Question: please solve and show your work, thank you :) 15 Instructions: Show all calculations in detail. No partial credit will be given for just answers.

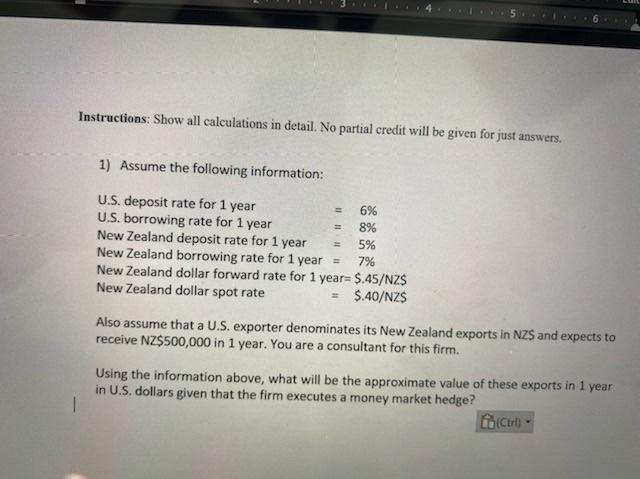

15 Instructions: Show all calculations in detail. No partial credit will be given for just answers. 1) Assume the following information: U.S. deposit rate for 1 year 6% U.S. borrowing rate for 1 year 8% New Zealand deposit rate for 1 year 5% New Zealand borrowing rate for 1 year = 7% New Zealand dollar forward rate for 1 year= $.45/NZ$ New Zealand dollar spot rate $.40/NZS Also assume that a U.S. exporter denominates its New Zealand exports in NZS and expects to receive NZ$500,000 in 1 year. You are a consultant for this firm. Using the information above, what will be the approximate value of these exports in 1 year in U.S. dollars given that the firm executes a money market hedge? (Ctrl 1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts