Question: please show all the steps on the answer for the question Navidale, a listed engineering company, manufactures large scale plant and machinery for industrial companies

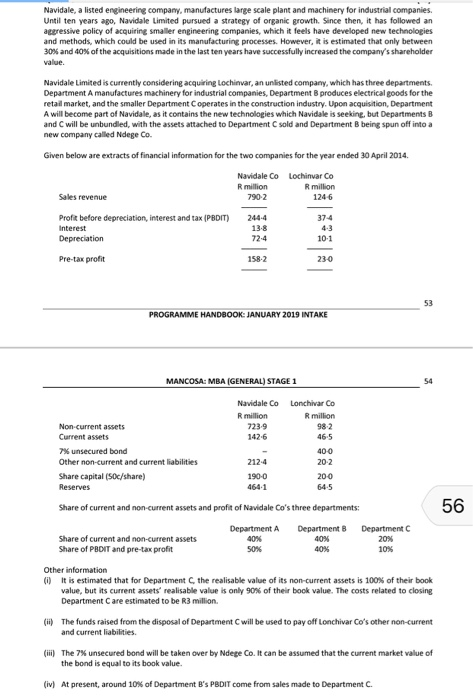

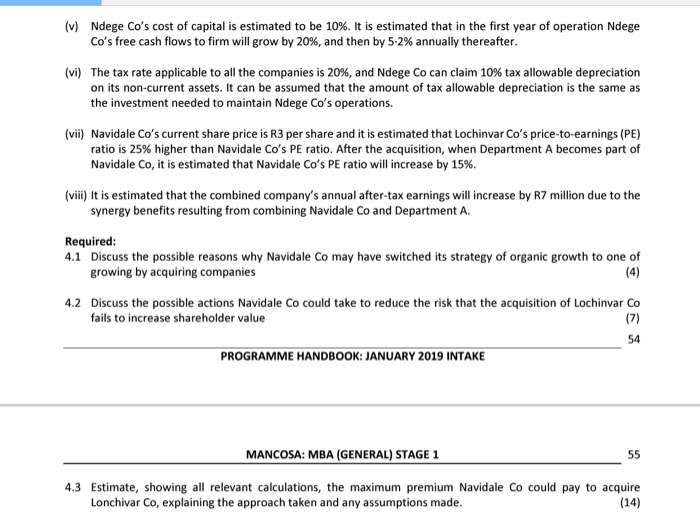

Navidale, a listed engineering company, manufactures large scale plant and machinery for industrial companies Until ten years ago, Navidale Limited pursued a strategy of organic growth. Since then, it has followed an agressive policy of acquiring smaller engineering companies, which it feels have developed new technologies and methods, which could be used in its manufacturing processes. However, is estimated that only between 30 and of the acquisitions made in the last ten years have successfully increased the company's shareholder Navidale Limited is currently considering acquiring Lochinvar, an unlisted company, which has three departments Department A manufactures machinery for industrial companies, Department produces electrical goods for the retail market, and the smaller Department operates in the construction industry. Upon acquisition Department A will become part of Navidale, as it contains the new technologies which Navidale is seeking, but Departments and will be unbundled, with the assets attached to Department Cold and Department being sun off into a new company called Ndege Co. Given below are extracts of financial information for the two companies for the year ended 30 April 2014 Navidale Colochinvar Co Rmillion Rmillion 1246 Sales revenue 2902 2444 Profit before depreciation, interest and tax (PBDIT) Interest Depreciation 72-4 Pre-tax profit PROGRAMME HANDBOOK: JANUARY 2019 INTAKE MANCOSA MBA (GENERAL) STAGE 1 Navidale Co Rmillion 723.9 Lonchivar Co Rmillion 142-6 465 400 Non-current assets Current assets Kunsecured bond Other non-current and current liabilities Share capital (S0c/share) Reserves 212-4 1900 202 200 645 Share of current and non-current assets and profit of Navidale Co's three departments: 56 Department Share of current and non-current assets Share of PBDIT and pre-tax profit Department A 40% 50% Department 20% 10% 40% Other information It is estimated that for Department the realisable value of its non-current assets is 100% of their book value, but its current assetsrealisable value is only Son of their book value. The costs related to closing Department Care estimated to be R3 million The funds raised from the disposal of Department will be used to pay off Lonchiar Co's other non-current and current abilities (ii) The 7% unsecured bond will be taken over by Ndege Co. It can be assumed that the current market value of the bond is equal to its book value. (iv) At present, around 10% of Department B's PSDIT come from sales made to Department C. (v) Ndege Co's cost of capital is estimated to be 10%. It is estimated that in the first year of operation Ndege Co's free cash flows to firm will grow by 20%, and then by 5-2% annually thereafter. (vi) The tax rate applicable to all the companies is 20%, and Ndege Co can claim 10% tax allowable depreciation on its non-current assets. It can be assumed that the amount of tax allowable depreciation is the same as the investment needed to maintain Ndege Co's operations. (vii) Navidale Co's current share price is R3 per share and it is estimated that Lochinvar Co's price-to-earnings (PE) ratio is 25% higher than Navidale Co's PE ratio. After the acquisition, when Department A becomes part of Navidale Co, it is estimated that Navidale Co's PE ratio will increase by 15%. (viii) It is estimated that the combined company's annual after-tax earnings will increase by R7 million due to the synergy benefits resulting from combining Navidale Co and Department A. Required: 4.1 Discuss the possible reasons why Navidale Co may have switched its strategy of organic growth to one of growing by acquiring companies (4) 4.2 Discuss the possible actions Navidale Co could take to reduce the risk that the acquisition of Lochinvar Co fails to increase shareholder value PROGRAMME HANDBOOK: JANUARY 2019 INTAKE MANCOSA: MBA (GENERAL) STAGE 1 4.3 Estimate, showing all relevant calculations, the maximum premium Navidale Co could pay to acquire Lonchivar Co, explaining the approach taken and any assumptions made. (14) Navidale, a listed engineering company, manufactures large scale plant and machinery for industrial companies Until ten years ago, Navidale Limited pursued a strategy of organic growth. Since then, it has followed an agressive policy of acquiring smaller engineering companies, which it feels have developed new technologies and methods, which could be used in its manufacturing processes. However, is estimated that only between 30 and of the acquisitions made in the last ten years have successfully increased the company's shareholder Navidale Limited is currently considering acquiring Lochinvar, an unlisted company, which has three departments Department A manufactures machinery for industrial companies, Department produces electrical goods for the retail market, and the smaller Department operates in the construction industry. Upon acquisition Department A will become part of Navidale, as it contains the new technologies which Navidale is seeking, but Departments and will be unbundled, with the assets attached to Department Cold and Department being sun off into a new company called Ndege Co. Given below are extracts of financial information for the two companies for the year ended 30 April 2014 Navidale Colochinvar Co Rmillion Rmillion 1246 Sales revenue 2902 2444 Profit before depreciation, interest and tax (PBDIT) Interest Depreciation 72-4 Pre-tax profit PROGRAMME HANDBOOK: JANUARY 2019 INTAKE MANCOSA MBA (GENERAL) STAGE 1 Navidale Co Rmillion 723.9 Lonchivar Co Rmillion 142-6 465 400 Non-current assets Current assets Kunsecured bond Other non-current and current liabilities Share capital (S0c/share) Reserves 212-4 1900 202 200 645 Share of current and non-current assets and profit of Navidale Co's three departments: 56 Department Share of current and non-current assets Share of PBDIT and pre-tax profit Department A 40% 50% Department 20% 10% 40% Other information It is estimated that for Department the realisable value of its non-current assets is 100% of their book value, but its current assetsrealisable value is only Son of their book value. The costs related to closing Department Care estimated to be R3 million The funds raised from the disposal of Department will be used to pay off Lonchiar Co's other non-current and current abilities (ii) The 7% unsecured bond will be taken over by Ndege Co. It can be assumed that the current market value of the bond is equal to its book value. (iv) At present, around 10% of Department B's PSDIT come from sales made to Department C. (v) Ndege Co's cost of capital is estimated to be 10%. It is estimated that in the first year of operation Ndege Co's free cash flows to firm will grow by 20%, and then by 5-2% annually thereafter. (vi) The tax rate applicable to all the companies is 20%, and Ndege Co can claim 10% tax allowable depreciation on its non-current assets. It can be assumed that the amount of tax allowable depreciation is the same as the investment needed to maintain Ndege Co's operations. (vii) Navidale Co's current share price is R3 per share and it is estimated that Lochinvar Co's price-to-earnings (PE) ratio is 25% higher than Navidale Co's PE ratio. After the acquisition, when Department A becomes part of Navidale Co, it is estimated that Navidale Co's PE ratio will increase by 15%. (viii) It is estimated that the combined company's annual after-tax earnings will increase by R7 million due to the synergy benefits resulting from combining Navidale Co and Department A. Required: 4.1 Discuss the possible reasons why Navidale Co may have switched its strategy of organic growth to one of growing by acquiring companies (4) 4.2 Discuss the possible actions Navidale Co could take to reduce the risk that the acquisition of Lochinvar Co fails to increase shareholder value PROGRAMME HANDBOOK: JANUARY 2019 INTAKE MANCOSA: MBA (GENERAL) STAGE 1 4.3 Estimate, showing all relevant calculations, the maximum premium Navidale Co could pay to acquire Lonchivar Co, explaining the approach taken and any assumptions made. (14)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts