Question: Please provide solution 2. (46 POINTS) A pension fund manager is considering investing in 2 mutual funds: a stock fund (S), a long-term government and

Please provide solution

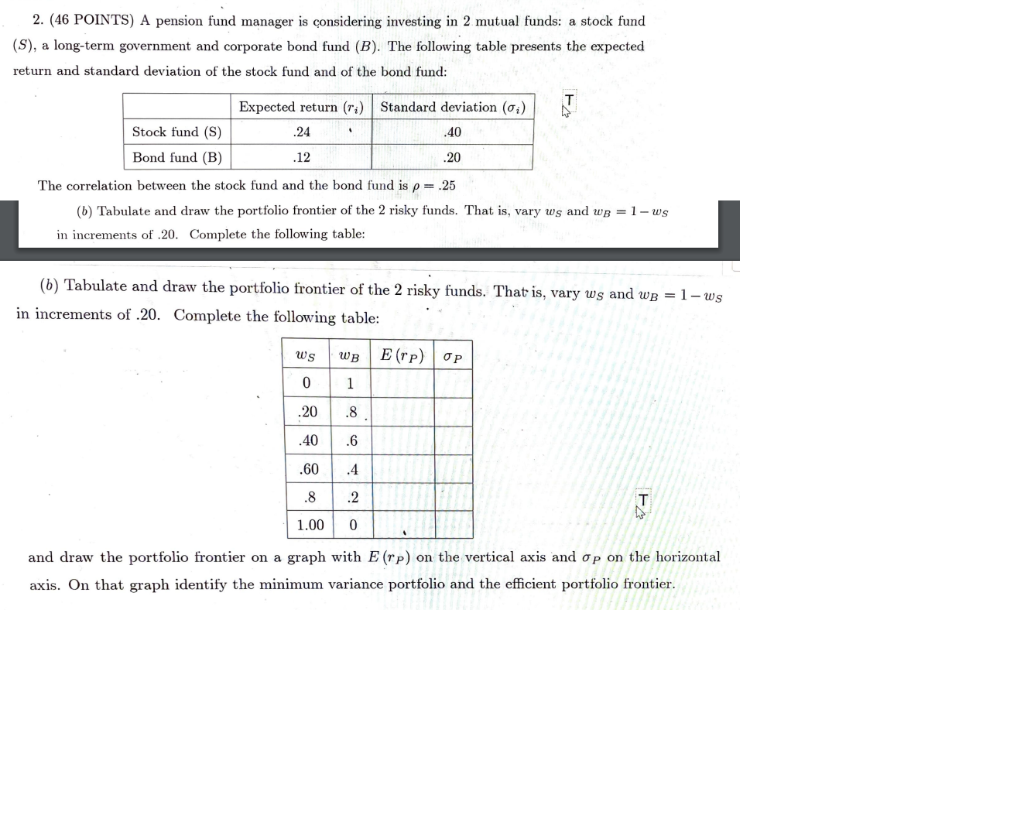

2. (46 POINTS) A pension fund manager is considering investing in 2 mutual funds: a stock fund (S), a long-term government and corporate bond fund (B). The following table presents the expected return and standard deviation of the stock fund and of the bond fund: Expected return (r) Standard deviation (0) Stock fund (S) .24 4 .40 Bond fund (B) .12 .20 The correlation between the stock fund and the bond fund is p= .25 (6) Tabulate and draw the portfolio frontier of the 2 risky funds. That is, vary ws and wg = 1 -ws in increments of.20. Complete the following table: (6) Tabulate and draw the portfolio frontier of the 2 risky funds. That is, vary ws and we = 1 -ws in increments of 20. Complete the following table: ws WB E (rp) OP 0 1 .20 .8 .40 .6 .60 .4 .8 .2 1.00 0 and draw the portfolio frontier on a graph with E (rp) on the vertical axis and Op on the horizontal axis. On that graph identify the minimum variance portfolio and the efficient portfolio frontier

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts