459 987,543 4,981 124,984 1,424,851 Income before taxes Gain(loss) on investments Income taxes 445,313 6,786 30,087 276,130 2,564 24,765 Net income after tax 422,012 253,929 Exhibit I (continued) Boss Ltd. Comparative Financial Statements As at September 30, 2019 STATEMENT OF RETAINED EARNINGS 2019 (Draft) 2018 (Audited) Net income after tax 422.012 253,929 Retained earnings, opening 400,279 146,350 Retained earnings, closing 822,291 400,279 Exhibit II Boss Ltd. Meeting Minutes (Prepared by Emma White, CPA) Since its inception in 2012, BOSS LTD has had increasing income. . Peter is involved in all aspects of the business. He negotiates prices for parts with the suppliers, ensures that manufacturing of the tractors is up to standards, is involved in the hiring of employees, and reviews the financial statements. Andrew is a CPA; he joined his father in the business in 2016, when he received his designation. Matthew receives an annual bonus of 3% of net income before tax. This year, Boss gave all of his staff a bonus, as they had received no wage increases in the last two years due to the sluggish economy. The total bonus amount paid was 25,000 Jack and Andrew are not concerned about implementing additional controls, as they feel that BOSS LTD's processes are straightforward and its employees are trustworthy. Boss sold a robotic welder for 3,000, as it was fully depreciated and was no longer required for building the tractors. The financial processes are fairly manual; BOSS LTD uses an off-the-shelf accounting package for its GL. With the current potential growth, Jack and Andrew feel that the current GL application may no longer meet their needs. Exhibit II Boss Ltd. Observation of Inventory Count and Count Procedures Performed (Prepared by Mark, associate) Observation of BOSS LTD's Inventory Count on September 30, 2019 . Inventory ranges from inexpensive parts, such as nuts and bolts, to valuable items, such as motors. In addition to raw materials, inventory also includes completed tractors. There is no work in process. A manager, who deals with BOSS LTD's inventory on a daily basis, supervised the count; most of the counters were those office staff available at the time. There weren't any written count procedures, but the manager said he told each count team which area to count, and asked that one member of the team perform the count and that the other member re-count it before writing it down. Rather than marking which areas are counted, BOSS LTD uses the pre-numbered count sheets to ensure all inventory is counted. Each count team took a pre-numbered count sheet from the manager, recorded their counts on the count sheet, and then handed it back to the manager. When a difference was found between the count sheet and inventory records, a re-count was performed. In the cases where there was still a difference, the manager considered this an error, and investigated the difference prior to changing the inventory records. The counters counted all inventory on the shelves, no matter what condition it was in. I asked Andrew Boss about this, and found that the only time BOSS LTD writes off inventory is when it is taken off the shelves to be used, but is found to be damaged or obsolete. According to Andrew Boss, this does not happen very often. Shipments were received during the count, and one staff person was dedicated to receiving the shipments into the inventory system, and placing those items on the shelves Count Procedures Performed 1. inspected the inventory for items that looked old or damaged, and found the following: a. Two engines that looked old, as they were dusty b. Three boxes of nuts that were rusty C. 10 sets of tires that were deflated 2. I performed test counts of the inventory. I selected a sample of 15 from the count sheets and traced them to the physical inventories on the shelf, and selected a sample of 15 from the physical inventories on the shelf and traced them to the count sheets. I found one error, in which the count sheet indicated that there were 290 gearboxes; when I counted, I found 250 gearboxes. When I informed the inventory manager of this difference, there was a re- count, and 250 was found to be the correct number. The inventory manager adjusted the amount in the system. 3. I obtained a copy of the final inventory listing and the count sheets Exhibit IV Boss Ltd. Accounts Receivable and Legal Confirmation Results Legal Confirmation Results: Legal Counsel Confirmation Description of Claim Wrongful dismissal of BOSS LTD's Evaluation This lawsuit arose in Sent Maxwell & Confirmation Results Legal counsel agreed with BOSS LTD's evaluation Mica LLP Leon, an 2017. We believe we employee of BOSS LTD. Leon will settle for 67,000 was fired for not before it reaches court, following and we have accrued manufacturing safety this amount protocol. He is suing for 120.000 Injury lawsuit of Mary The lawsuit arose in for 100,000 2018. We believe we Mary was an will settle for 48,000 employee of BOSS LTD. who before it reaches court, was injured on the job and we have accrued in the repair shop this amount Not identified by BOSS Lawsuit from Carefore LTD Maxwell & Mica LLP The evaluation provided by the lawyers is a settlement of 78,000. Patni & Sons Ltd LLP Carefore Ltd., a supplier of BOSS LTD, is suing for 30,000 for breach of contract in 2018. The lawsuit will be settled for 15,000 before it reaches court. Accounts Receivable Confirmation Results: Note - We sent five confirmations to high value accounts, which make up a significant portion of total AR population. Amount BOSS LTD AR Sub- ledger Confirmed by Customer Amount (CAD) Customer Customer Response Nx's Inc. 67,800 59,325 Invoice said we received eight tractors, but we received seven. Jill-Mart Inc. 20,756 20,756 Nil Emb Grocery Ltd 40,124 0 We sent the cheque for 40,124 on September 29, 2019 Halal Halal Inc. 30,578 23,094.65 Used a Euros exchange rate of 0.75527. Pata Shoes Ltd 50,651 0 We received the goods on October 2, 2019 1 Ignore PST, GST & HST 1) Prepare an audit planning memo for the audit working paper files and include: a. Assessment of overall risk at the financial statement level (pervasive risks). Include the risk factor and any associated factors that may decrease the magnitude of risk. Use the attached form to identify the risk, the accounts and transaction level assertions that may be affected and your assessment. In your memo, summarize your overall risk assessment and explain your reasoning. (hint: refer to entity-level controls covered in Chapter 7) b. Calculate materiality (use the attached form). Identify the users and their needs. Determine an appropriate base and performance materiality. Summarize your conclusions on materiality in the memo. 2) Perform the preliminary analytical procedures based on the draft financial statements. Calculate gross profit margin (%), current ratio, a'r turnover and inventory turnover. Interpret your findings and identify any impact on the audit (additional procedures that should be performed, etc.) 3) Identify at least five control deficiencies in the client's inventory count procedures along with implications and recommendations to improve. Summarize your findings in a draft memo to the client. 4) Identify substantive procedures to gather evidence for valuation, existence, completeness, cut-off and rights and obligations assertions related to the inventory account balance. (hint: given the control deficiencies identified, what other tests should the auditor perform to gather sufficient evidence). Summarize your findings in a separate memo to the audit engagement partner. 5) Analyze the legal and accounts receivable confirmations and identify proposed adjustments to account balances along with any other procedures that should be performed to gather additional information related to these confirmations. (hint: you will be drawing on your understanding of how assets and liabilities are properly measured and disclosed). Summarize your adjustments in a separate memo to the audit engagement partner. Working paper form for requirement #la Identification of financial statement level risks (add additional rows as needed) Potential risk-description Account(s) effected Related Assertion(s) Level of inherent risk Working paper form for requirement #1b Setting materiality Users Financial statement area of most concern to the user Base selected for planning materiality (PM): Justification for selection: Calculation of planning materiality Current Year Prior Year Base amount: S S S Normalizing adjustments (that is, non-recurring items) Annualized (if required): Benchmark applied Calculated materiality: Conclusion: Planning Materiality is: Performance materiality calculation: Conclusion: Performance materiality is: BOSS LTD is an owner-managed machinery manufacturer that specializes in producing small electric utility tractors for commercial use in London, England. Jack Boss the sole shareholder, started the business in 2012, his son, Andrew, is the controller. BOSS LTD recently won a bid from a large client. To ensure that BOSS LTD can deliver this large order, the new client wants to review the audited financial statements before finalizing the contract. In particular, they have indicated that they are interested in seeing the extent of BOSS LTD revenue. You are an associate articling with the firm of Ron & Harry Chartered Professional Accountants (RH). BOSS LTD has recently engaged RH as the auditor for the company. In prior years, BOSS LTD's financial statements were audited by a local public accounting firm. Emma White, the partner responsible for the file, has already dealt with all client acceptance issues. It is now October 31, 2019. You are meeting with Jennifer, who provides you with the following details. Emma: Here are the draft September 30, 2019, financial statements (Exhibit :). I met with Jack and Andrew last week to discuss the audit; here are my meeting notes, with some general information about BOSS LTD (Exhibit II). I would like you to prepare the audit planning memo for this new client. Please ensure that the overall financial statement risk, materiality determinations, and the preliminary analytical review of the financial statements are included. Your analysis should tie into the key accounts and assertions impacted. You do not have to provide audit procedures based on your analysis, as I will do that myself. As inventory is BOSS LTD's largest asset, another associate, Mark, attended the inventory count on September 30. He has documented his observations of the count and the procedures he performed (Exhibit III). I would like you to develop the follow-up audit procedures we will perform for each key inventory account assertion. As well, I would like you to review Mark's observations of the count and identify the risks and control improvements related to inventory count procedures that we will communicate to the client. Mark has already sent out the accounts receivable and legal confirmations. Here is a summary of the results (Exhibit IV). He did not have time to discuss the results with the client, so you will have to do all of the follow-up work. If you identify any potential adjustments to the financial statements, please prepare them, so I can add them to the summary of identified misstatements. Also, please explain what audit procedures you will perform related to the accounts receivable and legal confirmation results. Exhibiti Boss Ltd. Comparative Financial Statements As at September 30, 2019 BALANCE SHEET 2019 2018 (Draft) (Audited) ASSETS Current assets: Cash Short-term investments Accounts receivable Prepaid expenses Inventory 80,938 80,000 237,564 19,743 764,970 1,183,215 47,889 30,000 174,567 13,776 531,343 797,575 Property, plant, & equipment 300,766 1,483,981 330,889 1,128,464 LIABILITIES AND SHAREHOLDER'S EQUITY Current liabilities: Accounts payable and accruals Income taxes payable Current portion of note payable 236,515 40,075 30,000 306,590 370,998 30,087 30,000 431,085 Bank loan Other liabilities (Note 1) 200,000 155,000 661,590 230,000 67,000 728,085 Shareholder's equity Retained earnings 100 822,291 822,391 1,483,981 100 400,279 400,379 1,128,464 Notes: Note 1 - This includes contingent liabilities. Exhibit I (continued) Boss Ltd. Comparative Financial Statements As at September 30, 2019 STATEMENT OF INCOME 2019 (Draft) 2018 (Audited) Revenue Cost of goods sold 3,500,000 1,437,900 3,115,400 1.414,419 Gross profit 2,062,100 1,700,981 Expenses: Advertising & promotion Amortization Automobile Insurance Interest on notes payable Office & supplies Professional fees Repairs & maintenance Salaries Travel Utilities 25,745 30,123 24,000 20,983 12,564 45,876 47,899 62,899 1,190,345 8,675 147,678 1,616,787 19,876 34,567 24,000 22,567 14,653 42,345 25,876 123,459 987,543 4,981 124,984 1,424,851 Income before taxes Gain(loss) on investments Income taxes 445,313 6,786 30,087 276,130 2,564 24,765 Net income after tax 422,012 253,929 Exhibit I (continued) Boss Ltd. Comparative Financial Statements As at September 30, 2019 STATEMENT OF RETAINED EARNINGS 2019 (Draft) 2018 (Audited) Net income after tax 422.012 253,929 Retained earnings, opening 400,279 146,350 Retained earnings, closing 822,291 400,279 Exhibit II Boss Ltd. Meeting Minutes (Prepared by Emma White, CPA) Since its inception in 2012, BOSS LTD has had increasing income. . Peter is involved in all aspects of the business. He negotiates prices for parts with the suppliers, ensures that manufacturing of the tractors is up to standards, is involved in the hiring of employees, and reviews the financial statements. Andrew is a CPA; he joined his father in the business in 2016, when he received his designation. Matthew receives an annual bonus of 3% of net income before tax. This year, Boss gave all of his staff a bonus, as they had received no wage increases in the last two years due to the sluggish economy. The total bonus amount paid was 25,000 Jack and Andrew are not concerned about implementing additional controls, as they feel that BOSS LTD's processes are straightforward and its employees are trustworthy. Boss sold a robotic welder for 3,000, as it was fully depreciated and was no longer required for building the tractors. The financial processes are fairly manual; BOSS LTD uses an off-the-shelf accounting package for its GL. With the current potential growth, Jack and Andrew feel that the current GL application may no longer meet their needs. Exhibit II Boss Ltd. Observation of Inventory Count and Count Procedures Performed (Prepared by Mark, associate) Observation of BOSS LTD's Inventory Count on September 30, 2019 . Inventory ranges from inexpensive parts, such as nuts and bolts, to valuable items, such as motors. In addition to raw materials, inventory also includes completed tractors. There is no work in process. A manager, who deals with BOSS LTD's inventory on a daily basis, supervised the count; most of the counters were those office staff available at the time. There weren't any written count procedures, but the manager said he told each count team which area to count, and asked that one member of the team perform the count and that the other member re-count it before writing it down. Rather than marking which areas are counted, BOSS LTD uses the pre-numbered count sheets to ensure all inventory is counted. Each count team took a pre-numbered count sheet from the manager, recorded their counts on the count sheet, and then handed it back to the manager. When a difference was found between the count sheet and inventory records, a re-count was performed. In the cases where there was still a difference, the manager considered this an error, and investigated the difference prior to changing the inventory records. The counters counted all inventory on the shelves, no matter what condition it was in. I asked Andrew Boss about this, and found that the only time BOSS LTD writes off inventory is when it is taken off the shelves to be used, but is found to be damaged or obsolete. According to Andrew Boss, this does not happen very often. Shipments were received during the count, and one staff person was dedicated to receiving the shipments into the inventory system, and placing those items on the shelves Count Procedures Performed 1. inspected the inventory for items that looked old or damaged, and found the following: a. Two engines that looked old, as they were dusty b. Three boxes of nuts that were rusty C. 10 sets of tires that were deflated 2. I performed test counts of the inventory. I selected a sample of 15 from the count sheets and traced them to the physical inventories on the shelf, and selected a sample of 15 from the physical inventories on the shelf and traced them to the count sheets. I found one error, in which the count sheet indicated that there were 290 gearboxes; when I counted, I found 250 gearboxes. When I informed the inventory manager of this difference, there was a re- count, and 250 was found to be the correct number. The inventory manager adjusted the amount in the system. 3. I obtained a copy of the final inventory listing and the count sheets Exhibit IV Boss Ltd. Accounts Receivable and Legal Confirmation Results Legal Confirmation Results: Legal Counsel Confirmation Description of Claim Wrongful dismissal of BOSS LTD's Evaluation This lawsuit arose in Sent Maxwell & Confirmation Results Legal counsel agreed with BOSS LTD's evaluation Mica LLP Leon, an 2017. We believe we employee of BOSS LTD. Leon will settle for 67,000 was fired for not before it reaches court, following and we have accrued manufacturing safety this amount protocol. He is suing for 120.000 Injury lawsuit of Mary The lawsuit arose in for 100,000 2018. We believe we Mary was an will settle for 48,000 employee of BOSS LTD. who before it reaches court, was injured on the job and we have accrued in the repair shop this amount Not identified by BOSS Lawsuit from Carefore LTD Maxwell & Mica LLP The evaluation provided by the lawyers is a settlement of 78,000. Patni & Sons Ltd LLP Carefore Ltd., a supplier of BOSS LTD, is suing for 30,000 for breach of contract in 2018. The lawsuit will be settled for 15,000 before it reaches court. Accounts Receivable Confirmation Results: Note - We sent five confirmations to high value accounts, which make up a significant portion of total AR population. Amount BOSS LTD AR Sub- ledger Confirmed by Customer Amount (CAD) Customer Customer Response Nx's Inc. 67,800 59,325 Invoice said we received eight tractors, but we received seven. Jill-Mart Inc. 20,756 20,756 Nil Emb Grocery Ltd 40,124 0 We sent the cheque for 40,124 on September 29, 2019 Halal Halal Inc. 30,578 23,094.65 Used a Euros exchange rate of 0.75527. Pata Shoes Ltd 50,651 0 We received the goods on October 2, 2019 1 Ignore PST, GST & HST 1) Prepare an audit planning memo for the audit working paper files and include: a. Assessment of overall risk at the financial statement level (pervasive risks). Include the risk factor and any associated factors that may decrease the magnitude of risk. Use the attached form to identify the risk, the accounts and transaction level assertions that may be affected and your assessment. In your memo, summarize your overall risk assessment and explain your reasoning. (hint: refer to entity-level controls covered in Chapter 7) b. Calculate materiality (use the attached form). Identify the users and their needs. Determine an appropriate base and performance materiality. Summarize your conclusions on materiality in the memo. 2) Perform the preliminary analytical procedures based on the draft financial statements. Calculate gross profit margin (%), current ratio, a'r turnover and inventory turnover. Interpret your findings and identify any impact on the audit (additional procedures that should be performed, etc.) 3) Identify at least five control deficiencies in the client's inventory count procedures along with implications and recommendations to improve. Summarize your findings in a draft memo to the client. 4) Identify substantive procedures to gather evidence for valuation, existence, completeness, cut-off and rights and obligations assertions related to the inventory account balance. (hint: given the control deficiencies identified, what other tests should the auditor perform to gather sufficient evidence). Summarize your findings in a separate memo to the audit engagement partner. 5) Analyze the legal and accounts receivable confirmations and identify proposed adjustments to account balances along with any other procedures that should be performed to gather additional information related to these confirmations. (hint: you will be drawing on your understanding of how assets and liabilities are properly measured and disclosed). Summarize your adjustments in a separate memo to the audit engagement partner. Working paper form for requirement #la Identification of financial statement level risks (add additional rows as needed) Potential risk-description Account(s) effected Related Assertion(s) Level of inherent risk Working paper form for requirement #1b Setting materiality Users Financial statement area of most concern to the user Base selected for planning materiality (PM): Justification for selection: Calculation of planning materiality Current Year Prior Year Base amount: S S S Normalizing adjustments (that is, non-recurring items) Annualized (if required): Benchmark applied Calculated materiality: Conclusion: Planning Materiality is: Performance materiality calculation: Conclusion: Performance materiality is

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts