Question: Please make sure your answer is correct! Please do not copy other wrong answers There are three risky assets with rates of return r1,r2, and

Please make sure your answer is correct! Please do not copy other wrong answers

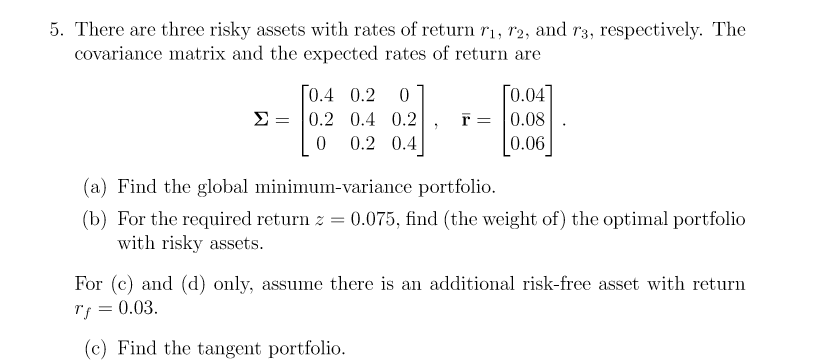

There are three risky assets with rates of return r1,r2, and r3, respectively. The covariance matrix and the expected rates of return are =0.40.200.20.40.200.20.4,r=0.040.080.06 (a) Find the global minimum-variance portfolio. (b) For the required return z=0.075, find (the weight of) the optimal portfolio with risky assets. For (c) and (d) only, assume there is an additional risk-free asset with return rf=0.03. (c) Find the tangent portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock