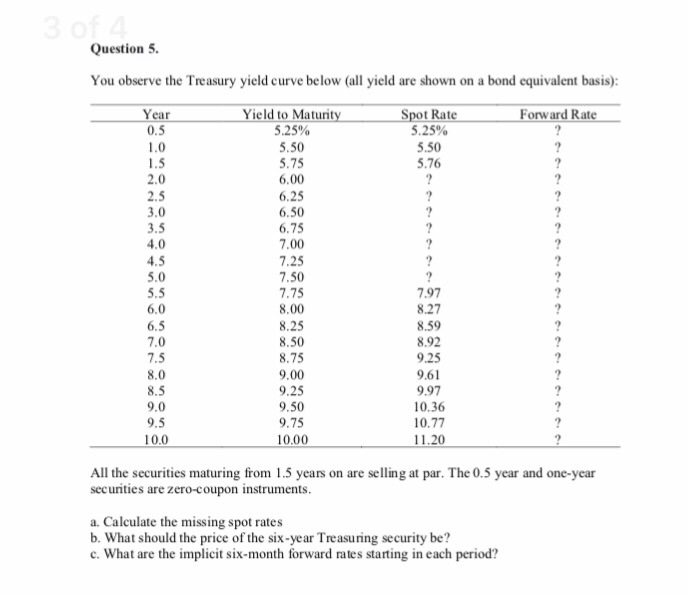

Question: Please show formulas Question 5 You observe the Treasury yield curve below (all yield are shown on a bond equivalent basis) Year 0.5 Yield to

Question 5 You observe the Treasury yield curve below (all yield are shown on a bond equivalent basis) Year 0.5 Yield to Maturity Spot Rate Forward Rate 5.25% 5.50 5.75 6.00 .25 6.50 5.25% 5.50 5.76 2.5 3.5 4.0 5.5 6.0 6.5 7.0 7.5 8.0 8.5 9.0 9.5 0.0 7.00 7.25 7.50 7.75 8.00 8.25 8.50 8.75 9.00 9.25 9.50 9.75 7.97 8.27 8.59 8.92 9.25 9.61 9.97 10.36 10.77 11.20 10.00 All the securities maturing from 1.5 years on are selling at par. The 0.5 year and one-year secunties are zero-coupon instruments a. Calculate the missing spot rates b. What should the price of the six-year Treasuring security be? c. What are the implicit six-month forward rates starting in each period

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts