Question: please show steps For problems 14 below, assume zero-coupon yields on default-free securities are as summarized in the follawing table: 1. What is the price

please show steps

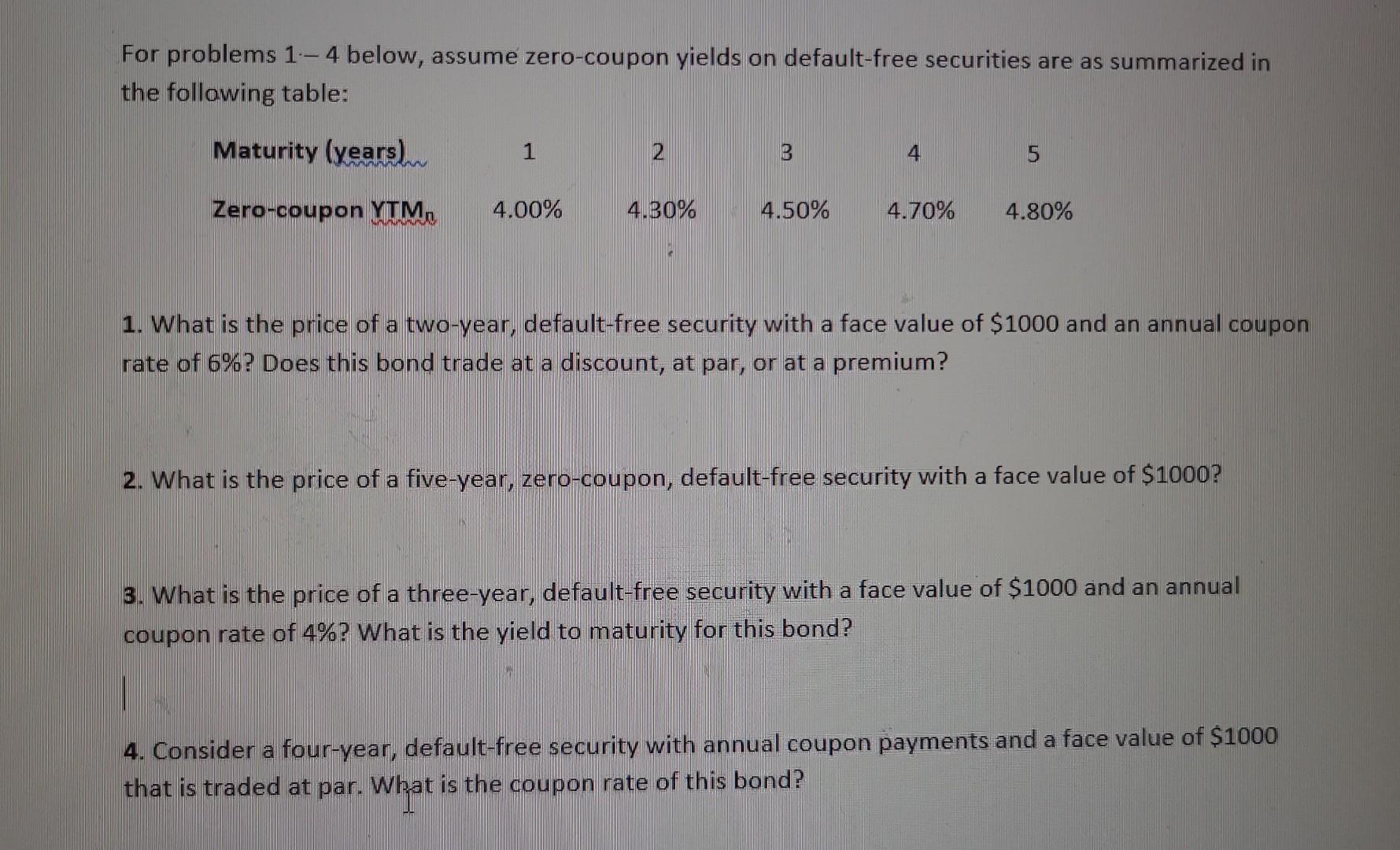

For problems 14 below, assume zero-coupon yields on default-free securities are as summarized in the follawing table: 1. What is the price of a two-year, default-free security with a face value of $1000 and an annual coupon rate of 6% ? Does this bond trade at a discount, at par, or at a premium? 2. What is the price of a five-year, zero-coupon, default-free security with a face value of $1000 ? 3. What is the price of a three-year, default-free security with a face value of $1000 and an annual coupon rate of 4% ? What is the yield to maturity for this bond? 4. Consider a four-year, default-free security with annual coupon payments and a face value of $1000 that is traded at par. What is the coupon rate of this bond

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts