Question: (Please post step-by-step solution on how to solve with a calculator, thank you!) Assume that you manage a risky portfolio with an expected rate of

(Please post step-by-step solution on how to solve with a calculator, thank you!)

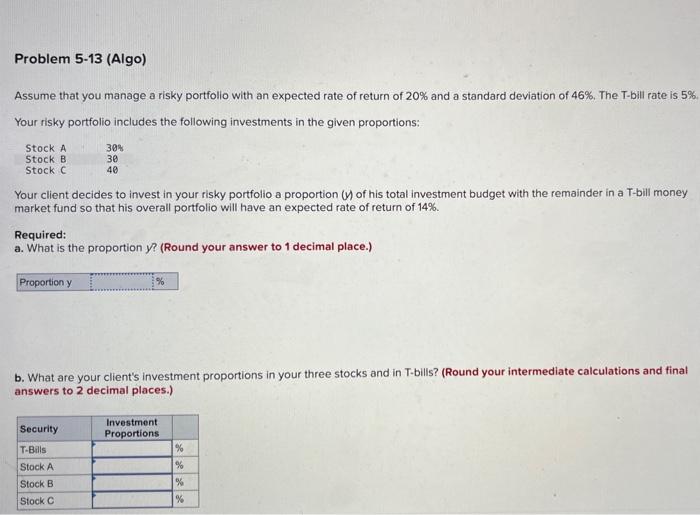

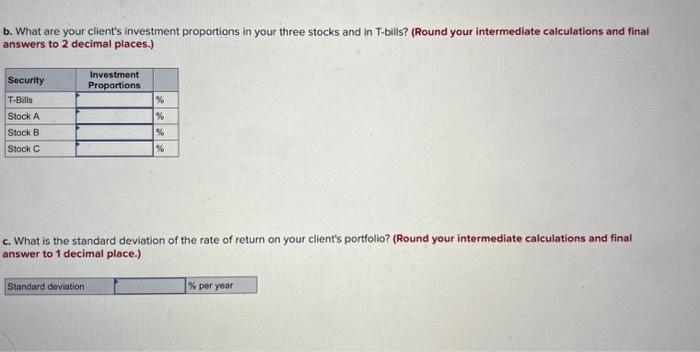

Assume that you manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 46%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: Your client decides to invest in your risky portfolio a proportion (y) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected rate of return of 14%. Required: a. What is the proportion y ? (Round your answer to 1 decimal place.) b. What are your client's investment proportions in your three stocks and in T-bills? (Round your intermediate calculations and final answers to 2 decimal places.) b. What are your client's investment proportions in your three stocks and in T-bills? (Round your intermediate calculations and final answers to 2 decimal places.) c. What is the standard deviation of the rate of return on your client's portfolio? (Round your intermediate calculations and final answer to 1 decimal place.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts