Question: Please show full solution please and thanks. For the next two questions (31-32), ASSUME that the one year returns for RIM are still (20%, -40%,

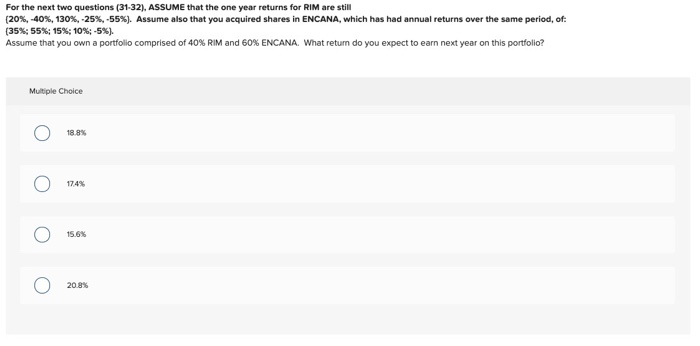

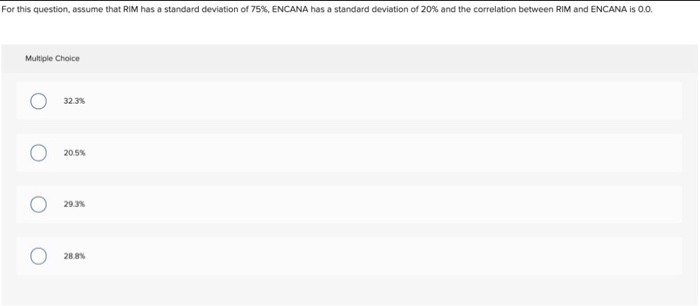

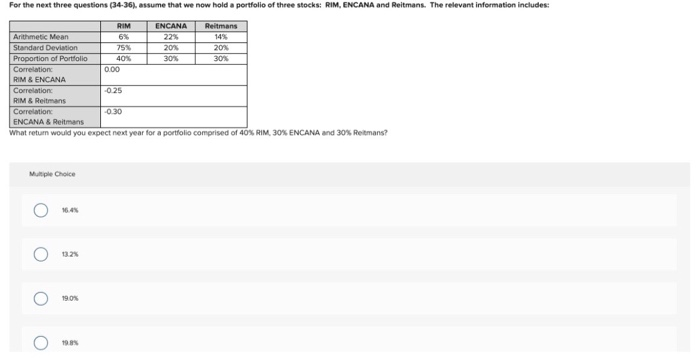

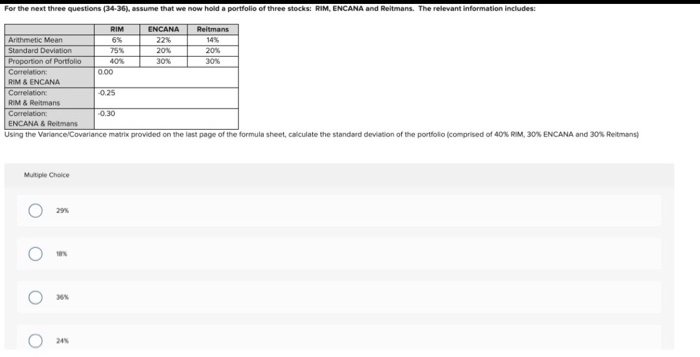

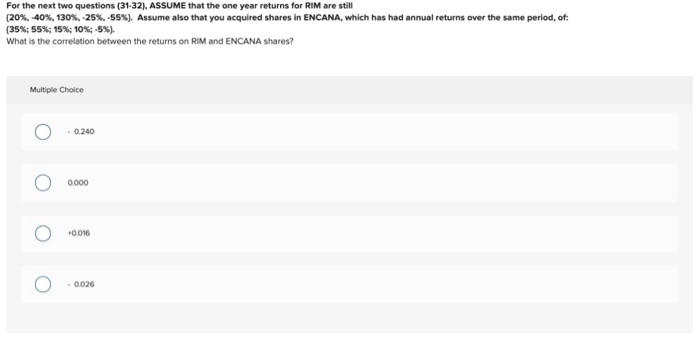

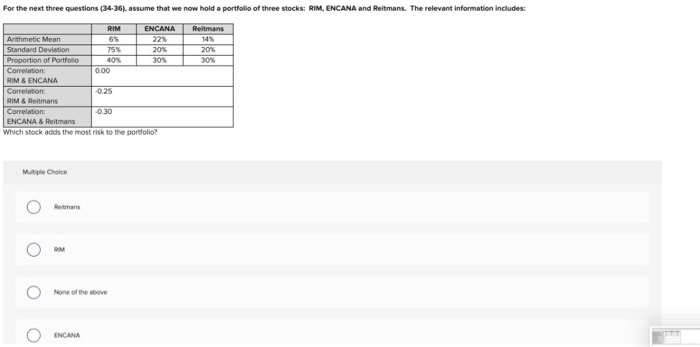

For the next two questions (31-32), ASSUME that the one year returns for RIM are still (20%, -40%, 130%, -25%, -55%). Assume also that you acquired shares in ENCANA, which has had annual returns over the same period, of: (35%; 55%: 15%: 10%-5%). Assume that you own a portfolio comprised of 40% RIM and 60% ENCANA. What return do you expect to earn next year on this portfolio? Multiple Choice 18.8% 0 174% O O 15.6% 20.8% For this question, assume that RIM has a standard deviation of 75%, ENCANA has a standard deviation of 20% and the correlation between RIM and ENCANA is 0.0. Multiple Choice 32.3% 20.5% 29.3% o 28.8% For the next three questions (34-36), assume that we now hold a portfolio of three stocks: RIM, ENCANA and Reitmans. The relevant information includes: RIM 6% 75% 40% 0.00 ENCANA 225 20% 30% Reitmans 14% 20% 30% Arithmetic Mean Standard Deviation Proportion of Portfolio Correlation RIM & ENCANA Correlation RIM & Reitmans Correlation ENCANA & Reitmans -0.25 -0.30 What retum would you expect next year for a portfolio comprised of 40% RIM, 30% ENCANA and 30% Retmans? Multiple Choice o 16.4% O 13.2% 190 O o For the next three questions (34-36), assume that we now hold a portfolio of three stocks: RIM, ENCANA and Reitmans. The relevant information includes: RIM ENCANA 22% 20% 30% Reitmans 14% 20% 30% 75% 40% 000 Arithmetic Mean Standard Deviation Proportion of Portfolio Correlation RIM & ENCANA Correlation: RIM & Reitmans Correlation: ENCANA & Reitman -0.25 -0.30 Using the Variance Covariance matrix provided on the last page of the formula sheet, calculate the standard deviation of the portfolio (comprised of 40% RIM, 30% ENCANA and 30% Retmans) Multiple Choice O o O o 24 For the next two questions (31-32), ASSUME that the one year returns for RIM are still (20% -40%, 130%-25%, -55%). Assume also that you acquired shares in ENCANA, which has had annual returns over the same period, of: (35%: 55%; 15%: 10%; -5%). What is the correlation between the returns on RIM and ENCANA shares? Multiple Choice -0.240 0.000 +0046 O 0 -0.026 For the next three questions (34-36), assume that we now hold a portfolio of three stocks: RIM, ENCANA and Reitmans. The relevant information includes: Reitmans 14% 20% 30% RIM ENCANA Arithmetic Mean 6% 22% Standard Deviation 75% 20% Proportion of Portfolio 40% 30% Correlation: 0.00 RIM & ENCANA Correlation: -0.25 RIM & Reitmans Correlation -0.30 ENCANA & Reitmans Which stock adds the most risk to the portfolio? Multiple Choice Romans O None of the above o ENCANA

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts