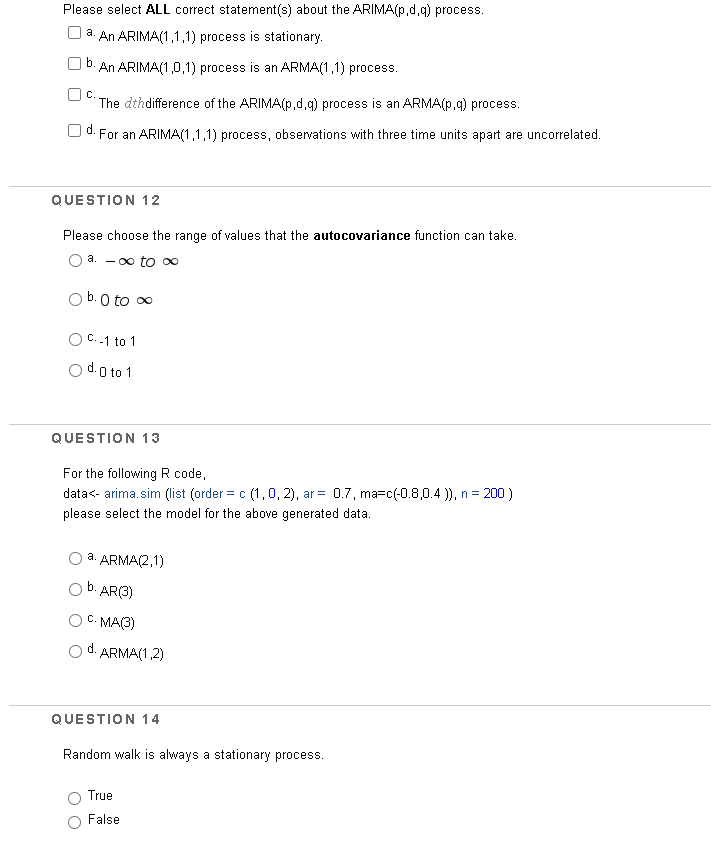

Question: Please select ALL correct statement(s) about the ARIMA(p, d, q) process. a. An ARIMA(1,1,1) process is stationary. O b. An ARIMA(1 0,1) process is an

Please select ALL correct statement(s) about the ARIMA(p, d, q) process. a. An ARIMA(1,1,1) process is stationary. O b. An ARIMA(1 0,1) process is an ARMA(1,1) process. "The dthdifference of the ARIMA(p,d,q) process is an ARMA(p,q) process. O d. For an ARIMA(1,1,1) process, observations with three time units apart are uncorrelated. QUESTION 12 Please choose the range of values that the autocovariance function can take. a. - 00 to Do O b. 0 to oo O C.-1 to 1 O do to 1 QUESTION 13 For the following R code, data

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock