Question: Please show full working with formulas Question 7 (1 point) Jack has invested $300,000 in security A, B and C. Their weights and beta are

Please show full working with formulas

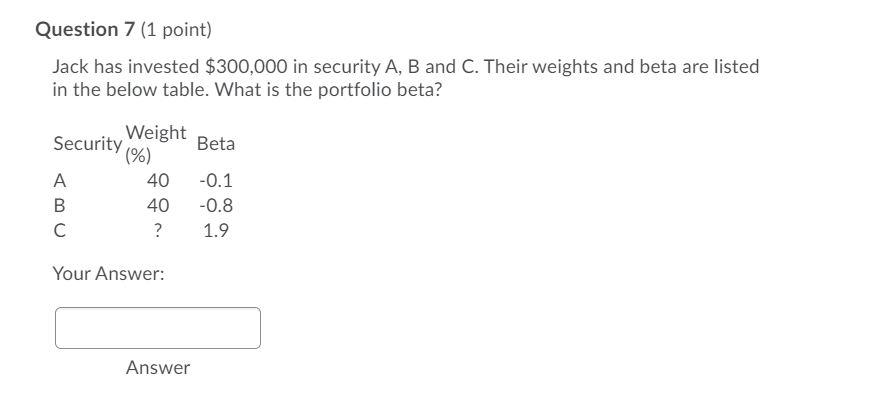

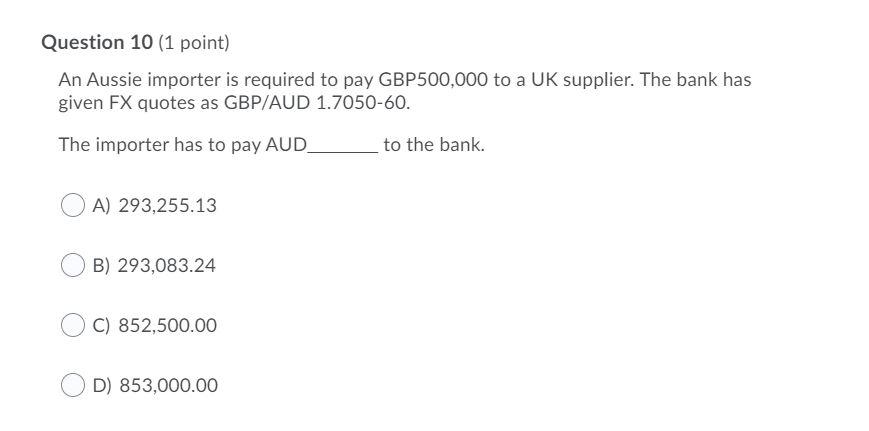

Question 7 (1 point) Jack has invested $300,000 in security A, B and C. Their weights and beta are listed in the below table. What is the portfolio beta? Weight Security (%) Beta A 40 -0.1 B 40 -0.8 C ? 1.9 Your Answer: Answer Question 8 (1 point) Simon only holds two investments, security A and B. Security A has a weight of 70%. The standard deviation of security A is 7% while the standard deviation of security B is 4%. The correlation coefficient between their returns is 0.70. What is the standard deviation of his portfolio's return? Question 10 (1 point) An Aussie importer is required to pay GBP500,000 to a UK supplier. The bank has given FX quotes as GBP/AUD 1.7050-60. The importer has to pay AUD to the bank. A) 293,255.13 B) 293,083.24 C) 852,500.00 D) 853,000.00 If USD/AUD is 1.1744 and USD/JPY is 119.34, the exchange rate between the Australian Dollar and the Japanese Yen (AUD/JPY) must be Hint: write up to 2 decimal points. If your answer is 110.115, input 110.12

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts