Question: Please provide the complete solution! Thank you! 1.9. A decision maker has utility function u(w) = k log w. The decision maker has wealth w,

Please provide the complete solution! Thank you!

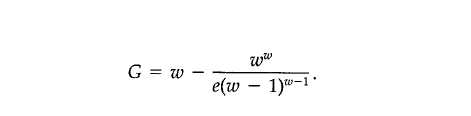

1.9. A decision maker has utility function u(w) = k log w. The decision maker has wealth w, w > 1, and faces a random loss X, which has a uniform distribution on the interval (0, 1). Use (1.3.1) to show that the maximum insurance pre- mium that the decision maker will pay for complete insurance is ww G = W- e(w 1)-1' 1.9. A decision maker has utility function u(w) = k log w. The decision maker has wealth w, w > 1, and faces a random loss X, which has a uniform distribution on the interval (0, 1). Use (1.3.1) to show that the maximum insurance pre- mium that the decision maker will pay for complete insurance is ww G = W- e(w 1)-1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts