Question: Please solve it by type it with computer keyboard Problem 3. Suppose my utility function for asset position x is given by U(x) = x2

Please solve it by type it with computer keyboard

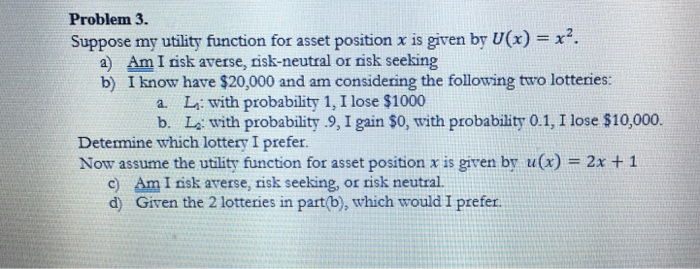

Problem 3. Suppose my utility function for asset position x is given by U(x) = x2 a) Am I risk averse, risk-neutral or risk seeking b) I know have $20,000 and am considering the following two lotteries: a. L: with probability 1, I lose $1000 b Lo with probability .9, 1 gain so, with probability 0.1, I lose $10,000. Determine which lottery I prefer Now assume the utility function for asset position x is given by u(x) = 2x + 1 c) Am I risk averse, risk seeking, or risk neutral. d) Given the 2 lotteries in part(b), which would I prefer

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock