Question: Please note A is incorrect let me know if you can find out which is the truly correct awnser Given the three Call prices on

Please note A is incorrect let me know if you can find out which is the truly correct awnser

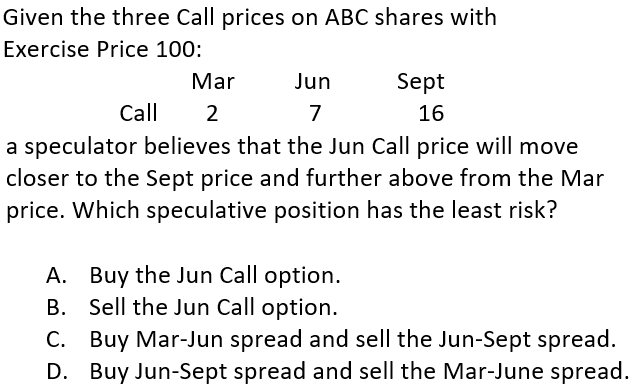

Given the three Call prices on ABC shares with Exercise Price 100: a speculator believes that the Jun Call price will move closer to the Sept price and further above from the Mar price. Which speculative position has the least risk? A. Buy the Jun Call option. B. Sell the Jun Call option. C. Buy Mar-Jun spread and sell the Jun-Sept spread. D. Buy Jun-Sept spread and sell the Mar-June spread

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock