Question: Please show work for this question. Will give thumbs up. Problem ARB-10B This is a continuation of an example from Chapter 7. Today is time

Please show work for this question. Will give thumbs up.

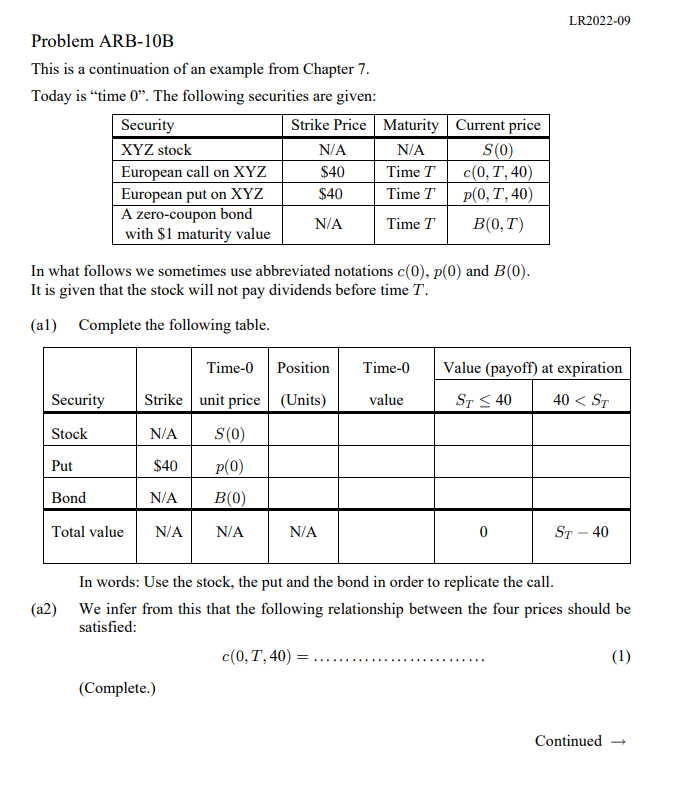

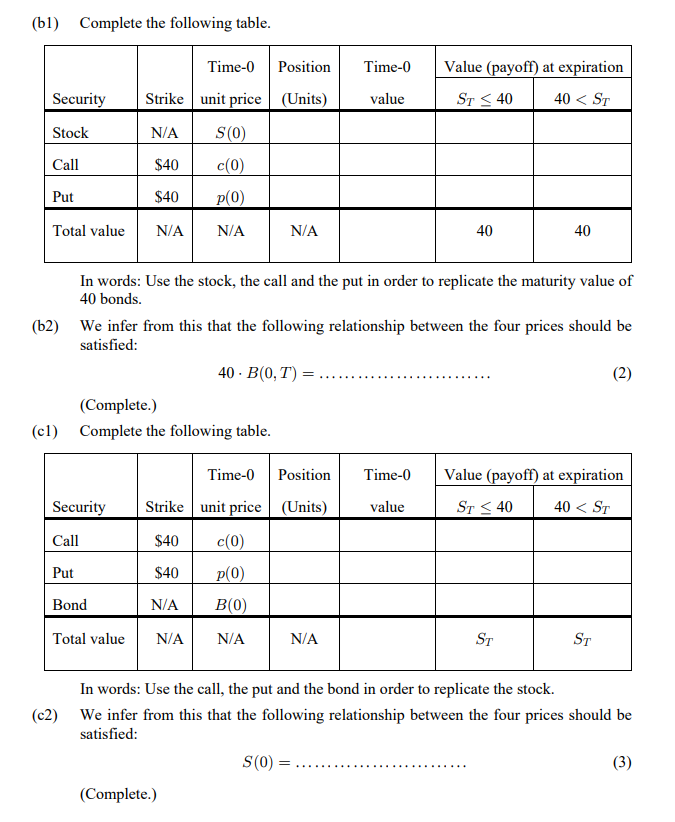

Problem ARB-10B This is a continuation of an example from Chapter 7. Today is "time 0 ". The following securities are given: In what follows we sometimes use abbreviated notations c(0),p(0) and B(0). It is given that the stock will not pay dividends before time T. (a1) Complete the following table. In words: Use the stock, the put and the bond in order to replicate the call. (a2) We infer from this that the following relationship between the four prices should be satisfied: c(0,T,40)=. (Complete.) (b1) Complete the following table. In words: Use the stock, the call and the put in order to replicate the maturity value of 40 bonds. (b2) We infer from this that the following relationship between the four prices should be satisfied: 40B(0,T)= (Complete.) (c1) Complete the following table. In words: Use the call, the put and the bond in order to replicate the stock. (c2) We infer from this that the following relationship between the four prices should be satisfied: S(0)= (Complete.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts