Question: please show work A. We are Bechtel, a private US construction firm We bid to develop the airport and the surrounding area for Thailand. We

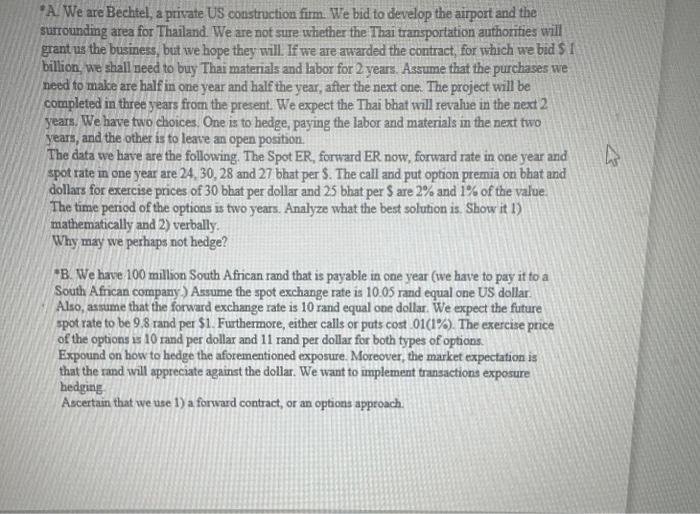

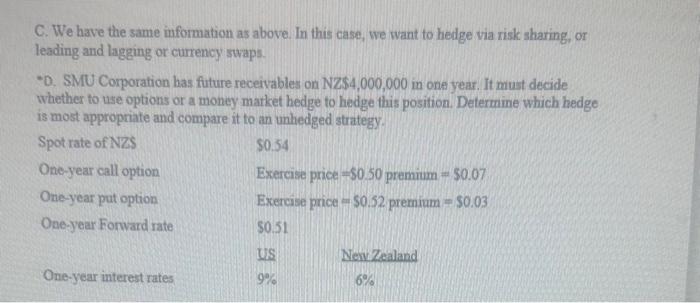

"A. We are Bechtel, a private US construction firm We bid to develop the airport and the surrounding area for Thailand. We are not sure whether the Thai transportation aufhorifies will grant us the business, but we hope they will. If we are awarded the contract, for which we bid SI billion, we stall need to buy Thai materials and labor for 2 years. Assume that the purchases we need to make are half in one year and half the year, after the next one. The project will be completed in three years from the present. We expect the Thai bhat will revalue in the next 2 years. We have two choices. One is to hedge, paying the labor and materials in the next two years, and the other is to leave an open position. The data we have are the following. The Spot ER, forward ER now, forward rate in one year and spot rate in one year are 24,30,28 and 27 bhat per $. The call and put option premia on bhat and dollars for exercise prices of 30 bhat per dollar and 25 bhat per $ are 2% and 1% of the value. The time period of the options is two years. Analyze what the best solution is. Show it 1) mathematically and 2 ) verbally. Why may we perhaps not hedge? "B. We have 100 million South African rand that is payable in one year (we have to pay it to a South African company) Assume the spot exchange rate is 10.05 rand equal one US dollar. Also, assume that the forward exchange rate is 10 rand equal one dollar. We expect the future spot rate to be 9.8 rand per $1. Furthermore, either calls or puts cost .01(1%). The exercise price of the options is 10 rand per dollar and 11 rand per dollar for both types of options. Expound on how to hedge the aforementioned exposure. Moreover, the market expectation is that the rand will appreciate against the dollar. We want to implement transactions exposure hedging Ascertain that we use 1) a forward contract, or an options approach. C. We have the same information as above. In this case, we want to hedge via risk sharing, or leading and lagging or currency swaps. -D. SMU Corporation has future receivables on NZS4,000,000 in one year. It mut decide whether to use options or a money market hedge to hedge fhis position. Determine which hedge is most appropriate and compare it to an unhedged strategy

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts