Question: Please solve as soon as You have run a regression of returns of ENGEL, a machine tool manufacturer, against the SEP 900 Index using monthly

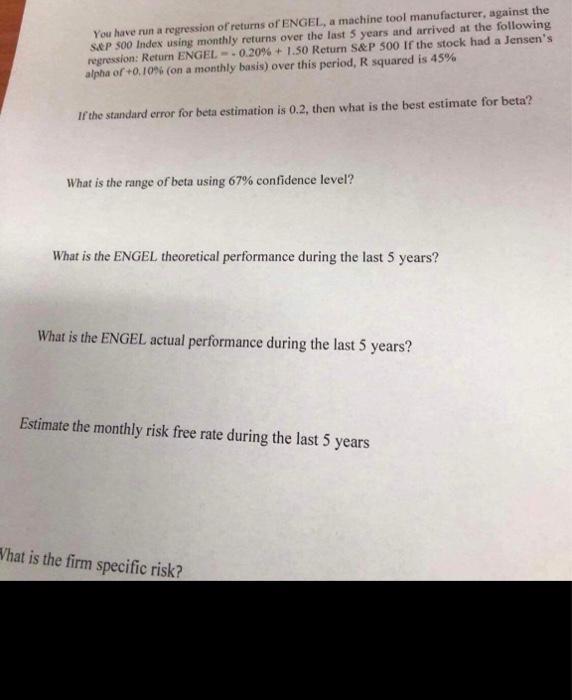

You have run a regression of returns of ENGEL, a machine tool manufacturer, against the SEP 900 Index using monthly returns over the last 5 years and arrived at the following regression: Return ENGEL -0.20% +1.50 Return S&P 500 If the stock had a Jensen's alpha of +0,10N (on a monthly basis) over this period, R squared is 45% If the standard error for beta estimation is 0.2, then what is the best estimate for beta? What is the range of beta using 67% confidence level? What is the ENGEL theoretical performance during the last 5 years? What is the ENGEL actual performance during the last 5 years? Estimate the monthly risk free rate during the last 5 years Vhat is the firm specific risk? You have run a regression of returns of ENGEL, a machine tool manufacturer, against the SEP 900 Index using monthly returns over the last 5 years and arrived at the following regression: Return ENGEL -0.20% +1.50 Return S&P 500 If the stock had a Jensen's alpha of +0,10N (on a monthly basis) over this period, R squared is 45% If the standard error for beta estimation is 0.2, then what is the best estimate for beta? What is the range of beta using 67% confidence level? What is the ENGEL theoretical performance during the last 5 years? What is the ENGEL actual performance during the last 5 years? Estimate the monthly risk free rate during the last 5 years Vhat is the firm specific risk

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts