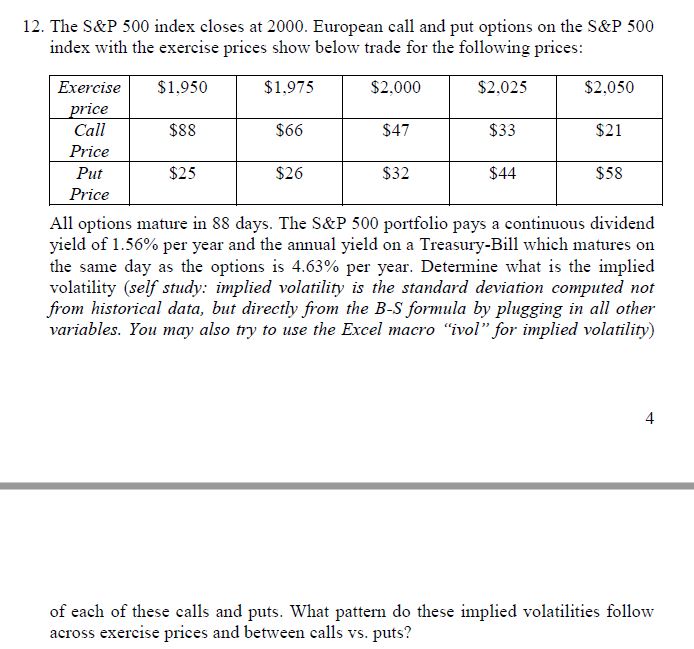

Question: Please solve the below study issue in EXCEL and show the working. 12. The S&P 500 index closes at 2000. European call and put options

Please solve the below study issue in EXCEL and show the working.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock