Question: Please only answer questions # 3, 5, and 6 . Thank you. CASE 2.2 FLIGHT TRANSPORTATION CORPORATION In January 1982, Charles Anne picked up his

Please only answer questions # 3, 5, and 6. Thank you.

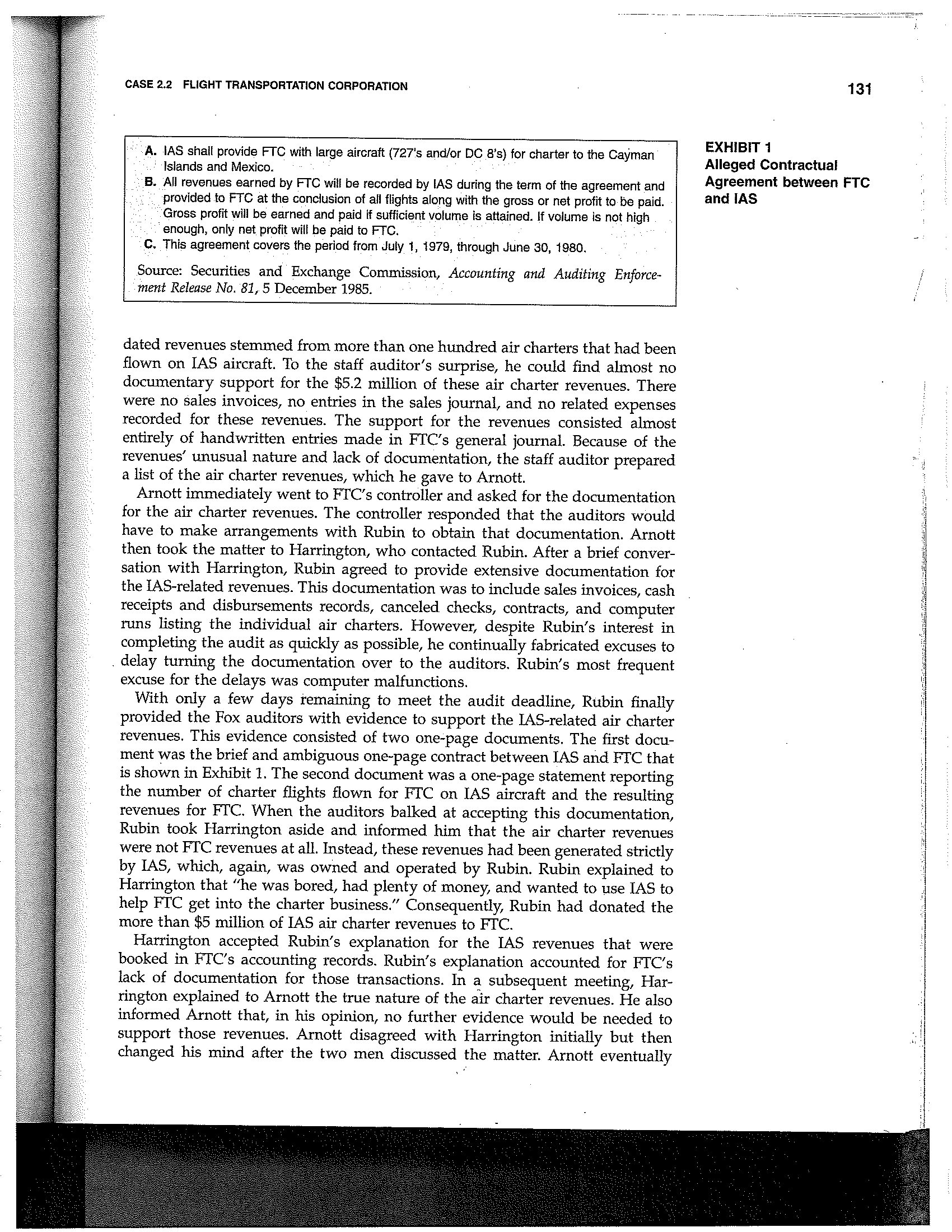

CASE 2.2 FLIGHT TRANSPORTATION CORPORATION In January 1982, Charles Anne picked up his phone and called the Federal Bureau of Investigation (FBI).1 Anne informed the FBI of a large-scale fraud being perpetrated by his former employer. Until 1981, Anne had worked for Flight Transportation Corporation (FTC), an aviation company based in Eden Prairie, Minnesota. FTC's principal line Of business was executive and group air charters. In 1980 and 1981, the rapidly growing company reported revenues Of $8 million and $24.8 million, respectiveiy. FTC's dramatic growth caught the attention of thousands of investors. These investors were particularly impressed by FTC's strong Operating results in the face of a nationwide recession. Unfortunately for these investors, most of FI'C's revenues were fabricated by its executives. Similarly, several million dollars of assets reported in the company' s 1980 and 1981 baiance sheets did not exist. From 1979 through 1982, FTC executives used the company' s bogus nancial statements to raise more than $32 miilion of capital in three securities Offerings to the pubiic. Several million dollars of these funds were diverted by the executives for their personal use. fior example, the company's president apparently nanced his expensive hobby, collecting vintage cars, by tapping the company' s bank accounts. In lune 1982, FTC was preparing to sell an additional $24 million of securities. However, as a result of Aune's tip and a secret six-month investigation by the FBI, the Securities and Exchange Commission (SEC) shut down FTC's _ operations. A federal judge then appointed a receiver to take custody Of the company' s assets. Over the next several months, press reports of the FTC fraud shocked investors who had purchased the company' s securities on the basis of its impressive nancial statements. Almost immediately, the underwriting firms that 1. Most of the facts of this case and the quotations, unless indicated otherwise, were drawn from the following source: Securities and Exchange Commission, Accounting and Auditing Enforcement Release No. 81, 5 December 1985. 129 136 SECYION TWO AUDITS OF HIGH-RISK ACCOUNTS AND INTERNAL CONTROL ISSUES had managed FTC's securities offerings came under fire. An executive of one of these rms responded to this criticism. \"I don't see this as embarrassing to our firm at all. Underwriters aren't auditors.\"2 Predictably, the press then turned to FTC's auditors, Fox 8: Company, for an explanation. John Harrington, a senior partner with Fox $1: Company, defended the 1980 and 1981 audits of FTC for which he had served as the audit engagement partner. We're not the guardians of the world. It's the con artists who should be punished. Besides, if we go into every client' 3 ofce with our eyes wide open, saying, "there's a crime in here somewhere,\" nobody is going to hire 115.3 M Fox's 1980 AUDIT or FTC The Minneapolis office of Fox ti: Company, the thirteenthlargest accounting firm in the nation at the time, acquired FTC as an audit client in March 1980. in prior years, the company had been audited by a sole practitioner. In addition to Harrington, the audit engagement team assigned to the 1980 and 1981 Fl'C audits included an audit manager, Gregory Arnott, and three staff auditors. The . fieldwork in both audits was supervised by Arnott. The 1980 FTC audit was the first engagement on which Arnott had served as an audit manager, since he had been promoted to that position shortly before the audit began. In his previous eight years with Fox & Company, Arnott had been assigned to only one audit of a public company. Harrington had been a partner with Fox & Company since 1975 and had served for a time as the managing partner of the Minneapolis office. During the early 19805, Harrington was in charge of the auditing practice of Fox's Minneapolis office and was responsible for reviewing and approving SEC registration statements filed by clients of that office. Harrington and Arnott met with the top executives of FTC in early March 1980 and discussed the contractual details of the audit engagement. These details were documented in an engagement letter signed by Harrington and an FTC ofcer. At this meeting, the stafng of the 1980 audit and timing issues were also discussed. FTC's scal year ended on June 30. The company's president, William Rubin, insisted that the audited nancial statements be ready for the printer by early August. Rubin wanted the audit completed quickly to expedite the ling of a registration statement with the SEC that would allow his firm to sell additional securities to the public. Like most large accounting rms, Fox Alt Company used a risk assessment questionnaire during the planning phase of each audit engagement to document \"special\" audit risks. This questionnaire contained several inquiries regarding such high-risk items as related party transactions. When asked whether FTC had engaged in any related party transactions during fiscal 1980, FTC officials responded with a blunt no. However, shortly after the audit eldwork began, a Fox auditor discovered that most of FTC's revenues resulted from a contractual arrangement with International Air Systems GAS), a company owned and operated by William Rubin. Approximately twothirds of FTC's T980 consolin 2. K. Johnson, \"How High-ying Numbers Fooled the Experts,\" New York Times, 29 August 1982, sec. 3, 9. 3. Ibid. CASE 2.2 FLIGHT TRANSPORTATION CORPORATION 131 A. IAS shall provide FTC with large aircraft (727's and/or DC 8's) for charter to the Cayman EXHIBIT 1 .Islands and Mexico. Alleged Contractual B. All revenues earned by FTC will be recorded by IAS during the term of the agreement and Agreement between FTC provided to FTC at the conclusion of all flights along with the gross or net profit to be paid. and IAS Gross profit will be earned and paid if sufficient volume is attained. If volume is not high enough, only net profit will be paid to FTC. C. This agreement covers the period from July 1, 1979, through June 30, 1980. Source: Securities and Exchange Commission, Accounting and Auditing Enforce- ment Release No. 81, 5 December 1985. dated revenues stemmed from more than one hundred air charters that had been flown on LAS aircraft. To the staff auditor's surprise, he could find almost no documentary support for the $5.2 million of these air charter revenues. There were no sales invoices, no entries in the sales journal, and no related expenses recorded for these revenues. The support for the revenues consisted almost entirely of handwritten entries made in FTC's general journal. Because of the revenues' unusual nature and lack of documentation, the staff auditor prepared a list of the air charter revenues, which he gave to Arnott. Arnott immediately went to FTC's controller and asked for the documentation for the air charter revenues. The controller responded that the auditors would have to make arrangements with Rubin to obtain that documentation. Arnott then took the matter to Harrington, who contacted Rubin. After a brief conver- sation with Harrington, Rubin agreed to provide extensive documentation for the IAS-related revenues. This documentation was to include sales invoices, cash receipts and disbursements records, canceled checks, contracts, and computer runs listing the individual air charters. However, despite Rubin's interest in completing the audit as quickly as possible, he continually fabricated excuses to delay turning the documentation over to the auditors. Rubin's most frequent excuse for the delays was computer malfunctions. With only a few days remaining to meet the audit deadline, Rubin finally provided the Fox auditors with evidence to support the LAS-related air charter revenues. This evidence consisted of two one-page documents. The first docu- ment was the brief and ambiguous one-page contract between LAS and FTC that is shown in Exhibit 1. The second document was a one-page statement reporting the number of charter flights flown for FTC on IAS aircraft and the resulting revenues for FTC. When the auditors balked at accepting this documentation, Rubin took Harrington aside and informed him that the air charter revenues were not FTC revenues at all. Instead, these revenues had been generated strictly by LAS, which, again, was owned and operated by Rubin. Rubin explained to Harrington that "he was bored, had plenty of money, and wanted to use IAS to help FTC get into the charter business." Consequently, Rubin had donated the more than $5 million of IAS air charter revenues to FTC. Harrington accepted Rubin's explanation for the LAS revenues that were booked in FTC's accounting records. Rubin's explanation accounted for FTC's lack of documentation for those transactions. In a subsequent meeting, Har- rington explained to Arnott the true nature of the air charter revenues. He also informed Arnott that, in his opinion, no further evidence would be needed to support those revenues. Arnott disagreed with Harrington initially but then changed his mind after the two men discussed the matter. Arnott eventually132 SECTION TWO AUDITS OF HIGH-RISK ACCOUNTS AND INTERNAL CONTROL ISSUES indicated in the 1980 audit workpapers that the $5.2 million of air charter revenues were \"appropriately included\" in FTC's 1980 nancial statements. During a subsequent SEC investigation, Arnott testified that he never beiieved sufficient competent audit evidence had been obtained to support the suspicious air charter revenues. An SEC representative then questioned Arnott regarding his knowledge of a Fox \"disagreement procedure.\" This procedure or policy allowed subordinate members of an audit team to express their disagreement with a decision rendered on an audit engagement. This disagreement was to be documented in a written memorandum included in the audit workpapers. The disagreement memorandum effectively dissociated the individual from the decision. Arnott testified that he was aware of the disagreement procedure but did not take advantage of it for two reasons. First, he realized that as the audit engagement partner, Harrington would make the nal decision in the matter. Second, he was worried that his job with Fox (in Company might be jeopardized if he followed that procedure. , I _ The SEC also quizzed Harrington regarding his discussion of the air charter revenues with Arnott. Harrington reported that he could not recall Arnott disagreeing with his decision that sufficient evidence had been coilected to support the air charter revenues. WM Fox's 1981 AUDIT or FTC In July 1980, shortly after the beginning of FTC's 1981 scal year, the company established a subsidiary located in the Cayman Islands. The reported purpose of this subsidiary was to operate an air charter business. During fiscai 198i, FTC booked more than $13 million of nonexistent revenues through FTC Cayman Ltd., its Cayman Islands subsidiary. These revenues represented more than onehalf of FTC's consolidated revenues for scal 1981. FTC's consolidated balance sheet as of June 39, 1981, the nal day of the company's 1981 fiscal year, reported more than $6 million of receivables, land, and other assets related to FTC Cayman. Again, these assets did not exist or were not owned by FTC or its subsidiary. In June 1981, Harrington and Arnott met with Rubin and other FTC officers in a planning conference for the 1981 audit. During this conference, Harrington and Arnott were informed that most of FTC's revenues had been generated by the company's new Cayman Islands subsidiary They were also told by FTC's management that the documentation for these revenues was in the Cayman Islands but that this documentation would be brought to Minnesota during the audit, Again, Rubin wanted the audit completed as quickly as possible. The parties agreed that the eldwork would be completed by July 31 and that the audit report would be signed by August 12. When the 1981 audit began in early July, the oniy documentation made available to the Fox auditors for FTC Cayman was a trial balance and a computerized general ledger and general journal. On August 6, one week after the fieldwork was supposed to be finished and less than one week before the audit report was to be signed, the auditors were also given the fiscal 1981 bank statements for FTC Cayman. Except for a few other minor items, these bank statements Were the only externally prepared documents provided to the Fox auditors to support the revenues of FTC Cayman. These bank statements were CASE 2.2 FLIGHT TRANSPORTATION CORPORATION not obtained directly from the subsidiary's bank but instead were given to the Fox auditors by an FTC employee. . Rubin informed Harrington and Arnott that they could verify the subsidiary's revenues by reviewing the deposits reported in its bank statements during fiscal 1981. A member of the audit engagement team did just that. A reconciliation of the revenues reported by FTC Cayman and the deposits reected in the subsidiary's 1981 bank statements resulted in a small, unlocated difference between the two amounts. Given this small difference, the auditors concluded The Fox auditors attempted to conrm $3 million of cash that FTC Cayman reportedly had on- deposit in the Cayman Islands as of June 30, 1981. Throughout the audit, FTC executives tried to persuade the auditors that obtaining a confirmation for that cash balance would be difcult, given the bank secrecy laws in the Cayman Islands. The auditors mailed a conrmation to the subsidiary's Cayman islands bank using an address supplied by FTC. That conrmation was never returned. Eventually, Harrington agreed to accept a confirmation of the year-end cash balance that an employee of the subsidiary had allegedly obtained from the Cayman Islands bank. This conrmation was forged by the FTC Harrington arranged to speak with an official Of the Cayman Islands bank to obtain an oral conrmation of the year-end cash balance. Rubin invited Har- rington to come to his ofce to obtain this conrmation over the telephone. After Rubin placed a callallegedly to the bankand had a brief conversation, he handed the telephone to Harrington. The individual at the other end of the line then conrmed that FTC's subsidiary had the reported amount of cash on deposit as of June 30, 1981. The Fox auditors also attempted to confirm a $2 million receivable of FTC Cayman at the end of fiscal 1981. A conrmation for this amount was mailed to a tour group operator who allegedly organized most of the subsidiary's air charter ights. A confirmation was returned indicating that the receivable did exist in the correct amount. However, the confirmation returned was not the conrmation that had been mailed by the Fox auditors. The returned conrma- M SANCTIONS IMPOSED ON HARRINGTON AND ARNOTT In late 1985, following the SEC investigation of the 1980 and 1981 FTC audits, the federal agency sanctioned both John Harrington and Gregory Arnott. Harrington was permanently banned from practicing before the SEC. However, the SEC's disciplinary order allowed Harrington to apply for a repeal of this ban after five years. Arnott was suspended from practicing before the SEC for one year. In commenting on Arnott's role in the FTC audits, the SEC stressed the need for members of an audit engagement team to maintain an independent state of mind even if that means jeopardizing their jobs. Arnott engaged in unprofessional conduct by abdicating his role as an independent professional to the audit partner. He properly recognized that the audit evidence was 133 134 SECTION TWO AUDITS OF HIGH-RISK ACCGUNTS AND INTERNAL CONTROL ISSUES inadequate and took the appropriate step of informing the partner. HOWever, he faiied to act on his conviction and caused the workpapers to evidence incorrectly his agreement. \" EPILOGUE Foliowing a series of highly publicized \"problem\" audits by Fox 82 Company, including the 1980 and 1981 FTC audits, the SEC prohibited the firm from accepting new SEC clients for a six-month period beginning in 1983. During this time, the SEC formed an independent committee to review Fox & Company's auditing practice. The purpose of this review was to recommend changes to improve Fox 82 Company's quality control procedures. In 1985, Fox (it Company merged with Alexander Grant :3: Company. Shortly thereafter, Alexander Grant was renamed Grant Thornton. _ In 1982, the SEC sanctioned William Rubin for his role in the fraudulent misrepresentation of FIGS financial statements. The SEC permanently enjoined Rubin from further violations of the federal securities laws. Eventually, the SEC, ' other federal agencies, and private plaintiffs recovered more than $45 million from FTC and its executives including almost $2 million from Rubin. These funds ' were distributed by FTC's court-appointed receiver to the company's bondhold- ers, other creditors, and stockholders. m QUESTIONS 1. Assume the role of Gregory Arnott during the 1980 FTC audit and draft a memo to be included in the FTC workpapers. In this memo, express your disagreement with John Harrington's decision that sufficient competent evidence had been collected to support the suspicious air charter revenues. 2. Identify measures accounting rms could adopt to diminish the likelihood that auditors will capitulate to their superiors when technical disagreements arise during an audit. 3. Assume that you were the staff auditor who discovered the bogus air charter revenues during the 1980 audit. What responsibilities did you have with respect to these revenues? For example, did you have a responsibility to write a memo dissociating yourself from Harrington's decision regarding these revenues? Make any assumptions you believe are necessary to respond to this question. 4. Besides the related party transactions, what other \"special\" audit risks existed in the FTC audits? How should these factors have affected the planning decisions for these audits? 5. Identify specific measures that audit rms can take to ensure that client- irnposed pressure does not adversely affect the quality of an independent audit. 6. In your opinion, what additional audit procedures should the Fox auditors have applied to the 1981 FTC Cayman revenues? 7. Briey identify the deficiencies in the conrmation procedures used by the Fox auditors. How did these deficiencies affect the competence and sufficiency of the audit evidence yielded by these procedures

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!