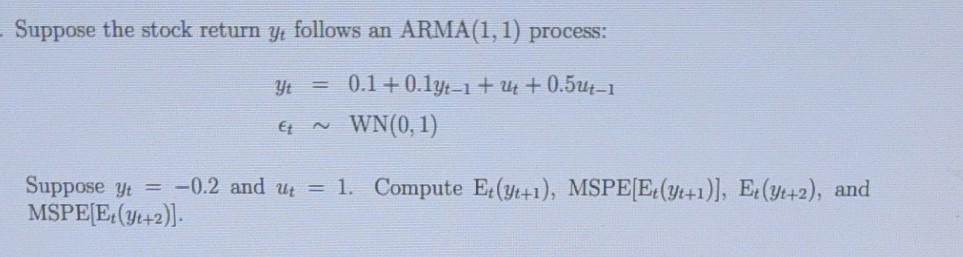

Question: Please show work for thumbs up:) Suppose the stock return yt follows an ARMA(1,1) process: yt = 0.1 +0.14-1 + 4 + 0.5ut-1 WN(0,1) Suppose

Please show work for thumbs up:)

Suppose the stock return yt follows an ARMA(1,1) process: yt = 0.1 +0.14-1 + 4 + 0.5ut-1 WN(0,1) Suppose yt = -0.2 and ut = 1. Compute Et(yt+1), MSPE[E4(yt+1)], E (yx+2), and MSPE[E(y+2)] Suppose the stock return yt follows an ARMA(1,1) process: yt = 0.1 +0.14-1 + 4 + 0.5ut-1 WN(0,1) Suppose yt = -0.2 and ut = 1. Compute Et(yt+1), MSPE[E4(yt+1)], E (yx+2), and MSPE[E(y+2)]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock