Question: Please show all work in excel spreadsheet! In an earlier worksheet, we discussed the difference between yield to maturity and yield to call. There is

Please show all work in excel spreadsheet!

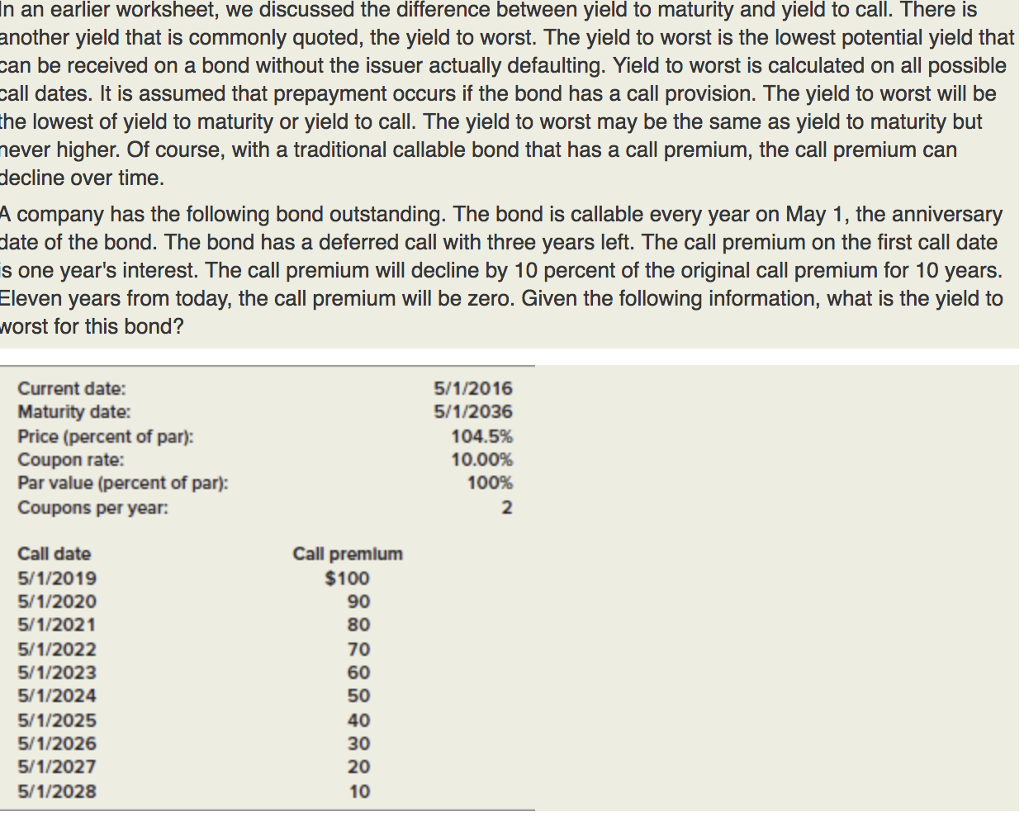

In an earlier worksheet, we discussed the difference between yield to maturity and yield to call. There is another yield that is commonly quoted, the yield to worst. The yield to worst is the lowest potential yield that an be received on a bond without the issuer actually defaulting. Yield to worst is calculated on all possible all dates. It is assumed that prepayment occurs if the bond has a call provision. The yield to worst will be the lowest of yield to maturity or yield to call. The yield to worst may be the same as yield to maturity but ever higher. Of course, with a traditional callable bond that has a call premium, the call premium can decline over time. A company has the following bond outstanding. The bond is callable every year on May 1, the anniversary date of the bond. The bond has a deferred call with three years left. The call premium on the first call date s one year's interest. The call premium will decline by 10 percent of the original call premium for 10 years Eleven years from today, the call premium will be zero. Given the following information, what is the yield to worst for this bond? Current date: Maturity date: Price (percent of par): Coupon rate: Par value (percent of par): Coupons per year: 5/1/2016 5/1/2036 104.5% 10.00% 100% 2 Call date 5/1/2019 5/1/2020 5/1/2021 5/1/2022 5/1/2023 5/1/2024 5/1/2025 5/1/2026 5/1/2027 5/1/2028 Call premlum $100 90 80 70 60 50 40 30 20 10

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts