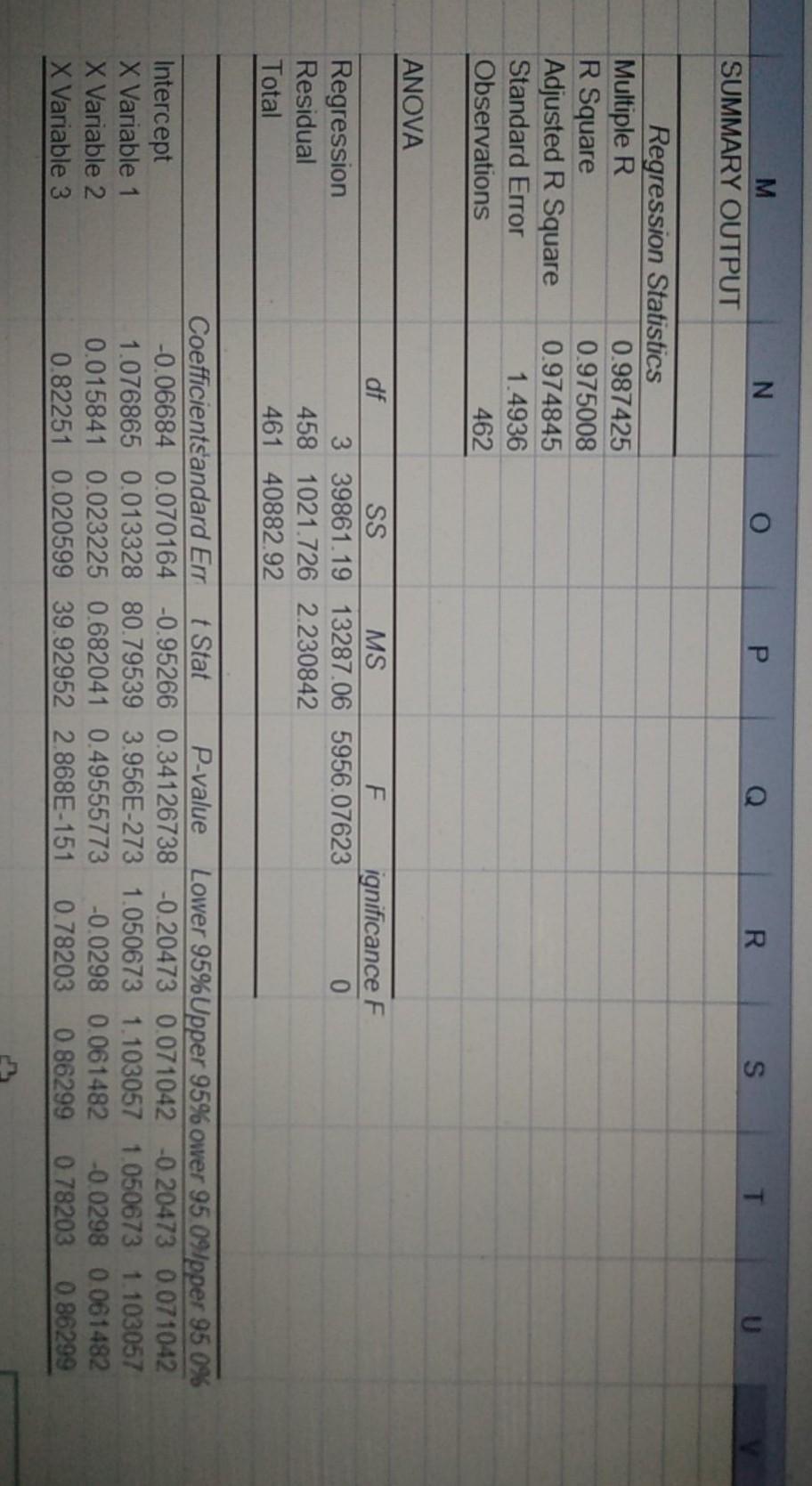

Question: Please refer to data spreadsheet, tab Fama-French 3F. Please run Fama-French three factor regression and select the CORRECT answer: Fama-French three factor model explains variation

Please refer to data spreadsheet, tab Fama-French 3F. Please run Fama-French three factor regression and select the CORRECT answer:

Fama-French three factor model explains variation in returns of the target portfolio better than the Capital asset pricing model

Coefficient of determination equals 91%

Market beta is statistically insignificant in the model

Intercept coefficient, or alpha, equals 2.47% a month

N M SUMMARY OUTPUT P R S T Regression Statistics Multiple R 0.987425 R Square 0.975008 Adjusted R Square 0.974845 Standard Error 1.4936 Observations 462 ANOVA Regression Residual Total df SS MS F ignificance F 3 39861.19 13287.06 5956.07623 0 458 1021.726 2.230842 461 40882.92 Intercept X Variable 1 X Variable 2 X Variable 3 Coefficients'andard Errt Stat P-value Lower 95%Upper 95% ower 95 09/pper 95 0% -0.06684 0.070164 -0.95266 0.34126738 -0.20473 0.071042 -0.20473 0.071042 1.076865 0.013328 80.79539 3.956E-273 1.050673 1.103057 1.050673 1.103057 0.015841 0.023225 0.682041 0.49555773 -0.0298 0.061482 -0.0298 0.061482 0.82251 0.020599 39.92952 2.868E-151 0.78203 0.86299 0.78203 0.86299

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts