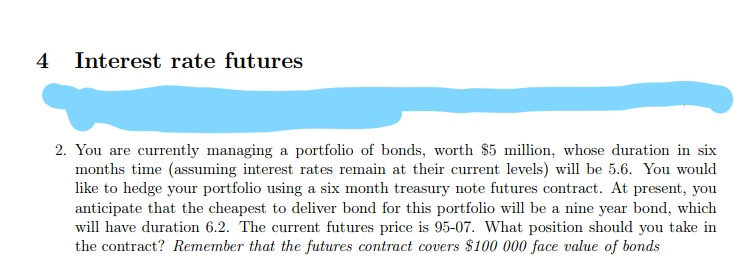

Question: (Please only answer the question no.2 as in the first image, The current futures price, 95.07) 4 Interest rate futures 2. You are currently managing

(Please only answer the question no.2 as in the first image, The current futures price, 95.07)

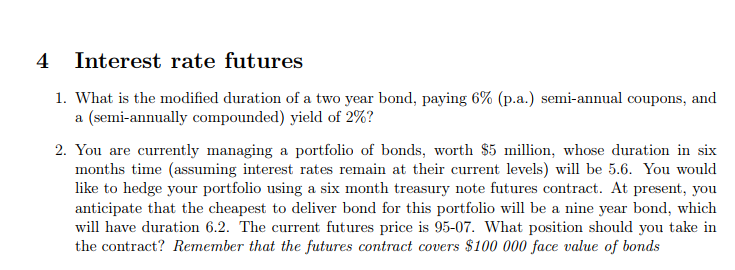

4 Interest rate futures 2. You are currently managing a portfolio of bonds, worth $5 million, whose duration in six months time (assuming interest rates remain at their current levels) wil be 5.6. You would like to hedge your portfolio using a six month treasury note futures contract. At present, you anticipate that the cheapest to deliver bond for this i will have duration 6.2. The current futures price is 95-07. What position should you take in the contract? Remember that the futures contract covers S100 000 face value of bonds

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts