Question: please make final answer clear, thank you! Consider the following spot rate curve: -6-month spot rate: 3%. - 12 -month spot rate: 5%. - 18

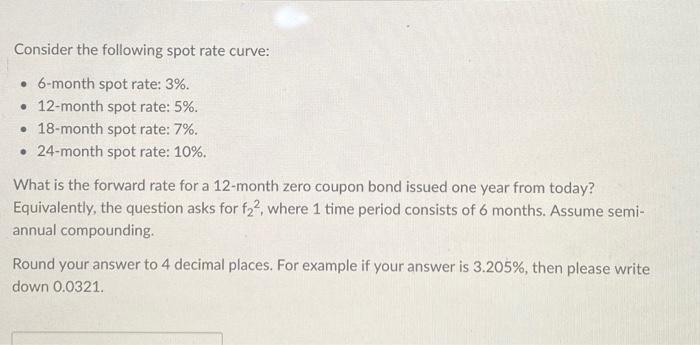

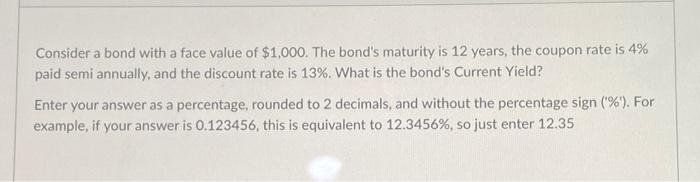

Consider the following spot rate curve: -6-month spot rate: 3%. - 12 -month spot rate: 5%. - 18 -month spot rate: 7%. - 24-month spot rate: 10%. What is the forward rate for a 12 -month zero coupon bond issued one year from today? Equivalently, the question asks for f22, where 1 time period consists of 6 months. Assume semiannual compounding. Round your answer to 4 decimal places. For example if your answer is 3.205%, then please write down 0.0321 . Consider a bond with a face value of $1,000. The bond's maturity is 12 years, the coupon rate is 4% paid semi annually, and the discount rate is 13%. What is the bond's Current Yield? Enter your answer as a percentage, rounded to 2 decimals, and without the percentage sign ('\%'). For example, if your answer is 0.123456 , this is equivalent to 12.3456%, so just enter 12.35

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts