Question: *Please show work and explain steps* Your client owns a large-cap mutual fund. She has asked you to help her decide which one of the

*Please show work and explain steps*

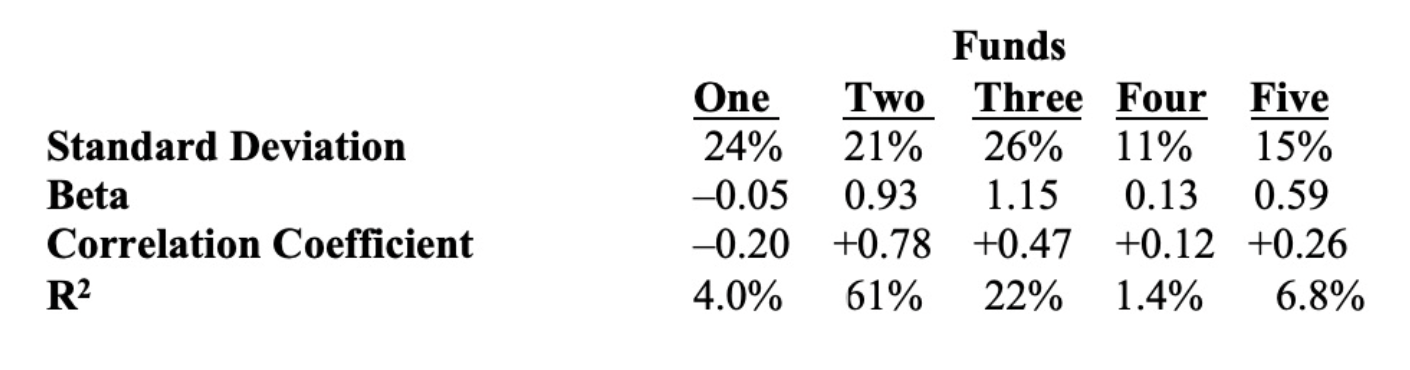

Your client owns a large-cap mutual fund. She has asked you to help her decide which one of the following funds she should add to her portfolio. Her only requirement is that the new fund contribute minimal additional risk when combined with the large- cap fund she already owns. (After she adds the new fund to her portfolio, she anticipates the large-cap fund will continue to represent about 90% of the value of her portfolio and the new fund will make up 10% of the portfolio.) The large-cap funds standard deviation is 17%, its beta is 1.07, and its R2 is 91% with the market index. The Beta and R2 calculations below were estimated by conducting regression analyses of the returns of each fund with the market index. The correlation coefficients below were estimated by correlating the past returns of each fund with the returns of the clients large-cap fund for the same time periods.

Standard Deviation Beta Correlation Coefficient R2 Funds One Two Three Four Five 24% 21% 26% 11% 15% -0.05 0.93 1.15 0.13 0.59 -0.20 +0.78 +0.47 +0.12 +0.26 4.0% 61% 22% 1.4% 6.8%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts