Question: Please show work. 5. Consider a forward start option which, 1 year from today, will give its owner a 1-year European call option with a

Please show work.

Please show work.

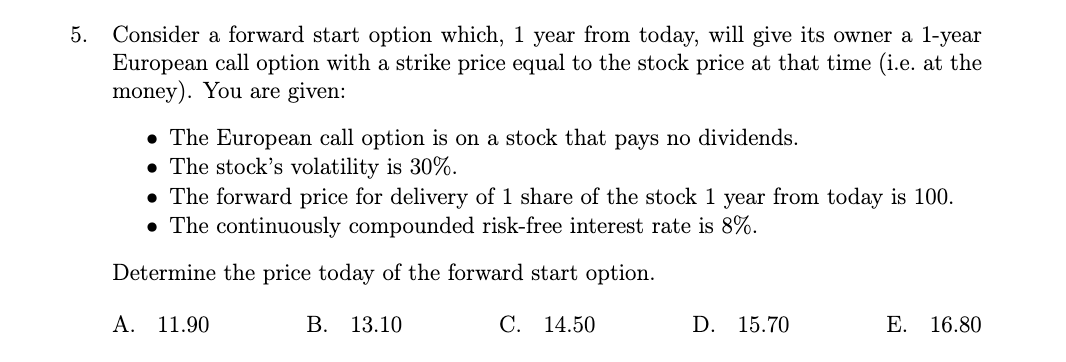

5. Consider a forward start option which, 1 year from today, will give its owner a 1-year European call option with a strike price equal to the stock price at that time (i.e. at the money). You are given: The European call option is on a stock that pays no dividends. The stock's volatility is 30%. The forward price for delivery of 1 share of the stock 1 year from today is 100. The continuously compounded risk-free interest rate is 8%. Determine the price today of the forward start option. A. 11.90 B. 13.10 C. 14.50 D. 15.70 E. 16.80

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock