Question: Please see screenshots attached. If additional info is needed please let me know You have been provided the fdlowing data about the securities of three

Please see screenshots attached. If additional info is needed please let me know

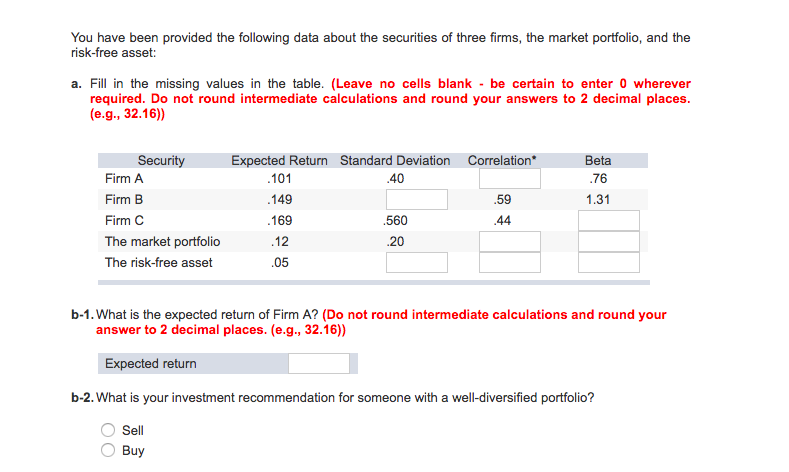

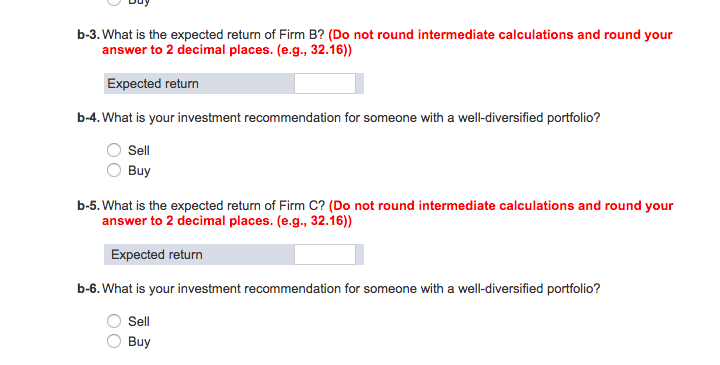

You have been provided the fdlowing data about the securities of three rms, the market portfolio. and the risk-free asset: a. Fill in the missing values in the table. [Leave no cells blank - be certain to enter 0 wherever required. Do not round intermediate calculations and round your answers to 2 decimal places. [e.g., 32.161} Security Expected Rolum Stande Deviation Gonelation' Bola Flrrn A .1111 .411 |:| .ra rm a .149 |:| .59 1.31 44 Firm 0 .169 .550 . The market portfolio .12 .20 The riskfree asset .05 |:| b-1.What is the expected return of Firm A? [Do not round intermediate calculations and round your answer Ito 2 decimal places. {e.g., 32.16)} 5mm D h-2.'What is your investment recommendation for someone with a well-diversied portfolio? ,' Hur- h-3.What is the expected return of Firm B? [Do not rcu nd intermediate calculations and reund yrcur answer to 2 decimal places. {e.g., 32.151} Emum E h-deWhat is your investment recommendation for someone with a well-diversied portfolio? h-5.What is the expected return of Firm 0'? {Do not run nd intermediate calculations and round your answer to 2 decimal places. {e.g., 32.15)} mm D h-E.What is your investment recommendation for someone with a welldiversied portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts