Question: please show formulas and please use excel. need to understand it and work it out not just the answers! thank you! Annual Standard 4. Portfolio

please show formulas and please use excel. need to understand it and work it out not just the answers! thank you!

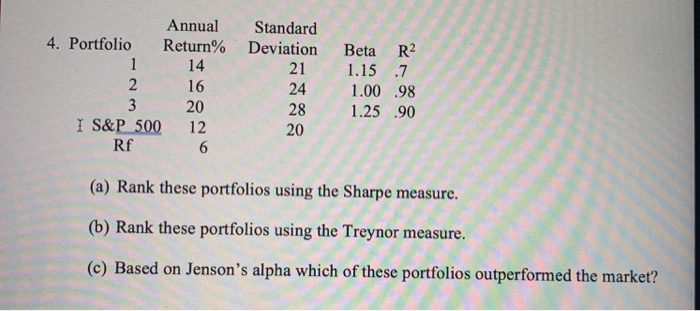

Annual Standard 4. Portfolio Return% Deviation 1 14 21 2 16 24 3 20 28 I S&P 500 12 20 RE 6 Beta R2 1.15 .7 1.00 98 1.25 90 (a) Rank these portfolios using the Sharpe measure. (b) Rank these portfolios using the Treynor measure. (c) Based on Jenson's alpha which of these portfolios outperformed the market

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock