Question: please show all the work clearly!! and answer every part please. 19. You are in charge of the bond trading and forward loan department of

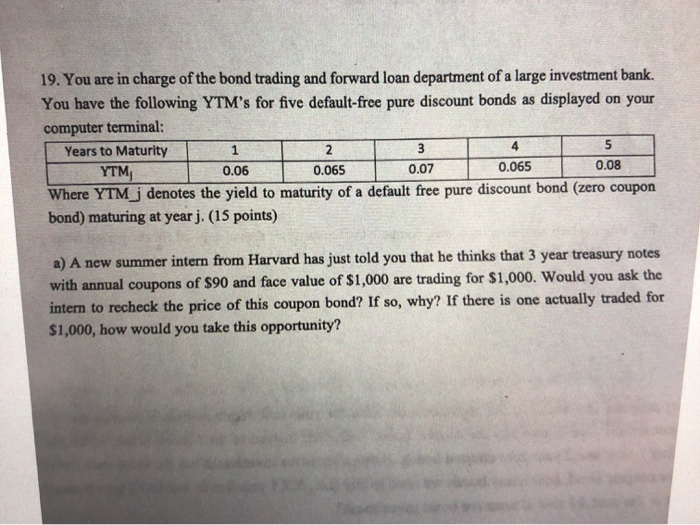

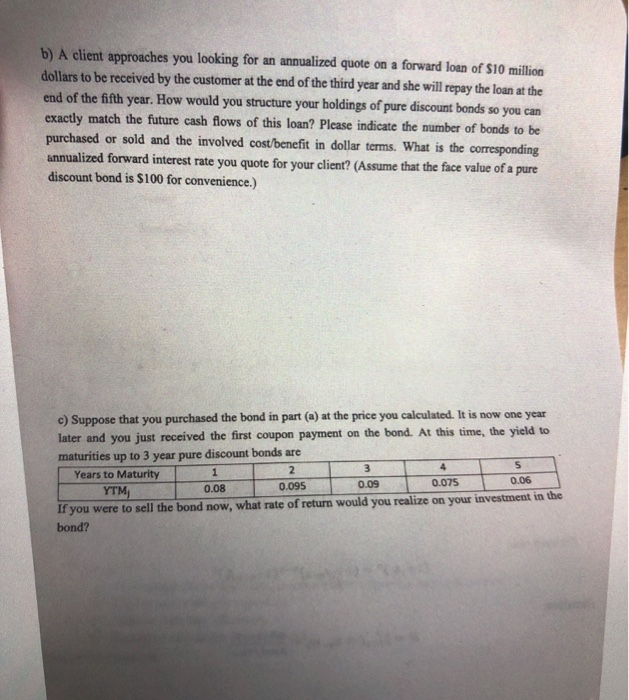

19. You are in charge of the bond trading and forward loan department of a large investment bank. You have the following YTM's for five default-free pure discount bonds as displayed on your computer terminal: Years to Maturity 2 3 YTM 0.06 0.065 0.07 0.065 0.08 Where YTM_j denotes the yield to maturity of a default free pure discount bond (zero coupon bond) maturing at year j. (15 points) a) A new summer intern from Harvard has just told you that he thinks that 3 year treasury notes with annual coupons of $90 and face value of $1,000 are trading for $1,000. Would you ask the intern to recheck the price of this coupon bond? If so, why? If there is one actually traded for $1,000, how would you take this opportunity? b) A client approaches you looking for an annualized quote on a forward loan of S10 million dollars to be received by the customer at the end of the third year and she will repay the loan at the end of the fifth year. How would you structure your holdings of pure discount bonds so you can exactly match the future cash flows of this loan? Please indicate the number of bonds to be purchased or sold and the involved cost/benefit in dollar terms. What is the corresponding annualized forward interest rate you quote for your client? (Assume that the face value of a pure discount bond is $100 for convenience.) c) Suppose that you purchased the bond in part @) at the price you calculated. It is now one year Later and you just received the first coupon payment on the bond. At this time, the yield to maturities up to 3 year pure discount bonds are Years to Maturity 0.095 0.08 YTM, 0.06 0.09 0.075 If you were to sell the bond now, what rate of return would you realize on your investment in the bond

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts