Question: Please send me answer of this question within 10 min i will give you like sure.send me typed answer only C Adapted from Besanko and

Please send me answer of this question within 10 min i will give you like sure.send me typed answer only

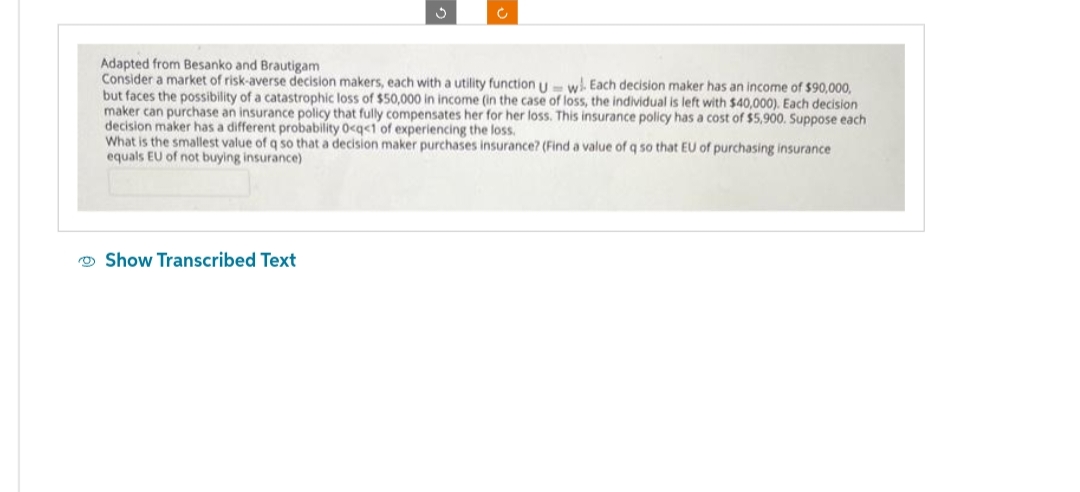

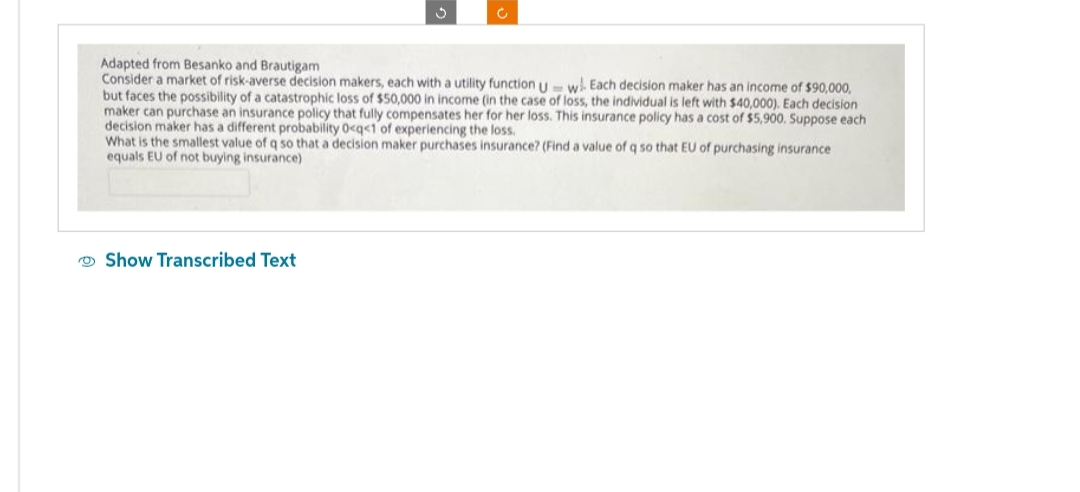

C Adapted from Besanko and Brautigam Consider a market of risk-averse decision makers, each with a utility function U = wJ. Each decision maker has an income of $90,000, but faces the possibility of a catastrophic loss of $50,000 in income (in the case of loss, the individual is left with $40,000). Each decision maker can purchase an insurance policy that fully compensates her for her loss. This insurance policy has a cost of $5,900. Suppose each decision maker has a different probability 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock