Question: Please show all excel work on excel sheet Question 4: (4 points) Given the settlement date of December 9. 2020 and the yield to maturity

Please show all excel work on excel sheet

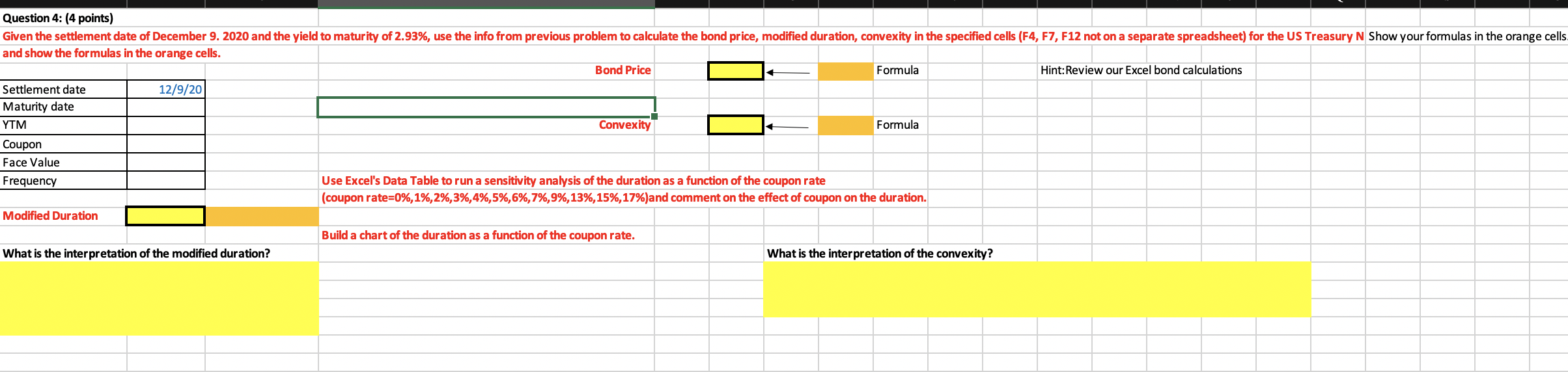

Question 4: (4 points) Given the settlement date of December 9. 2020 and the yield to maturity of 2.93%, use the info from previous problem to calculate the bond price, modified duration, convexity in the specified cells (F4, F7, F12 not on a separate spreadsheet) for the US Treasury N Show your formulas in the orange cells and show the formulas in the orange cells. Bond Price Formula Hint: Review our Excel bond calculations Settlement date 12/9/20 Maturity date TM Convexity Formula Coupon Face Value Frequency Use Excel's Data Table to run a sensitivity analysis of the duration as a function of the coupon rate (coupon rate=0%,1%,2%,3%,4%,5%,6%, 7%,9%,13%,15%,17%)and comment on the effect of coupon on the duration. Modified Duration Build a chart of the duration as a function of the coupon rate. What is the interpretation of the modified duration? What is the interpretation of the convexity

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts