Question: Please show working and formula step by step. Much appreciate if you could help c) too. (b) The following information is available for another investment

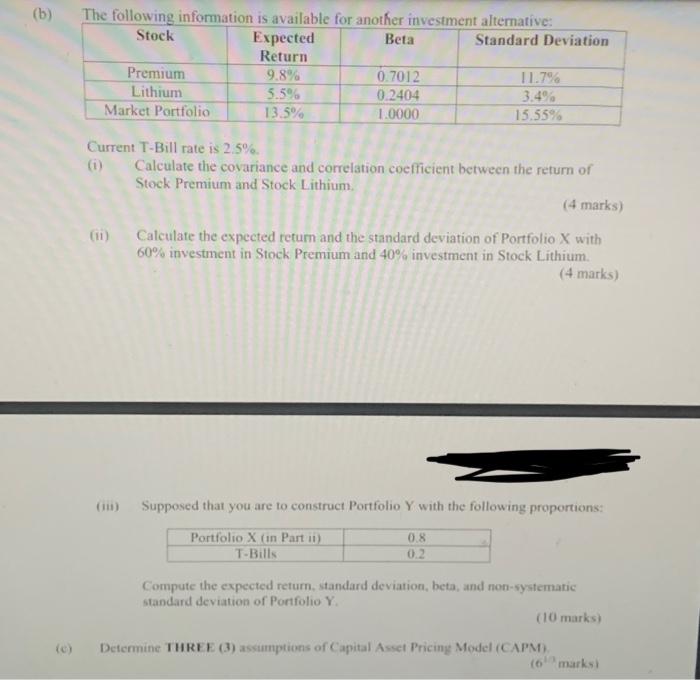

(b) The following information is available for another investment alternative: Stock Expected Beta Standard Deviation Return Premium 9.8% 0.7012 11.7% Lithium 5.5% 0.2404 3.4% Market Portfolio 13.5% 1.0000 15.53% Current T-Bill rate is 2.5%. (i) Calculate the covariance and correlation coefficient between the return of Stock Premium and Stock Lithium (4 marks) (1) Calculate the expected retum and the standard deviation of Portfolio X with 60% investment in Stock Premium and 40% investment in Stock Lithium. (4 marks) Supposed that you are to construct Portfolio Y with the following proportions: Portfolio X (in Part ii) T-Bills 0.8 0.2 Compute the expected retum, standard deviation, beta, and non-systematic standard deviation of Portfolio Y. (10 marks) Determine THREE (3) assumptions of Capital Asset Pricing Model (CAPM) (marks (b) The following information is available for another investment alternative: Stock Expected Beta Standard Deviation Return Premium 9.8% 0.7012 11.7% Lithium 5.5% 0.2404 3.4% Market Portfolio 13.5% 1.0000 15.53% Current T-Bill rate is 2.5%. (i) Calculate the covariance and correlation coefficient between the return of Stock Premium and Stock Lithium (4 marks) (1) Calculate the expected retum and the standard deviation of Portfolio X with 60% investment in Stock Premium and 40% investment in Stock Lithium. (4 marks) Supposed that you are to construct Portfolio Y with the following proportions: Portfolio X (in Part ii) T-Bills 0.8 0.2 Compute the expected retum, standard deviation, beta, and non-systematic standard deviation of Portfolio Y. (10 marks) Determine THREE (3) assumptions of Capital Asset Pricing Model (CAPM) (marks

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts