Question: Please provide step by step explanations :) Question 3: Beta (4 marks) Assume that both Spark and Vodafone plot on the Security Market Line (SML).

Please provide step by step explanations :)

Please provide step by step explanations :)

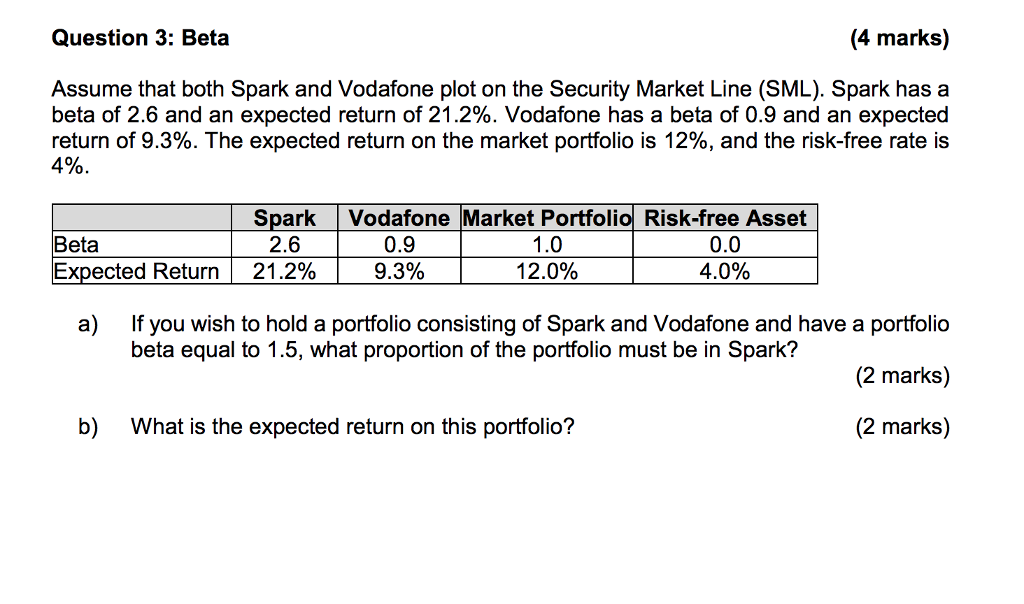

Question 3: Beta (4 marks) Assume that both Spark and Vodafone plot on the Security Market Line (SML). Spark has a beta of 2.6 and an expected return of 21.2%. Vodafone has a beta of 0.9 and an expected return of 9.3%. The expected return on the market portfolio is 12%, and the risk-free rate is 4%. SparkVodafone Market Portfolio Risk-free Asset 0.9 9.3% 1.0 120% 0.0 4.0% 2.6 Expected Return | 21.2% | a) If you wish to hold a portfolio consisting of Spark and Vodafone and have a portfolio beta equal to 1.5, what proportion of the portfolio must be in Spark? (2 marks) b) What is the expected return on this portfolio? (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts