Question: Please solve all the question and explain Problem 1: You work for an Argentinean wine exporter and expect to receive USD 1 million in one

Please solve all the question and explain

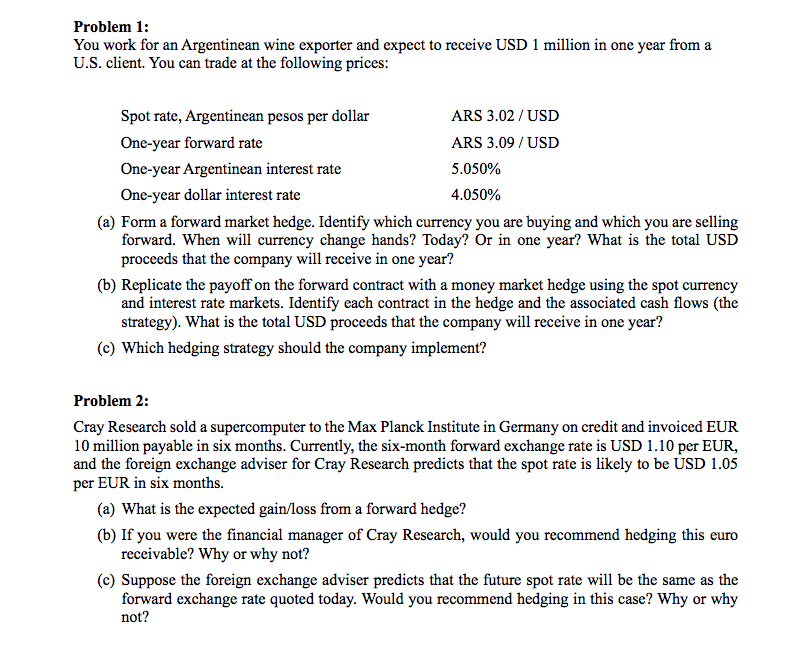

Problem 1: You work for an Argentinean wine exporter and expect to receive USD 1 million in one year from a U.S. client. You can trade at the following prices: Spot rate, Argentinean pesos per dollar ARE 3.02 1 USD l[line-year forward rate ARE 3.00 t'USD l[lne-yearu'gentinean interest rate 5.050% l[line-year dollar interest rate 4.050% (a) Form a forward market hedge. Identify which currency you are buying and which you are selling forward. When will currency change hands? Today? Or in one year? What is the total USD proceeds that the company will receive in one year? (h) Replicate the payoff on the forward contract with a money market hedge using the spot cm'rency and interest rate markets. Identify each contract in the hedge and the associated cash ows (the strategy). What is the total USD proceeds that the company will receive in one year? (c) Which hedging strategy should the company implement? Problem 2: Cray Research sold a supercomputer to the Max Planck Institute in Germany on credit and invoiced EUR 10 million payable in six months. Currently, the six-month forward exchange rate is USD 1.1Il]I per EUR, and the foreign exchange adviser for Cray Research predicts that the spot rate is likely to be USD 1.05 per EUR in six months. (a) What is the expected gainiloss from a forward hedge? (b) If you were the nancial manager of Cray Research, would you recommend hedging this euro receivable? Why or why not? (c) Suppose the foreign exchange adviser predicts that the future spot rate will he the same as the forward exchange rate quoted today. Would you recommend hedging in this case? Why or why not

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts