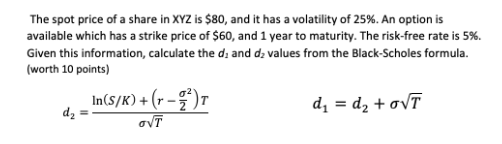

Question: Please show all work - no excel sheets if possible The spot price of a share in XYZ is $80, and it has a volatility

Please show all work - no excel sheets if possible

The spot price of a share in XYZ is $80, and it has a volatility of 25%. An option is available which has a strike price of $60, and 1 year to maturity. The risk-free rate is 5%. Given this information, calculate the d, and dz values from the Black-Scholes formula. (worth 10 points) In(s/K) + (- - ) dz dy = d2 +ovt NT

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock