Question: Please solve problem (c) only! FYI, u(CE) = E(u(L) = p 1 u(w 1 ) + p 2 u(w 2 ) Thank you. The coefficient

Please solve problem (c) only!

FYI, u(CE) = E(u(L) = p1u(w1) + p2u(w2)

Thank you.

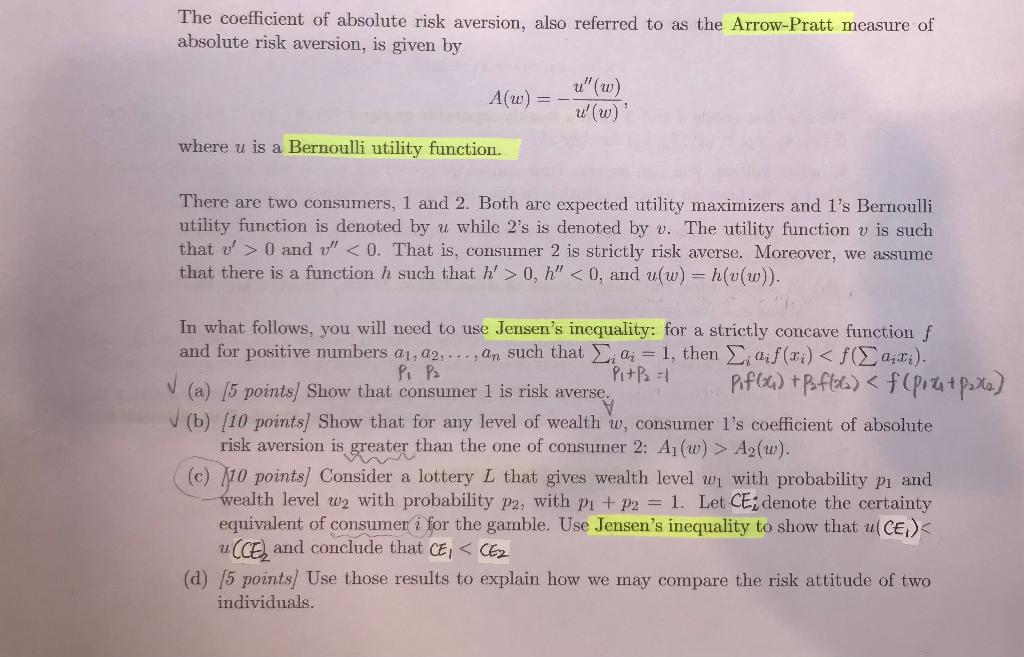

The coefficient of absolute risk aversion, also referred to as the Arrow-Pratt measure of absolute risk aversion, is given by u"(w) A(W) = - where u is a Bernoulli utility function. There are two consumers, 1 and 2. Both are expected utility maximizers and 1's Bernoulli utility function is denoted by u while 2's is denoted by u. The utility function v is such that v'>0 and u 0,h" A2(w). (c) 110 points) Consider a lottery L that gives wealth level wi with probability p and wealth level w2 with probability P2, with pi + P2 = 1. Let CE; denote the certainty equivalent of consumer i for the gamble. Use Jensen's inequality to show that ulCE) (CE) and conclude that CE, CE2 (d) (5 points Use those results to explain how we may compare the risk attitude of two individuals. The coefficient of absolute risk aversion, also referred to as the Arrow-Pratt measure of absolute risk aversion, is given by u"(w) A(W) = - where u is a Bernoulli utility function. There are two consumers, 1 and 2. Both are expected utility maximizers and 1's Bernoulli utility function is denoted by u while 2's is denoted by u. The utility function v is such that v'>0 and u 0,h" A2(w). (c) 110 points) Consider a lottery L that gives wealth level wi with probability p and wealth level w2 with probability P2, with pi + P2 = 1. Let CE; denote the certainty equivalent of consumer i for the gamble. Use Jensen's inequality to show that ulCE) (CE) and conclude that CE, CE2 (d) (5 points Use those results to explain how we may compare the risk attitude of two individuals

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts